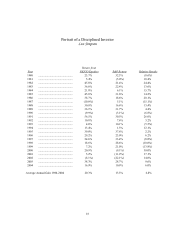

Berkshire Hathaway 2004 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2004 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

|

|

Several of their brethren, however, each of whom received board and committee fees totaling

about $100,000 annually, scuttled the proposal, which meant that shareholders never learned of

this multi-billion offer. Non-management directors owned little stock except for shares they had

received from the company. Their open-market purchases in recent years had meanwhile been

nominal, even though the stock had sold far below the acquisition price proposed. In other words,

these directors didn’ t want the shareholders to be offered X even though they had consistently

declined the opportunity to buy stock for their own account at a fraction of X.

I don’ t know which directors opposed letting shareholders see the offer. But I do know that

$100,000 is an important portion of the annual income of some of those deemed “independent,”

clearly meeting the Matthew 6:21 definition of “treasure.” If the deal had gone through, these fees

would have ended.

Neither the shareholders nor I will ever know what motivated the dissenters. Indeed they

themselves will not likely know, given that self-interest inevitably blurs introspection. We do

know one thing, though: At the same meeting at which the deal was rejected, the board voted itself

a significant increase in directors’ fees.

• While we are on the subject of self-interest, let’ s turn again to the most important accounting

mechanism still available to CEOs who wish to overstate earnings: the non-expensing of stock

options. The accomplices in perpetuating this absurdity have been many members of Congress

who have defied the arguments put forth by all Big Four auditors, all members of the Financial

Accounting Standards Board and virtually all investment professionals.

I’ m enclosing an op-ed piece I wrote for The Washington Post describing a truly breathtaking bill

that was passed 312-111 by the House last summer. Thanks to Senator Richard Shelby, the Senate

didn’ t ratify the House’ s foolishness. And, to his great credit, Bill Donaldson, the investor-

minded Chairman of the SEC, has stood firm against massive political pressure, generated by the

check-waving CEOs who first muscled Congress in 1993 about the issue of option accounting and

then repeated the tactic last year.

Because the attempts to obfuscate the stock-option issue continue, it’ s worth pointing out that no

one – neither the FASB, nor investors generally, nor I – are talking about restricting the use of

options in any way. Indeed, my successor at Berkshire may well receive much of his pay via

options, albeit logically-structured ones in respect to 1) an appropriate strike price, 2) an escalation

in price that reflects the retention of earnings, and 3) a ban on his quickly disposing of any shares

purchased through options. We cheer arrangements that motivate managers, whether these be

cash bonuses or options. And if a company is truly receiving value for the options it issues, we

see no reason why recording their cost should cut down on their use.

The simple fact is that certain CEOs know their own compensation would be far more rationally

determined if options were expensed. They also suspect that their stock would sell at a lower price

if realistic accounting were employed, meaning that they would reap less in the market when they

unloaded their personal holdings. To these CEOs such unpleasant prospects are a fate to be fought

with all the resources they have at hand – even though the funds they use in that fight normally

don’ t belong to them, but are instead put up by their shareholders.

Option-expensing is scheduled to become mandatory on June 15th. You can therefore expect

intensified efforts to stall or emasculate this rule between now and then. Let your Congressman

and Senators know what you think on this issue.

24