MasterCard 2011 Annual Report Download - page 11

Download and view the complete annual report

Please find page 11 of the 2011 MasterCard annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

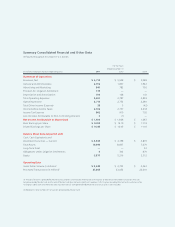

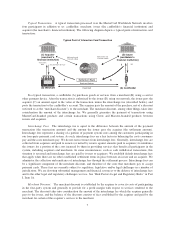

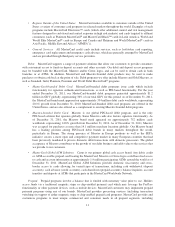

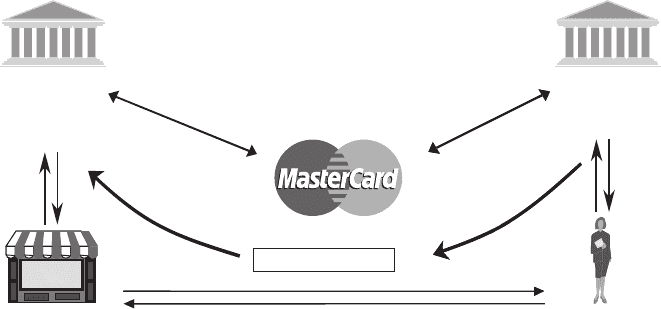

Typical Transaction. A typical transaction processed over the MasterCard Worldwide Network involves

four participants in addition to us: cardholder, merchant, issuer (the cardholder’s financial institution) and

acquirer (the merchant’s financial institution). The following diagram depicts a typical point-of-interaction card

transaction:

$

(less merchant discount)

Typical Point of Interaction Card Transaction

Authorization and

Transaction Data

Authorization and

Transaction Data

(C) Acquirer

(merchant’s

financial institution)

Transaction

Data Bill

$

(D) Issuer

(cardholder’s

financial institution)

$

(B) Merchant (A) Cardholder

Present Card

Goods and Services

Settlement Bank

$

In a typical transaction, a cardholder (A) purchases goods or services from a merchant (B) using a card or

other payment device. After the transaction is authorized by the issuer (D) using our network, the issuer pays the

acquirer (C) an amount equal to the value of the transaction, minus the interchange fee (described below), and

posts the transaction to the cardholder’s account. The acquirer pays the amount of the purchase, net of a discount

(referred to as the “merchant discount”), to the merchant. The merchant discount, among other things, takes into

consideration the amount of the interchange fee. We generally guarantee the payment of transactions using

MasterCard-branded products and certain transactions using Cirrus and Maestro-branded products between

issuers and acquirers.

Interchange Fees. The interchange fee is equal to the difference between the amount of the payment

transaction (the transaction amount) and the amount the issuer pays the acquirer (the settlement amount).

Interchange fees represent a sharing of a portion of payment system costs among the customers participating in

our four-party payment card system. As such, interchange fees are a key factor in balancing the costs consumers

pay and the costs merchants pay. We do not earn revenues from interchange fees. Generally, interchange fees are

collected from acquirers and paid to issuers (or netted by issuers against amounts paid to acquirers) to reimburse

the issuers for a portion of the costs incurred by them in providing services that benefit all participants in the

system, including acquirers and merchants. In some circumstances, such as cash withdrawal transactions, this

situation is reversed and interchange fees are paid by issuers to acquirers. We establish default interchange fees

that apply when there are no other established settlement terms in place between an issuer and an acquirer. We

administer the collection and remittance of interchange fees through the settlement process. Interchange fees can

be a significant component of the merchant discount, and therefore of the costs that merchants pay to accept

payment cards. These fees are currently subject to regulatory, legislative and/or legal challenges in a number of

jurisdictions. We are devoting substantial management and financial resources to the defense of interchange fees

and to the other legal and regulatory challenges we face. See “Risk Factors-Legal and Regulatory Risks” in Part

I, Item 1A.

Merchant Discount. The merchant discount is established by the acquirer to cover its costs of participating

in the four-party system and generally to provide for a profit margin with respect to services rendered to the

merchant. The discount takes into consideration the amount of the interchange fee which the acquirer generally

pays to the issuer, and the balance of the discount consists of fees established by the acquirer and paid by the

merchant for certain of the acquirer’s services to the merchant.

7