MasterCard 2011 Annual Report Download - page 13

Download and view the complete annual report

Please find page 13 of the 2011 MasterCard annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

supplement this protection with mitigation efforts to strengthen our protection against such threats, both in terms

of operability of the network and protection of the information transmitted through the network. To date, we have

consistently maintained availability of our global processing systems more than 99.9% of the time.

Processing Capabilities.

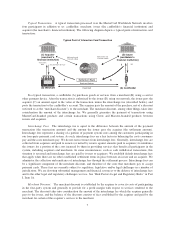

•Transaction Switching—Authorization, Clearing and Settlement. MasterCard provides transaction

switching (authorization, clearing and settlement) through the MasterCard Worldwide Network.

OAuthorization. Authorization refers to the process by which a transaction is routed to the issuer for

approval and then a decision whether or not to approve the transaction is made by the issuer or, in

certain circumstances such as when the issuer’s systems are unavailable or cannot be contacted, by

MasterCard or others on behalf of the issuer in accordance with either the issuer’s instructions or

applicable rules (also known as “stand-in”). Our standards, which may vary across regions, establish

the circumstances under which merchants and acquirers must seek authorization of transactions.

OClearing. Clearing refers to the exchange of financial transaction information between issuers and

acquirers after a transaction has been successfully conducted at the point of interaction. MasterCard

clears transactions among customers through our central and regional processing systems.

MasterCard clearing solutions can be managed with minimal system development, which has

enabled us to accelerate our customers’ ability to develop customized programs and services.

OSettlement. Once transactions have been authorized and cleared, MasterCard helps to settle the

transactions by facilitating the exchange of funds between parties. Once clearing is completed, a

daily reconciliation is provided to each customer involved in settlement, detailing the net amounts

by clearing cycle and a final settlement position. The actual exchange of funds takes place between

a settlement bank, designated by the customer and approved by MasterCard, and a settlement bank

chosen by MasterCard. Customer settlement occurs in U.S. dollars or in a limited number of other

currencies in accordance with our established rules.

•Cross-Border and Domestic Processing. The MasterCard Worldwide Network provides our customers

with a flexible structure that enables them to support processing across regions and for domestic

markets. The network processes transactions throughout the world on our branded products where the

merchant country and cardholder country are different (cross-border transactions). MasterCard

processes transactions denominated in more than 150 currencies through our global system, providing

cardholders with the ability to utilize, and merchants to accept, MasterCard cards and other payment

devices across multiple country borders. For example, we may process a transaction in a merchant’s

local currency; however the charge for the transaction would appear on the cardholder’s statement in the

cardholder’s home currency. MasterCard also provides domestic (or intra-country) transaction

processing services to customers in every region of the world, which allow customers to facilitate

payment transactions between cardholders and merchants throughout a particular country. We process

most of the cross-border transactions using MasterCard, Maestro and Cirrus-branded cards and process

the majority of MasterCard-branded domestic transactions in the United States, United Kingdom,

Canada, Brazil and a select number of other smaller countries. Outside of these countries, most intra-

country (as opposed to cross-border) transaction activity conducted with our branded payment products

is authorized, cleared and/or settled by our customers or other processors without the involvement of the

MasterCard Worldwide Network. We continue to invest in our network and build relationships to

expand opportunities for domestic transaction processing. In particular, the Single European Payment

Area (“SEPA”) initiative creates an open and competitive market in many European countries that were

previously mandated to process domestic debit transactions with domestic processors. As a result, in

addition to cross-border transactions, MasterCard now processes some domestic debit transactions in

nearly every SEPA country.

•Extended Processing Capabilities. In addition to transaction switching, MasterCard continually

evaluates and invests in ways to strategically extend our processing capabilities in the payment value

9