Harley Davidson 2012 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2012 Harley Davidson annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

|

|

73

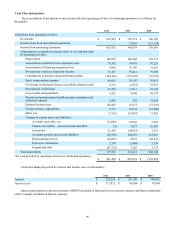

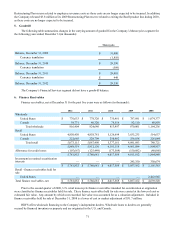

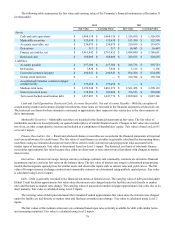

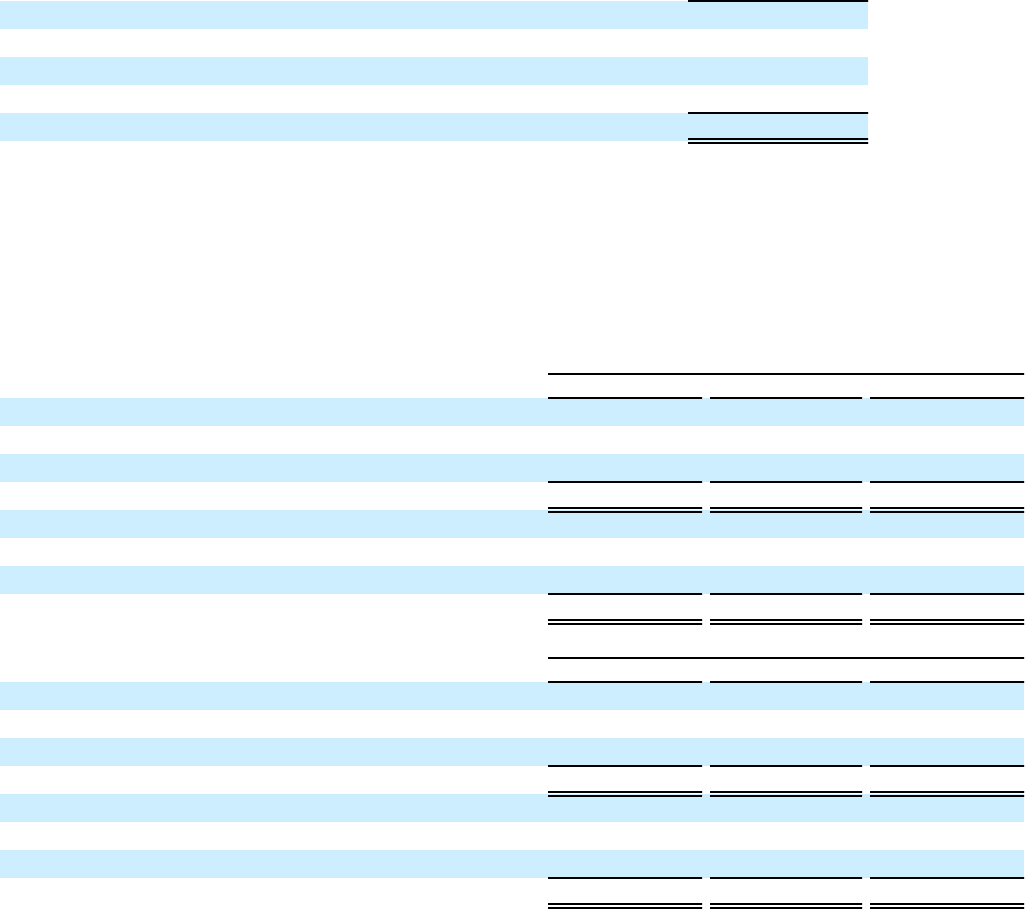

Changes in the allowance for credit losses on finance receivables for the year ended December 31 were as follows (in

thousands):

2010

Balance, beginning of period $ 150,082

Allowance related to newly consolidated finance receivables (1) 49,424

Provision for credit losses 93,118

Charge-offs, net of recoveries (119,035)

Balance, end of period $ 173,589

(1) As a part of the required consolidation of formerly unconsolidated VIEs done in connection with the adoption of the new requirements within ASC

Topics 810 and 860 on January 1, 2010, the Company consolidated a $49.4 million allowance for credit losses related to the newly consolidated

finance receivables.

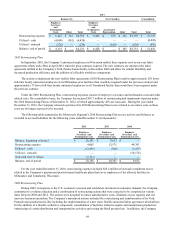

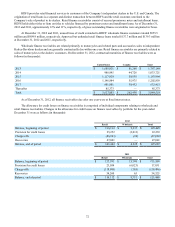

The allowance for credit losses and finance receivables by portfolio, segregated by those amounts that are individually

evaluated for impairment and those that are collectively evaluated for impairment, at December 31, were as follows (in

thousands):

2012

Retail Wholesale Total

Allowance for credit losses, ending balance:

Individually evaluated for impairment $ — $ — $ —

Collectively evaluated for impairment 101,442 6,225 107,667

Total allowance for credit losses $ 101,442 $ 6,225 $ 107,667

Finance receivables, ending balance:

Individually evaluated for impairment $ — $ — $ —

Collectively evaluated for impairment 5,073,115 816,404 5,889,519

Total finance receivables $ 5,073,115 $ 816,404 $ 5,889,519

2011

Retail Wholesale Total

Allowance for credit losses, ending balance:

Individually evaluated for impairment $ — $ — $ —

Collectively evaluated for impairment 116,112 9,337 125,449

Total allowance for credit losses $ 116,112 $ 9,337 $ 125,449

Finance receivables, ending balance:

Individually evaluated for impairment $ — $ — $ —

Collectively evaluated for impairment 5,087,490 824,640 5,912,130

Total finance receivables $ 5,087,490 $ 824,640 $ 5,912,130

Finance receivables are considered impaired when management determines it is probable that the Company will be

unable to collect all amounts due according to the loan agreement. As retail finance receivables are collectively and not

individually reviewed for impairment, this portfolio does not have specifically impaired finance receivables. A specific

allowance is established for wholesale finance receivables determined to be individually impaired in accordance with the

applicable accounting standards when management concludes that the borrower will not be able to make full payment of the

contractual amounts due based on the original terms of the loan agreement. The impairment is determined based on the cash

that the Company expects to receive discounted at the loan’s original interest rate and the fair value of the collateral, if the loan

is collateral-dependent. In establishing the allowance, management considers a number of factors including the specific

borrower’s financial performance as well as ability to repay. At December 31, 2012 and 2011, there were no wholesale finance

receivables that were individually deemed to be impaired under ASC Topic 310, “Receivables”.

Retail finance receivables accrue interest until either collected or charged-off. Interest continues to accrue on past due

wholesale finance receivables until the finance receivable becomes uncollectible, at which time the finance receivable is placed

on non-accrual status. The Company will resume accruing interest on these wholesale finance receivables when payments are

current according to the terms of the loan agreements and future payments are reasonably assured. At December 31, 2012 and

2011, there were no wholesale finance receivables on non-accrual status.