IBM 2002 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2002 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

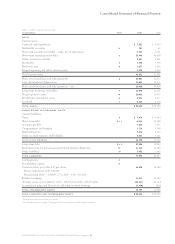

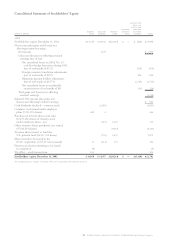

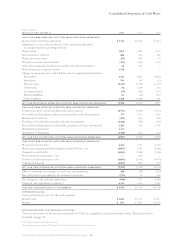

Notes to Consolidated Financial Statements

75international business machines corporation and Subsidiary Companies

Common Stock

Common stock refers to the $.20 par value capital stock as

designated in the company’s Certificate of Incorporation.

Tr easury stock is accounted for using the cost method. When

treasury stock is reissued, the value is computed and recorded

using a weighted-average basis.

Product Warranties

The company estimates its warranty costs based on historical

warranty claim experience and applies this estimate to the

revenue stream for products under warranty. Included in the

company’s warranty accrual are costs for limited warranties

and extended warranty coverage. Future costs for warranties

applicable to revenue recognized in the current period are

charged to cost of revenue. The warranty accrual is reviewed

quarterly to verify that it properly reflects the remaining obli-

gation based on the anticipated expenditures over the balance

of the obligation period. Adjustments are made when actual

warranty claim experience differs from estimates.

Earnings Per Share of Common Stock

Earnings per share of common stock

—

basic is computed by

dividing Net income applicable to common stockholders by the

weighted-average number of common shares outstanding for

the period. Earnings per share of common stock

—

assuming

dilution reflects the maximum potential dilution that could

occur if securities or other contracts to issue common stock

were exercised or converted into common stock and would

then share in the net income of the company. See note t,

“Earnings Per Share of Common Stock,” on page 93 for

additional information.

bAccounting Changes

Standards Implemented

In April 2002, the Financial Accounting Standards Board

(FASB) issued SFAS No. 145, “Rescission of FASB Statements

No. 4, 44 and 64, Amendment of FASB Statement No. 13, and

Technical Corrections,” effective May 15, 2002. SFAS No. 145

eliminates the requirement that gains and losses from the

extinguishment of debt be aggregated and classified as an

extraordinary item, net of tax, and makes certain other tech-

nical corrections. SFAS No. 145 did not have a material effect

on the company’s Consolidated Financial Statements.

Effective January 1, 2002, the company adopted State-

ment of Financial Position (“SOP”) 01-6, “Accounting by

Certain Entities (including entities with Trade Receivables)

That Lend to or Finance the Activities of Others.” With

limited exception, SOP 01-6 applies to any entity that lends

to or finances the activities of, others and provides specialized

guidance for certain transactions specific to financial institu-

tions. This SOP reconciles and conforms, as appropriate, the

accounting and financial reporting guidance established by

the American Institute of Certified Public Accountants. The

adoption did not have a material effect on the company’s

Consolidated Financial Statements.

In October 2001, the FASB issued SFAS No. 144, “Account-

ing for the Impairment or Disposal of Long-Lived Assets.”

SFAS No. 144 addresses significant issues relating to the imple-

mentation of SFAS No. 121, “Accounting for the Impairment

of Long-Lived Assets and for Long-Lived Assets to Be

Disposed Of,” and develops a single accounting model, based

on the framework established in SFAS No. 121 for long-lived

assets to be disposed of by sale, whether such assets are or are

not deemed to be a business. SFAS No. 144 also modifies the

accounting and disclosure rules for discontinued operations.

The standard was adopted on January 1, 2002, and did not have

a material impact on the company’s Consolidated Financial

Statements. The discontinued HDD operations are presented

in the Consolidated Financial Statements in accordance with

the new SFAS No. 144 rules.

In November 2001, the FASB issued Emerging Issues

Task Force (EITF) Issue No. 01-14, “Income Statement

Characterization of Reimbursements Received for ‘Out of

Pocket’ Expenses Incurred.” This guidance requires compa-

nies to recognize the recovery of reimbursable expenses such

as travel costs on services contracts as revenue. These costs

are not to be netted as a reduction of cost. This guidance was

effective January 1, 2002. This guidance did not have a mate-

rial effect on the company’s Consolidated Financial Statements

due to the company’s billing practices. For instance, outside

the United States, almost all of the company’s contracts

involve fixed billings that are designed to recover all costs,

including out-of-pocket costs. Therefore, the “reimbursement”

of these costs is already recorded in revenue.

In July 2001, the FASB issued SFAS No. 141, “Business

Combinations,” and SFAS No. 142, “Goodwill and Other

Intangible Assets.” SFAS No. 141 requires the use of the pur-

chase method of accounting for business combinations and

prohibits the use of the pooling of interests method. Under

the previous rules, the company used the purchase method of

accounting. SFAS No. 141 also refines the definition of intan-

gible assets acquired in a purchase business combination. As a

result, the purchase price allocation of current business com-

binations may be different than the allocation that would have

resulted under the old rules. Business combinations must be

accounted for using SFAS No. 141 effective July 1, 2001.

SFAS No. 142 eliminates the amortization of goodwill,

requires annual impairment testing of goodwill and intro-

duces the concept of indefinite life intangible assets. The

company adopted SFAS No. 142 on January 1, 2002. The new

rules also prohibit the amortization of goodwill associated

with business combinations that closed after June 30, 2001.