IBM 2002 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2002 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

|

|

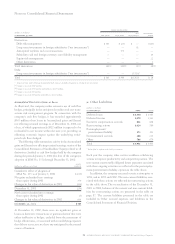

Notes to Consolidated Financial Statements

95international business machines corporation and Subsidiary Companies

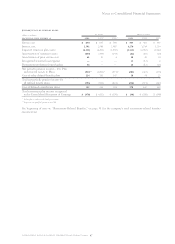

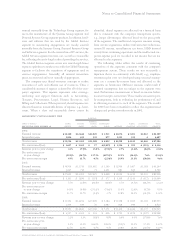

(dollars in millions) u.s. non-u.s. total

for the year ended december 31: 2002 2001 2000 2002 2001 2000 2002 2001 2000

Total retirement-related

plans

—

income $«(154) $«(256) $«(156) $«(17) $«(181) $«(171) $«(171) *$«(437) *$«(327) *

Comprise:

Defined benefit and contribution

pension plans

—

income $«(478) $«(632) $«(530) $«(46) $«(209) $«(198) $«(524) $«(841) $«(728)

Nonpension postretirement

benefits

—

cost 324 376 374 29 28 27 353 404 401

*Includes amounts for discontinued operations costs of $77 million, $56 million and $62 million for 2002, 2001 and 2000, respectively.

company intends to request stockholder approval of a new

ESPP in April 2003. If approved, shares may be issued under

that plan and employee participation would be subject to the

terms and conditions of that plan.

Pro Forma Disclosure

See “Stock-Based Compensation” on page 72, in note a,

“Significant Accounting Policies,” for the pro forma disclo-

sures of net income and earnings per share required under

SFAS No. 123.

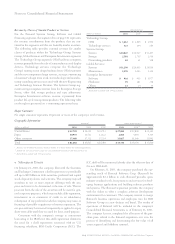

wRetirement-Related Benefits

IBM offers defined benefit pension plans, defined contribution

pension plans and nonpension postretirement plans, primarily

consisting of retiree medical benefits. These benefits form an

important part of the company’s total compensation and

benefits program that is designed to attract and retain highly

skilled and talented employees. The following table provides

the total retirement-related benefit plans’ impact on income

before income taxes.

Accounting Policy

defined benefit pension and

nonpension postretirement benefit plans

The company accounts for its defined benefit pension plans

and its nonpension postretirement benefit plans using actuarial

models required by SFAS No. 87, “Employers’ Accounting

for Pensions,” and SFAS No. 106, “Employers’ Accounting for

Postretirement Benefits Other Than Pensions,” respectively.

These models use an attribution approach that generally

spreads individual events over the service lives of the employ-

ees in the plan. Examples of “events” are plan amendments

and changes in actuarial assumptions such as discount rate,

rate of compensation increases and mortality. See the next

paragraph for information on the expected long-term rate of

return on plan assets. The principle underlying the required

attribution approach is that employees render service over

their service lives on a relatively smooth basis and therefore,

the income statement effects of pensions or nonpension

postretirement benefit plans are earned in, and should follow,

the same pattern.

One of the principal components of the net periodic pen-

sion (income)/cost calculation is the expected long-term rate

of return on plan assets. The required use of expected long-

term rate of return on plan assets may result in recognized

pension income that is greater or less than the actual returns

of those plan assets in any given year. Over time, however, the

expected long-term returns are designed to approximate the

actual long-term returns and therefore result in a pattern of

income and expense recognition that more closely matches the

pattern of the services provided by the employees. Differences

between actual and expected returns are recognized in the

calculation of net periodic pension (income)/cost over five

years as provided for in the accounting rules.

The company uses long-term historical actual return

information, the expected mix of investments that comprise

plan assets, and future estimates of long-term investment

returns to develop its expected return on plan assets.

The discount rate assumptions used for pension and non-

pension postretirement benefit plan accounting reflect the

prevailing rates available on high-quality, fixed-income debt

instruments. The rate of compensation increase is another

significant assumption used in the actuarial model for pension

accounting and is determined by the company, based upon its

long-term plans for such increases. For retiree medical plan

accounting, the company reviews external data and its own

historical trends for health care costs to determine the health

care cost trend rates.

As required by SFAS No. 87, for instances in which pension

plan assets are less than the accumulated benefit obligation

(ABO) as of the end of the reporting period (defined as an

unfunded ABO position), a minimum liability equal to this

difference is established in the Statement of Financial Position.

The ABO is the present value of the actuarially determined

company obligation for pension payments assuming no further

salary increases for the employees. The offset to the mini-

mum liability is a charge to equity, net of tax. In addition, any

prepaid pension asset in excess of unrecognized prior service

cost must be reversed through a net-of-tax charge to equity.

The charge to equity is included in the Accumulated gains

and (losses) not affecting retained earnings section of the

Stockholders’ equity in the Consolidated Statement of

Financial Position.