MasterCard 2011 Annual Report Download - page 12

Download and view the complete annual report

Please find page 12 of the 2011 MasterCard annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

Additional Fees and Economic Considerations. Among the parties in a four-party system, various types of

fees may be charged to different constituents for various services. For example, acquirers may charge merchants

processing and related fees in addition to the merchant discount. Issuers may also charge cardholders fees for the

transaction, including, for example, fees for extending revolving credit. As described below, we charge issuers

and acquirers transaction-based and related fees for the transaction processing and related services we provide

them.

In a four-party payment system, the economics of a payment transaction relative to MasterCard vary widely

depending on such factors as whether the transaction is domestic (and, if it is domestic, the country in which it

takes place) or cross-border, whether it is a point-of-sale purchase transaction or cash withdrawal, and whether

the transaction is processed over our network or a third-party network or is handled solely by a financial

institution that is both the acquirer for the merchant and the issuer to the cardholder (an “on-us” transaction).

Authentication. Generally, transactions processed over our network can be authenticated at the point of

interaction and across the processing value chain. A typical transaction processed over our network can be

authenticated in several ways (depending on the type of card or device being used):

• “signature” transactions that typically require a cardholder to sign a sales receipt as the primary means

of validation at the point of interaction (other than circumstances, such as with respect to low value

purchases, where a signature is not necessary),

• “PIN-based” transactions that require the cardholder to use a PIN for verification which can be validated

by the issuer at their processing site and

• transactions using chip-enabled cards and point of interaction devices which allow for automatic

authentication between the card and device (as well as, depending on the card or device, signature or

PIN authentication).

In addition, some payment cards and devices are equipped with an RFID (radio frequency identification)

microchip, which provides an advanced authentication technique, and technology which allows contactless

payments requiring neither signature nor PIN under established maximum transaction amounts.

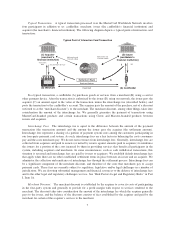

MasterCard Worldwide Network Architecture and Operations. We believe the architecture of the

MasterCard Worldwide Network is unique, featuring a globally integrated structure that provides scalability for

our customers and enables them to expand into regional and global markets. Our network also features an

intelligent architecture that enables it to adapt to the needs of each transaction by blending two distinct

processing structures-distributed (peer-to-peer) and centralized (hub-and-spoke). Transactions that require fast,

reliable processing, such as those submitted using a MasterCard PayPass®-enabled device in a tollway, use the

network’s distributed processing structure, ensuring they are processed close to where the transaction occurred.

Transactions that require value-added processing, such as real-time access to transaction data for fraud scoring or

rewards at the point-of-sale, or customization of transaction data for unique consumer-spending controls, use the

network’s centralized processing structure, ensuring advanced processing services are applied to the transaction.

Through the unique architecture of our network, we are able to connect all parties with respect to payments

transactions regardless of whether the transaction is occurring at a traditional physical location, at an ATM, on

the internet or through a mobile device, enabling electronic commerce.

The network typically operates at under 80% capacity and has the capacity to handle more than 160 million

transactions per hour with an average network response time of 130 milliseconds. The network can also

substantially scale capacity to meet demand. Our transaction processing services are available 24 hours per day,

every day of the year. Our global payment network provides multiple levels of back-up protection and related

continuity procedures should the issuer, acquirer or payment network experience a service interruption.

Moreover, the network features multiple layers of protection against hacking or other cybersecurity attacks. We

8