Berkshire Hathaway 2003 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2003 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

|

|

66

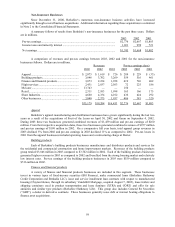

Management’s Discussion (Continued)

Interest Rate Risk (Continued)

interest rate sensitive instruments may be affected by the creditworthiness of the issuer, prepayment options, relative

values of alternative investments, the liquidity of the instrument and other general market conditions. Fixed interest

rate investments may be more sensitive to interest rate changes than variable rate investments.

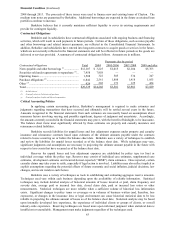

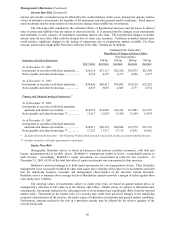

The following table summarizes the estimated effects of hypothetical increases and decreases in interest

rates on assets and liabilities that are subject to interest rate risk. It is assumed that the changes occur immediately

and uniformly to each category of instrument containing interest rate risks. The hypothetical changes in market

interest rates do not reflect what could be deemed best or worst case scenarios. Variations in market interest rates

could produce significant changes in the timing of repayments due to prepayment options available. For these

reasons, actual results might differ from those reflected in the table. Dollars are in millions.

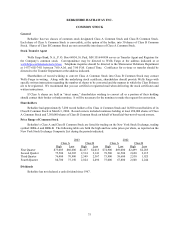

Estimated Fair Value after

Hypothetical Change in Interest Rates

(bp=basis points)

Insurance and other businesses 100 bp 100 bp 200 bp 300 bp

Fair Value decrease increase increase increase

As of December 31, 2003

Investments in securities with fixed maturities ..... $26,116 $27,113 $25,220 $24,333 $23,550

Notes payable and other borrowings..................... 4,334 4,397 4,277 4,226 4,177

As of December 31, 2002

Investments in securities with fixed maturities ..... $38,096 $40,411 $36,087 $34,129 $32,262

Notes payable and other borrowings..................... 4,925 5,010 4,847 4,777 4,712

Finance and financial products businesses *

As of December 31, 2003

Investments in securities with fixed maturities

and loans and finance receivables ...................... $14,573 $14,905 $14,323 $13,987 $13,557

Notes payable and other borrowings **................ 11,617 11,838 11,419 11,244 11,079

As of December 31, 2002

Investments in securities with fixed maturities

and loans and finance receivables ...................... $20,011 $20,152 $20,062 $19,779 $19,161

Notes payable and other borrowings **................ 17,237 17,317 17,112 17,032 16,962

*Excludes General Re Securities – See Financial Products Risk section for discussion of risks associated with this business.

** Includes securities sold under agreements to repurchase.

Equity Price Risk

Strategically, Berkshire strives to invest in businesses that possess excellent economics, with able and

honest management and at sensible prices. Berkshire’ s management prefers to invest a meaningful amount in

each investee. Accordingly, Berkshire’ s equity investments are concentrated in relatively few investees. At

December 31, 2003, 68.9% of the total fair value of equity investments was concentrated in four investees.

Berkshire’ s preferred strategy is to hold equity investments for very long periods of time. Thus, Berkshire

management is not necessarily troubled by short term equity price volatility with respect to its investments provided

that the underlying business, economic and management characteristics of the investees remain favorable.

Berkshire strives to maintain above average levels of shareholder capital to provide a margin of safety against short

term equity price volatility.

The carrying values of investments subject to equity price risks are based on quoted market prices or

management’ s estimates of fair value as of the balance sheet dates. Market prices are subject to fluctuation and,

consequently, the amount realized in the subsequent sale of an investment may significantly differ from the reported

market value. Fluctuation in the market price of a security may result from perceived changes in the underlying

economic characteristics of the investee, the relative price of alternative investments and general market conditions.

Furthermore, amounts realized in the sale of a particular security may be affected by the relative quantity of the

security being sold.