IBM 2002 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2002 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

Management Discussion

61international business machines corporation and Subsidiary Companies

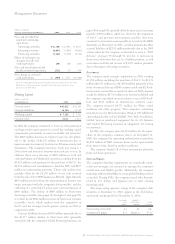

compared to 2000. The increases in 2002 gross profit dollars

and gross profit margin were primarily driven by lower bor-

rowing costs related to the current interest rate environment.

The increase in 2001 was driven by lower borrowing costs

discussed above and improved margins in used equipment

sales due to a mix change to higher margin products.

Global Financing pre-tax income decreased 16.4 percent

in 2002 versus 2001, following a decrease of 2.8 percent in 2001

versus 2000. The decrease in 2002 was driven by an increase in

the provision for bad debts due to the current economic envi-

ronment. See page 62 for an additional discussion of Global

Financing Allowance for Doubtful Accounts. The decrease in

2001 was due to increases in provision for bad debts partially

offset by an increase in gross profit discussed above.

The decline in return on equity from 2001 to 2002 was

due to lower earnings primarily associated with an increased

provision for bad debts expense. The increase in return on

equity from 2000 to 2001 was primarily due to the decline in

the equity balance from 2000 to 2001 as evidenced by the

increase in the debt to equity ratio from 6.6x to 6.8x. See page

62 for a discussion of the allowance for doubtful accounts and

page 63 for a discussion on debt.

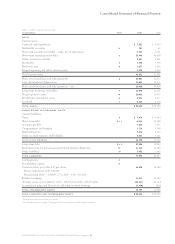

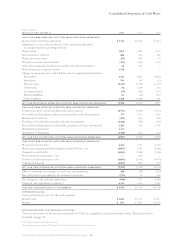

Financial Condition

balance sheet

(dollars in millions)

at december 31: 2002 2001

Cash $«««1,157 $««««««785

Net investment in sales-type leases 12,314 12,903

Equipment under operating leases:

External customers 1,922 2,213

Internal customers*1,701 1,585

Customer loans 9,621 9,486

Total customer financing assets 25,558 26,187

Commercial financing receivables 5,525 6,500

Intercompany financing receivables*1,616 1,883

Other receivables 445 597

Other assets 941 718

Total financing assets $«35,242 $«36,670

Intercompany payables*$«««5,383 $«««4,820

Debt 23,828 25,545

Other liabilities 2,556 2,548

Total financing liabilities 31,767 32,913

Total financing equity 3,475 ««3,757

Total financing liabilities and equity $«35,242 $«36,670

*Amounts eliminated for purposes of IBM’s consolidated results and therefore do not

appear on pages 65 or on page 69. These assets, along with the other assets in this

table, are however, leveraged using Global Financing debt.

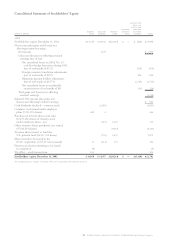

sources and uses of funds

The primary use of funds in Global Financing is to originate

customer and commercial financing assets. Customer financ-

ing assets for end users consist primarily of IBM hardware,

software and services, but also include non-IBM equipment,

software and services to meet IBM customers’ total solutions

requirements. Customer financing assets are primarily sales-

type, direct financing, and operating leases for equipment as

well as loans for software and services with terms generally

for two to five years.

Commercial financing originations arise primarily from

inventory and accounts receivable financing for dealers and

remarketers of IBM and non-IBM products. Payment terms

for inventory financing generally range from 30 to 75 days.

Payment terms for accounts receivable financing generally

range from 30 to 90 days. Also included in commercial financ-

ing assets are syndicated loans.

originations

The following are total external and internal financing

originations.

(dollars in millions)

for the year ended december 31: 2002 2001

Customer finance:

External $«12,845 $«15,620

Internal 1,061 931

Commercial finance 22,546 25,071

Total $«36,452 $«41,622

The decreases in originations were due to a lower demand

for IT equipment associated with the current economic

environment.

Cash collections of both customer and commercial financ-

ing assets exceeded new financing originations in both 2002

and 2001, which resulted in a net decline in financing assets

in these years. Cash collections in 2002 and 2001 included

$218 million and zero, respectively, generated through sales

of portions of Global Financing’s syndicated loan portfolio.

These sales transactions did not have a material impact on the

company’s Consolidated Statement of Earnings. Additionally,

funds were generated through the sale and lease of used equip-

ment sourced primarily from prior years’ lease originations.

Cash generated by Global Financing was deployed to pay

dividends to IBM and to reduce debt.

financing assets by sector

The following are the percentage of external financing assets

by industry sector.

at december 31: 2002 2001

Financial Services 31% 27%

Industrial 18 21

Business Partners*14 13

Communications 12 13

Distribution 11 9

Public 10 12

Other 45

Total 100% 100%

*Business Partner financing assets represent a portion of commercial financing inventory

and accounts receivable financing for terms generally less than 90 days.