PG&E 2011 Annual Report Download - page 93

Download and view the complete annual report

Please find page 93 of the 2011 PG&E annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

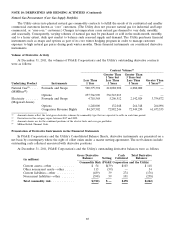

|

|

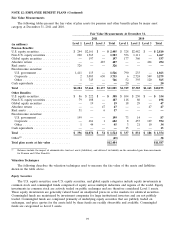

NOTE 11: FAIR VALUE MEASUREMENTS (Continued)

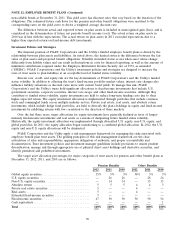

Trust Assets

The assets held by the nuclear decommissioning trusts, the rabbi trusts related to the non-qualified deferred

compensation plans, and the long-term disability trust are composed primarily of equity securities, debt securities,

and life insurance policies. In general, investments held in the trusts are exposed to various risks, such as interest

rate, credit, and market volatility risks.

Equity securities primarily include investments in common stock, which are valued based on unadjusted prices in

active markets for identical securities and are classified as Level 1. Equity securities also include commingled funds

composed of equity securities traded publicly on exchanges across multiple industry sectors in the U.S. and other

regions of the world, which are classified as Level 2. Price quotes for the assets held by these funds are readily

observable and available.

Debt securities are composed primarily of fixed-income securities that include U.S. government and agency

securities, municipal securities, and corporate debt securities. U.S. government and agency securities consist primarily

of treasury securities that are classified as Level 1 because the fair value is determined by observable market prices

in active markets. A market-based valuation approach is generally used to estimate the fair value of debt securities

classified as Level 2. Under a market approach, fair values are determined based on evaluated pricing data, such as

broker quotes, for similar securities adjusted for observable differences. Significant inputs used in the valuation

model generally include benchmark yield curves and issuer spreads. The external credit rating, coupon rate, and

maturity of each security are considered in the valuation, as applicable.

Price Risk Management Instruments

Price risk management instruments include physical and financial derivative contracts, such as forwards, swaps,

options, and CRRs that are either exchange-traded or over-the-counter traded. (See Note 10 above.)

Exchange-traded forwards and swaps that are valued using observable market prices for the underlying

commodity are classified as Level 1. Forwards and swaps transacted in the over-the-counter market that are identical

to exchange-traded forwards and swaps or are valued using market-corroborated inputs are classified as Level 2.

Forwards and swaps that are valued using unobservable data are classified as Level 3. These contracts are valued

using either estimated basis adjustments from liquid trading points or techniques, including extrapolation from

observable prices, when a contract term extends beyond a period for which market data is available.

Exchange-traded options are valued using observable market data and market-corroborated data and are

classified as Level 2. Over-the-counter options are valued using a standard option pricing model which includes

forward prices for the underlying commodity, time value at a risk-free rate, and volatility and are classified as

Level 3. For periods where market data is not available, the Utility extrapolates observable data using internal

models.

The Utility holds CRRs to hedge financial risk of CAISO-imposed congestion charges in the day-ahead market.

CRRs are valued based on prices observed in the auction which are extrapolated and discounted at the risk free rate.

Limited market data is available between auction dates; therefore, CRRs are classified as Level 3.

Transfers between Levels

PG&E Corporation and the Utility recognize any transfers between levels in the fair value hierarchy as of the

end of the reporting period. At December 31, 2011, the valuation of price risk management over-the-counter

forwards and swaps and exchange-traded options incorporated market observable and market corroborated inputs,

where certain previously-considered unobservable inputs became observable. Therefore, the Utility transferred these

instruments out of Level 3 and into Level 2. No significant transfers between Levels 1 and 2 occurred in the years

ended December 31, 2011 and 2010.

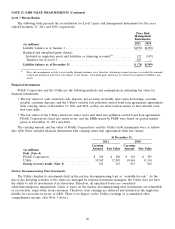

89