PG&E 2011 Annual Report Download - page 88

Download and view the complete annual report

Please find page 88 of the 2011 PG&E annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

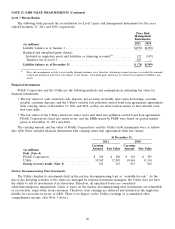

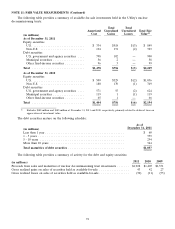

NOTE 10: DERIVATIVES AND HEDGING ACTIVITIES (Continued)

The Utility uses both derivative and non-derivative contracts in managing its customers’ exposure to commodity-

related price risk, including:

• forward contracts that commit the Utility to purchase a commodity in the future;

• swap agreements that require payments to or from counterparties based upon the difference between two

prices for a predetermined contractual quantity; and

• option contracts that provide the Utility with the right to buy a commodity at a predetermined price.

These instruments are not held for speculative purposes and are subject to certain regulatory requirements.

Commodity-related price risk management activities that meet the definition of derivatives are recorded at fair

value on the Consolidated Balance Sheets. As long as the current ratemaking mechanisms discussed above remain in

place and the Utility’s risk management activities are carried out in accordance with CPUC directives, the Utility

expects to fully recover, in rates, all costs related to commodity derivative instruments. Therefore, all unrealized gains

and losses associated with the change in fair value of these derivative instruments are deferred and recorded within

the Utility’s regulatory assets and liabilities on the Consolidated Balance Sheets. (See Note 3 above.) Net realized

gains or losses on commodity derivative instruments are recorded in the cost of electricity or the cost of natural gas

with corresponding increases or decreases to regulatory balancing accounts for recovery from customers.

The Utility elects the normal purchase and sale exception for qualifying commodity derivative instruments.

Derivative instruments that require physical delivery in quantities that are expected to be used by the Utility over a

reasonable period in the normal course of business, and do not contain pricing provisions unrelated to the

commodity delivered are eligible for the normal purchase and sale exception. The fair value of instruments that are

eligible for the normal purchase and sales exception are not reflected in the Consolidated Balance Sheets.

Electricity Procurement

The Utility enters into third-party power purchase agreements for electricity to meet customer needs. The

Utility’s third-party power purchase agreements are generally accounted for as leases, but certain third-party power

purchase agreements are considered derivative instruments. The Utility elects the normal purchase and sale

exception for eligible derivative instruments.

A portion of the Utility’s third-party power purchase agreements contain market-based pricing terms. In order to

reduce volatility in customer rates, the Utility enters into financial swap contracts to effectively fix the price of future

purchases and reduce cash flow variability associated with fluctuating electricity prices. These financial swaps are

considered derivative instruments.

Electric Transmission Congestion Revenue Rights

The California electric transmission grid, controlled by the California Independent System Operator (‘‘CAISO’’),

is subject to transmission constraints when there is insufficient transmission capacity to supply the market resulting in

transmission congestion. The CAISO imposes congestion charges on market participants to manage transmission

congestion. To allocate the congestion revenues among the market participants the CAISO has created congestion

revenue rights (‘‘CRRs’’) to allow market participants to hedge the financial risk of CAISO-imposed congestion

charges in the day-ahead market. The CAISO releases CRRs through an annual and monthly process, each of which

includes an allocation phase (in which load-serving entities such as the Utility are allocated CRRs at no cost based

on the customer demand or ‘‘load’’ they serve) and an auction phase (in which CRRs are priced at market and

available to all market participants). The Utility participates in the allocation and auction phases of the annual and

monthly CRR processes. The CRRs held by the Utility are considered derivative instruments.

Natural Gas Procurement (Electric Fuels Portfolio)

The Utility’s electric procurement portfolio is exposed to natural gas price risk primarily through physical natural

gas commodity purchases to fuel Utility-owned natural gas generating facilities and tolling agreements, and electricity

procurement contracts indexed to natural gas prices. To reduce the volatility in customer rates, the Utility purchases

financial instruments such as swaps and options to reduce future cash flow variability from fluctuating natural gas

prices. These financial instruments are considered derivative instruments.

84