MasterCard 2011 Annual Report Download - page 112

Download and view the complete annual report

Please find page 112 of the 2011 MasterCard annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

MASTERCARD INCORPORATED

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

The Company’s discount rate assumptions are based on a yield curve derived from high quality corporate

bonds, which is matched to the expected cash flows to each of the respective Plans.

For the Qualified Plan, the Company utilized an actuarial practice referred to as a building block method to

determine the assumption for the expected weighted average return on plan assets. This method includes the

following components: (1) compiling historical return data for both the equity and fixed income markets over the

past ten-, twenty- and thirty-year periods; (2) weighting the assets within our portfolio at December 31, 2011 by

class; and (3) identifying expected rate of return on assets utilizing both current and historical market experience.

Plan assets are managed with a long-term perspective intended to ensure that there is an adequate level of

assets to support benefit payments to participants over the life of the Qualified Plan. In 2011, the Company

conducted an asset-liability study to assess the preferred target asset allocation. As a result of the study, the

Company increased the asset allocation to fixed income from 30% to 60% and decreased the asset allocation to

equities from 70% to 40%. Plan assets are managed within asset allocation ranges, towards targets of 60% fixed

income, 24% large/medium cap U.S. equity, 8% small cap U.S. equity, and 8% non-U.S. equity. The Company

intends to increase the allocation to fixed income, subject to certain improvements in Plan funded status. Plan

assets are managed by external investment managers. Investment manager performance is measured against

benchmarks for each asset class and peer group on quarterly, one-, three-, and five-year periods. An external

advisor assists management with investment manager selections and performance evaluations. The balance in

cash and cash equivalents is available to pay expected benefit payments and expenses. Considering the change in

plan allocation targets, the Company reduced the 2012 expected return on plan assets assumption from 8% to 6%.

The Valuation Hierarchy of the Qualified Plan’s assets is determined using a consistent application of the

categorization measurements for the Company’s financial instruments. See Note 1 (Summary of Significant

Accounting Policies).

Mutual funds (including small cap U.S. equity securities and non-U.S. equity securities) are public

investment vehicles valued at quoted market prices, which represent the net asset value of the shares held by the

Qualified Plan and are therefore included in Level 1 of the Valuation Hierarchy. Commingled funds (including

large/medium cap U.S. equity securities and fixed income securities) are valued at unit values provided by

investment managers, which are based on the fair value of the underlying investments utilizing public

information, independent external valuation from third-party services or third-party advisors, and are therefore

included in Level 2 of the Valuation Hierarchy.

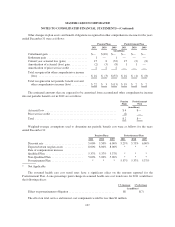

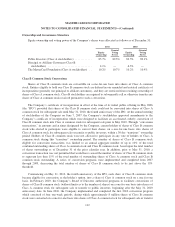

The following table sets forth by level, within the Valuation Hierarchy, the Qualified Plan’s assets at fair

value as of December 31, 2011 and 2010:

December 31, 2011

Quoted Prices

in Active

Markets

(Level 1)

Significant

Other

Observable

Inputs

(Level 2)

Significant

Unobservable

Inputs

(Level 3)

Fair

Value

(in millions)

Mutual funds:

Money market ........................ $ 2 $— $— $ 2

Domestic small cap equity ............... 19 — — 19

International equity .................... 16 — — 16

Common and collective funds:

Domestic large cap equity ............... — 59 — 59

Domestic fixed income ................. — 147 — 147

Total .................................... $ 37 $206 $— $243

108