PG&E 2011 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2011 PG&E annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

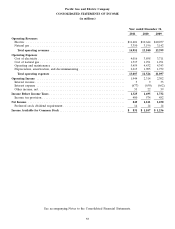

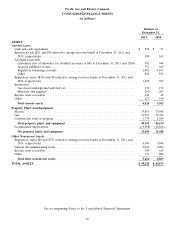

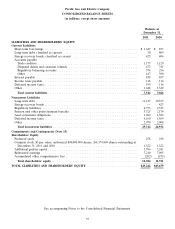

NOTE 2: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

table sets forth the after-tax changes in each component of PG&E Corporation’s accumulated other comprehensive

loss:

2011 2010 2009

(in millions)

Balance at beginning of year ............................................... $(202) $(160) $(221)

Period change in pension benefits and other benefits (Note 12):

Unrecognized prior service cost(1) .......................................... 36 (29) (1)

Unrecognized net gain (loss)(2) ............................................ (655) (110) 363

Unrecognized net transition obligation(3) ..................................... 15 15 15

Transfer to regulatory account(4)(5) .......................................... 593 82 (316)

Balance at end of year ................................................... $(213) $(202) $(160)

(1) Net of income tax benefit (expense) of $(24) million, $20 million, and $1 million for December 31, 2011, 2010, and 2009, respectively.

(2) Net of income tax benefit (expense) of $452 million, $73 million, and $(216) million for December 31, 2011, 2010, and 2009, respectively.

(3) Net of income tax benefit (expense) of $(11) million for December 31, 2011, 2010, and 2009.

(4) Net of income tax benefit (expense) of $(408) million, $(57) million, and $218 million for December 31, 2011, 2010, and 2009, respectively.

(5) Amounts transferred to the pension regulatory asset are probable of recovery from customers in future rates.

There was no material difference between PG&E Corporation’s and the Utility’s accumulated other

comprehensive income (loss) for the periods presented above.

Revenue Recognition

The Utility recognizes revenues after the CPUC or the FERC has authorized rate recovery, amounts are

objectively determinable and probable of recovery, and amounts will be collected within 24 months. (See Note 3

below.) The Utility recognizes revenues as the electricity and natural gas services are delivered, and include amounts

for services rendered but not yet billed at the end of the period.

The CPUC authorizes most of the Utility’s revenue requirements in its general rate case (‘‘GRC’’), which

generally occurs every three years. The Utility’s ability to recover revenue requirements authorized by the CPUC in

the GRC is independent, or ‘‘decoupled’’, from the volume of the Utility’s sales of electricity and natural gas services.

Generally, the revenue recognition criteria are met ratably over the year.

The CPUC also has authorized the Utility to collect additional revenue requirements to recover certain capital

expenditures and costs that the Utility has been authorized to pass on to customers, including costs to purchase

electricity and natural gas; to fund public purpose, demand response, and customer energy efficiency programs.

Generally, the revenue recognition criteria for pass through costs billed to customers are met at the time the costs

are incurred.

The Utility’s revenues and earnings also are affected by incentive ratemaking mechanisms that adjust rates

depending on the extent to which the Utility meets certain performance criteria.

The FERC authorizes the Utility’s revenue requirements in annual transmission owner rate cases. The Utility’s

ability to recover revenue requirements authorized by the FERC is dependent on the volume of the Utility’s

electricity sales, and revenue is recognized only for amounts billed and unbilled.

The Utility records differences between actual customer billings and the Utility’s authorized revenue

requirement, as well as differences between incurred costs and customer billings or authorized revenue meant to

recover those costs. To the extent these differences are probable of recovery or refund, the Utility records a

regulatory balancing account asset or liability, respectively.

In determining whether revenue transactions should be presented net of the related expenses, the Utility

considers various factors, including whether the Utility takes title to the product being delivered, has latitude in

establishing price for the product, and is subject to the customer credit risk.

64