IHOP 2013 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2013 IHOP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

|

|

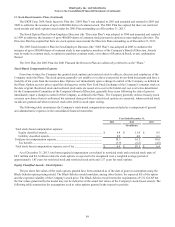

DineEquity, Inc. and Subsidiaries

Notes to the Consolidated Financial Statements (Continued)

7. Long-Term Debt (Continued)

79

letters of credit and for swing-line borrowings, and may be used for general corporate purposes, including working capital,

permitted acquisitions, capital expenditures, dividends and investments. The Credit Agreement also provides for an

uncommitted incremental facility that permits the Company, subject to certain conditions, to increase the Credit Facility by up

to $250.0 million, provided that the aggregate amount of the commitments under the Revolving Facility may not exceed $150.0

million. See “Amendments to Credit Agreement”.

Interest Rate

Loans made under the Term Facility (“Term Loans”) and the Revolving Facility (“Revolving Loans”) bore interest, at the

Company's option, at an annual rate equal to (i) a LIBOR-based rate (originally subject to a floor of 1.50%) plus a margin

(originally 4.50%) or (ii) the base rate (the “Base Rate”) (originally subject to a floor of 2.50%) which will be equal to the

highest of (a) the federal funds rate plus 0.50%, (b) the prime rate and (c) the one month LIBOR rate (originally subject to a

floor of 1.50%) plus 1.00%, plus a margin of 3.50%. The margin for the Revolving Facility is subject to debt leverage-based

step-downs. Both the Term Facility and the Revolving Facility were subject to upfront fees of 1.00% of the principal amount

thereof. See “Amendments to Credit Agreement”.

Amendments to Credit Agreement

On February 25, 2011, the Company entered into Amendment No. 1 (“Amendment No. 1”) to the Credit Agreement.

Pursuant to Amendment No. 1, the interest rate margin applicable to LIBOR-based Term Loans was reduced from 4.50% to

3.00%, and the interest rate floors used to determine the LIBOR and Base Rate reference rates for Term Loans was reduced

from 1.50% to 1.25% for LIBOR-based Term Loans and from 2.50% to 2.25% for Base Rate-denominated Term Loans. In

addition, Amendment No. 1 increased the lender commitments under the Revolving Facility from $50.0 million to $75.0

million. Amendment No. 1 also modified certain restrictive covenants of the Credit Agreement, including those relating to

repurchases of other debt securities, permitted acquisitions and payments on equity.

The Company paid $12.3 million in fees and costs related to Amendment No. 1, of which $7.4 million in fees paid to

lenders was recorded as additional discount on debt and $0.8 million of costs related to the increase in the Revolving Facility

was recorded as deferred financing costs. Fees paid to third parties of $4.0 million were recorded as “Debt modification costs”

in the Consolidated Statement of Comprehensive Income for the year ended December 31, 2011.

On February 4, 2013, the Company entered into Amendment No. 2 (“Amendment No. 2”) to the Credit Agreement.

Pursuant to Amendment No. 2, the interest rate margin applicable to LIBOR-based Term Loans was reduced from 3.00% to

2.75%, and the interest rate floors used to determine the LIBOR and Base Rate reference rates for Term Loans was reduced

from 1.25% to 1.00% for LIBOR-based Term Loans and from 2.25% to 2.00% for Base Rate-denominated Term Loans. The

interest rate margin for Revolving Loans was reduced from 3.50% to 1.75% for Base Rate loans and from 4.50% to 2.75%

LIBOR Rate loans. The commitment fee for the unused portion of the Revolving Facility was reduced from 0.75% to 0.50%

and, if the consolidated leverage ratio is reduced below 4.75:1, from 0.50% to 0.375%.

In addition, Amendment No. 2 established the following consolidated leverage ratio thresholds for excess cash flow

prepayments: 50% if the consolidated leverage ratio is 5.75:1 or greater; 25% if the consolidated leverage ratio is less than

5.75:1 and greater than or equal to 5.25:1; and 0% if the consolidated leverage ratio is less than 5.25:1.

Amendment No. 2 revised the definition of excess cash flow to eliminate the deduction for any extraordinary receipts or

disposition proceeds. Finally, Amendment No. 2 revised the definition of certain permitted payments so that the calculation of

allowable restricted payments is performed on a quarterly basis instead of an annual basis that was required prior to

Amendment No. 2. All other material provisions, including maturity and covenants under the Credit Agreement, remain

unchanged.

Fees of $1.3 million paid to third parties in connection with Amendment No. 2 were included as “Debt modification costs”

in the Consolidated Statement of Comprehensive Income for the year ended December 31, 2013.