Harley Davidson 2012 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2012 Harley Davidson annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

|

|

72

HDFS provides retail financial services to customers of the Company’s independent dealers in the U.S. and Canada. The

origination of retail loans is a separate and distinct transaction between HDFS and the retail customer, unrelated to the

Company’s sale of product to its dealers. Retail finance receivables consist of secured promissory notes and installment loans.

HDFS holds either titles or liens on titles to vehicles financed by promissory notes and installment loans. As of December 31,

2012 and 2011, approximately 12% and 11%, respectively, of gross outstanding finance receivables were originated in Texas.

At December 31, 2012 and 2011, unused lines of credit extended to HDFS’ wholesale finance customers totaled $955.5

million and $909.9 million, respectively. Approved but unfunded retail finance loans totaled $137.7 million and $139.3 million

at December 31, 2012 and 2011, respectively.

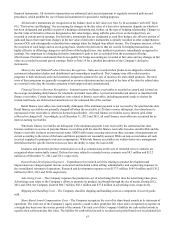

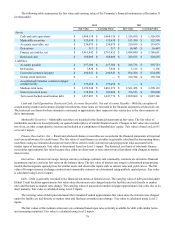

Wholesale finance receivables are related primarily to motorcycles and related parts and accessories sales to independent

Harley-Davidson dealers and are generally contractually due within one year. Retail finance receivables are primarily related to

sales of motorcycles to the dealers’ customers. On December 31, 2012, contractual maturities of finance receivables were as

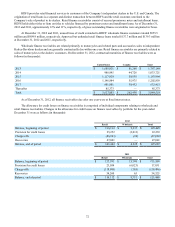

follows (in thousands):

United States Canada Total

2013 $ 1,685,921 $ 81,268 $ 1,767,189

2014 988,995 44,726 1,033,721

2015 1,117,929 50,035 1,167,964

2016 1,146,884 55,975 1,202,859

2017 601,981 30,432 632,413

Thereafter 85,373 — 85,373

Total $ 5,627,083 $ 262,436 $ 5,889,519

As of December 31, 2012, all finance receivables due after one year were at fixed interest rates.

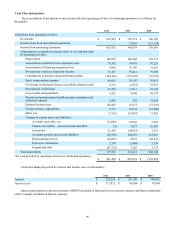

The allowance for credit losses on finance receivables is comprised of individual components relating to wholesale and

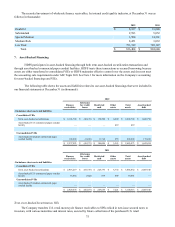

retail finance receivables. Changes in the allowance for credit losses on finance receivables by portfolio for the year ended

December 31 were as follows (in thousands):

2012

Retail Wholesale Total

Balance, beginning of period $ 116,112 $ 9,337 $ 125,449

Provision for credit losses 25,252 (3,013) 22,239

Charge-offs (86,963)(99)(87,062)

Recoveries 47,041 — 47,041

Balance, end of period $ 101,442 $ 6,225 $ 107,667

2011

Retail Wholesale Total

Balance, beginning of period $ 157,791 $ 15,798 $ 173,589

Provision for credit losses 23,054 (6,023) 17,031

Charge-offs (118,993)(503)(119,496)

Recoveries 54,260 65 54,325

Balance, end of period $ 116,112 $ 9,337 $ 125,449