Berkshire Hathaway 2004 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2004 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

|

|

34

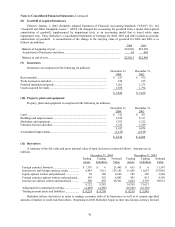

Notes to Consolidated Financial Statements (Continued)

(1) Significant accounting policies and practices (Continued)

(d) Investments (Continued)

Berkshire utilizes the equity method of accounting with respect to investments where it exercises significant

influence, but not control, over the policies of the investee. A voting interest of at least 20% and no

greater than 50% is normally a prerequisite for utilizing the equity method. However Berkshire may

apply the equity method with less than 20% voting interests based upon the facts and circumstances

including representation on the Board of Directors, contractual veto or approval rights, participation in

policy making processes and the existence or absence of other significant owners. Berkshire applies the

equity method to investments in common stock and other investments when such other investments

possess substantially identical subordinated interests to common stock.

In applying the equity method, investments are recorded at cost and subsequently increased or decreased by

the proportionate share of net earnings or losses of the investee. Berkshire also records its proportionate

share of other comprehensive income items of the investee as a component of its comprehensive income.

Dividends or other equity distributions are recorded as a reduction of the investment. In the event that

net losses of the investee have reduced the equity method investment to zero, additional net losses may

be recorded if additional investments in the investee are at-risk, even if Berkshire has not committed to

provide financial support to the investee. Berkshire bases such additional equity method loss amounts, if

any, on the change in its claim on the investee’ s book value.

(e) Loans and finance receivables

Loans and finance receivables consist of commercial and consumer loans originated or purchased by

Berkshire’ s finance and financial products businesses. Loans and finance receivables are not held for

sale and are stated at amortized cost less allowances for uncollectible accounts. Berkshire has the ability

and intent to hold such loans and receivables to maturity. Amortized cost represents acquisition cost,

plus or minus origination and commitment costs paid or fees received which together with acquisition

premiums or discounts are required to be deferred and amortized as yield adjustments over the life of the

loan.

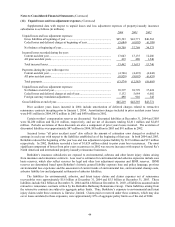

(f) Derivatives

Derivative instruments include interest rate, currency and credit swaps and options, interest rate caps and

floors and futures and forward contracts.

Berkshire carries derivative contracts at estimated fair value. Derivatives are classified as trading account

assets or trading account liabilities in the accompanying Consolidated Balance Sheets and reflect

reductions permitted under master netting agreements with counterparties. The fair values of these

instruments represent the present value of expected future cash flows under the contracts, which are a

function of underlying interest rates, currency rates, security values, related volatility, the

creditworthiness of counterparties and duration of the contracts. Future changes in these factors or a

combination thereof may affect the fair value of these instruments. With minor exception, derivative

contracts are not designated as hedges for accounting purposes. Changes in the fair value of such

contracts are included in the Consolidated Statements of Earnings.

Cash collateral received from or paid to counterparties to secure trading account assets or liabilities is

included in liabilities or assets of finance and financial products businesses in the Consolidated Balance

Sheets. Securities received from counterparties as collateral are not recorded as assets and securities

delivered to counterparties as collateral continue to be reflected as assets in the Consolidated Balance

Sheets.

(g) Securities sold under agreements to repurchase

Securities sold under agreements to repurchase are accounted for as collateralized borrowings and are

recorded at the contractual repurchase amounts.

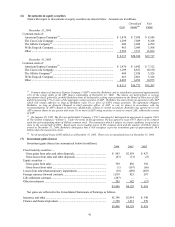

(h) Inventories

Inventories are stated at the lower of cost or market. Cost with respect to manufactured goods includes raw

materials, direct and indirect labor and factory overhead. As of December 31, 2004, approximately 61%

of the total inventory cost was determined using the last-in-first-out (“LIFO”) method, 29% using the

first-in-first-out (“FIFO”) method, with the remainder using the specific identification method. With

respect to inventories carried at LIFO cost, the aggregate difference in value between LIFO cost and cost

determined under FIFO methods was $115 million and $23 million as of December 31, 2004 and

December 31, 2003, respectively.