MasterCard 2011 Annual Report Download - page 138

Download and view the complete annual report

Please find page 138 of the 2011 MasterCard annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

MASTERCARD INCORPORATED

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

between the payment transaction date and subsequent settlement. The duration of this exposure is short term and

typically limited to a few days. Settlement Exposure is primarily estimated using the average daily card volume

during the quarter multiplied by the estimated number of days to settle. The Company has global risk

management policies and procedures, which include risk standards, to provide a framework for managing the

Company’s settlement risk. Customer-reported transaction data and the transaction clearing data underlying the

settlement risk calculation may be revised in subsequent reporting periods.

In the event that MasterCard effects a payment on behalf of a failed customer, MasterCard may seek an

assignment of the underlying receivables. Subject to approval by the Board of Directors, customers may be

charged for the amount of any settlement loss incurred during these ordinary course activities of the Company.

The Company’s global risk management policies and procedures are aimed at managing the risk of

settlement loss. These risk management procedures include interaction with the bank regulators of countries in

which we operate, requiring customers to make adjustments to settlement processes, and requiring collateral from

customers. MasterCard requires certain customers that are not in compliance with the Company’s risk standards

in effect at the time of review to post collateral, typically in the form of cash, letters of credit, or guarantees. This

requirement is based on management’s review of the individual risk circumstances for each customer that is out

of compliance. In addition to these amounts, MasterCard holds collateral to cover variability and future growth in

customer programs. The Company may also hold collateral to pay merchants in the event of merchant bank/

acquirer failure. Although we are not contractually obligated under our rules to effect such payments to

merchants, we may elect to do so to protect brand integrity. MasterCard monitors its credit risk portfolio on a

regular basis and the adequacy of collateral on hand. Additionally, from time to time, the Company reviews its

risk management methodology and standards. As such, the amounts of estimated settlement risk are revised as

necessary.

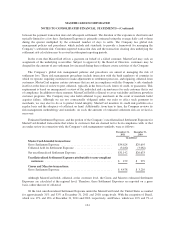

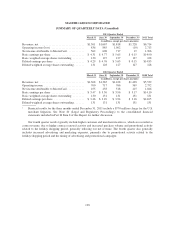

Estimated Settlement Exposure, and the portion of the Company’s uncollateralized Settlement Exposure for

MasterCard-branded transactions that relates to customers that are deemed not to be in compliance with, or that

are under review in connection with, the Company’s risk management standards, were as follows:

December 31,

2011

December 31,

2010

(in millions)

MasterCard-branded transactions:

Gross Settlement Exposure .................................... $34,624 $29,695

Collateral held for Settlement Exposure .......................... (3,482) (3,062)

Net uncollateralized Settlement Exposure ......................... $31,142 $26,633

Uncollateralized Settlement Exposure attributable to non-compliant

customers ............................................... $ 479 $ 279

Cirrus and Maestro transactions:

Gross Settlement Exposure .................................... $ 4,478 $ 3,210

Although MasterCard holds collateral at the customer level, the Cirrus and Maestro estimated Settlement

Exposures are calculated at the regional level. Therefore, these Settlement Exposures are reported on a gross

basis, rather than net of collateral.

Of the total uncollateralized Settlement Exposure under the MasterCard brand, the United States accounted

for approximately 31% and 33% at December 31, 2011 and 2010, respectively. With the exception of Brazil,

which was 17% and 16% at December 31, 2011 and 2010, respectively, and France, which was 10% and 7% at

134