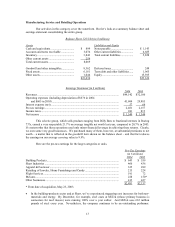

Berkshire Hathaway 2004 Annual Report Download - page 24

Download and view the complete annual report

Please find page 24 of the 2004 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

|

|

On such questions, the interests of the CEO may well differ from those of the shareholders.

Directors, moreover, sometimes lack the knowledge or gumption to overrule the CEO. Therefore,

it’ s vital that large owners focus on these three questions and speak up when necessary.

Instead many simply follow a “checklist” approach to the issue du jour. Last year I was on the

receiving end of a judgment reached in that manner. Several institutional shareholders and their

advisors decided I lacked “independence” in my role as a director of Coca-Cola. One group

wanted me removed from the board and another simply wanted me booted from the audit

committee.

My first impulse was to secretly fund the group behind the second idea. Why anyone would wish

to be on an audit committee is beyond me. But since directors must be assigned to one committee

or another, and since no CEO wants me on his compensation committee, it’ s often been my lot to

get an audit committee assignment. As it turned out, the institutions that opposed me failed and I

was re-elected to the audit job. (I fought off the urge to ask for a recount.)

Some institutions questioned my “independence” because, among other things, McLane and Dairy

Queen buy lots of Coke products. (Do they want us to favor Pepsi?) But independence is defined

in Webster’ s as “not subject to control by others.” I’ m puzzled how anyone could conclude that

our Coke purchases would “control” my decision-making when the counterweight is the well-

being of $8 billion of Coke stock held by Berkshire. Assuming I’ m even marginally rational,

elementary arithmetic should make it clear that my heart and mind belong to the owners of Coke,

not to its management.

I can’ t resist mentioning that Jesus understood the calibration of independence far more clearly

than do the protesting institutions. In Matthew 6:21 He observed: “For where your treasure is,

there will your heart be also.” Even to an institutional investor, $8 billion should qualify as

“treasure” that dwarfs any profits Berkshire might earn on its routine transactions with Coke.

Measured by the biblical standard, the Berkshire board is a model: (a) every director is a member

of a family owning at least $4 million of stock; (b) none of these shares were acquired from

Berkshire via options or grants; (c) no directors receive committee, consulting or board fees from

the company that are more than a tiny portion of their annual income; and (d) although we have a

standard corporate indemnity arrangement, we carry no liability insurance for directors.

At Berkshire, board members travel the same road as shareholders.

* * * * * * * * * * * *

Charlie and I have seen much behavior confirming the Bible’ s “treasure” point. In our view,

based on our considerable boardroom experience, the least independent directors are likely to be

those who receive an important fraction of their annual income from the fees they receive for

board service (and who hope as well to be recommended for election to other boards and thereby

to boost their income further). Yet these are the very board members most often classed as

“independent.”

Most directors of this type are decent people and do a first-class job. But they wouldn’ t be human

if they weren’ t tempted to thwart actions that would threaten their livelihood. Some may go on to

succumb to such temptations.

Let’ s look at an example based upon circumstantial evidence. I have first-hand knowledge of a

recent acquisition proposal (not from Berkshire) that was favored by management, blessed by the

company’ s investment banker and slated to go forward at a price above the level at which the

stock had sold for some years (or now sells for). In addition, a number of directors favored the

transaction and wanted it proposed to shareholders.

23