Berkshire Hathaway 2004 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2004 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

|

|

36

Notes to Consolidated Financial Statements (Continued)

(1) Significant accounting policies and practices (Continued)

(m) Deferred charges reinsurance assumed (Continued)

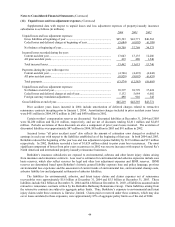

Changes to the expected timing and estimated amount of loss payments produce changes in the unamortized

deferred charge balance. Such changes in estimates are accounted for retrospectively with the net effect

included in amortization expense in the period of the change.

(n) Reinsurance

Provisions for losses and loss adjustment expenses are reported in the accompanying Consolidated

Statements of Earnings after deducting amounts recovered and estimates of amounts recoverable under

reinsurance contracts. Reinsurance contracts do not relieve the ceding company of its obligations to

indemnify policyholders with respect to the underlying insurance and reinsurance contracts.

(o) Insurance premium acquisition costs

Certain costs of acquiring insurance premiums are deferred, subject to ultimate recoverability, and charged

to income as the premiums are earned. Acquisition costs consist of commissions, premium taxes,

advertising and other underwriting costs. The recoverability of premium acquisition costs, generally,

reflects anticipation of investment income. The unamortized balances of deferred premium acquisition

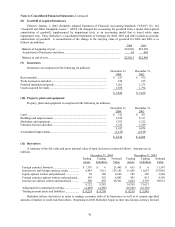

costs are included in other assets and were $1,371 million and $1,278 million at December 31, 2004 and

2003, respectively.

(p) Foreign currency

The accounts of foreign-based subsidiaries are measured in most instances using the local currency as the

functional currency. Revenues and expenses of these businesses are translated into U.S. dollars at the

average exchange rate for the period. Assets and liabilities are translated at the exchange rate as of the

end of the reporting period. Gains or losses from translating the financial statements of foreign-based

operations are included in shareholders’ equity as a component of accumulated other comprehensive

income. Unrealized gains or losses associated with available-for-sale securities are included as a

component of other comprehensive income. Gains and losses arising from other transactions

denominated in a foreign currency are included in the Consolidated Statements of Earnings.

(q) Deferred income taxes

Deferred income taxes are calculated under the liability method. Deferred tax assets and liabilities are

recorded based on differences between the financial statement and tax bases of assets and liabilities at

the enacted tax rates. Changes in deferred income tax assets and liabilities that are associated with

components of other comprehensive income, primarily unrealized investment gains, are charged or

credited directly to other comprehensive income. Otherwise, changes in deferred income tax assets and

liabilities are included as a component of income tax expense.

(r) Accounting pronouncements to be adopted in 2005

In December 2003, the American Institute of Certified Public Accountants issued Statement of Position 03-

3 (“Accounting for Certain Loans or Debt Securities Acquired in a Transfer”) (“SOP 03-3”), which

specifies the accounting and disclosure requirements for loans or debt securities purchased in a transfer

where it is probable that the investor will be unable to collect all contractually required amounts due as a

result of deteriorated credit quality of the issuer. SOP 03-3 also addresses post-acquisition income

recognition with respect to such loans and debt securities. SOP 03-3 is effective for loans or debt

securities acquired in years beginning after December 15, 2004. For loans acquired in years beginning

before December 15, 2004, the provisions of SOP 03-3 related to changes in expected cash flows are to

be applied prospectively. The adoption of SOP 03-3 is not expected to have a material effect on

Berkshire’ s financial statements.

In March 2004 the Emerging Issues Task Force (“EITF”) ratified additional provisions of Issue No. 03-01,

The Meaning of Other-Than-Temporary Impairment and Its Application to Certain Investments. The

provisions of EITF 03-01 ratified in March 2004: (a) define impairments of debt and equity securities

accounted for under SFAS 115, (b) provide criteria to be used by management in judging whether or not

impairments are other-than-temporary, and (c) provide guidance on determining the amount of an

impairment loss. These additional provisions were originally scheduled to be applied prospectively

beginning July 1, 2004. Subsequently, the effective date for applying items (b) and (c) above was

postponed in order to consider implementation issues. The postponed provisions are expected to

become effective during 2005. The adoption of the additional provisions of EITF 03-01 is not expected

to have a material effect on Berkshire’ s financial statements.