Berkshire Hathaway 2003 Annual Report Download - page 16

Download and view the complete annual report

Please find page 16 of the 2003 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

|

|

15

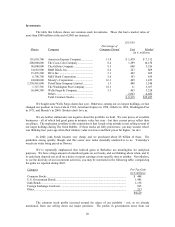

Finance and Financial Products

This sector includes a wide-ranging group of activities. Here’ s some commentary on the most

important.

• I manage a few opportunistic strategies in AAA fixed-income securities that have been quite

profitable in the last few years. These opportunities come and go – and at present, they are

going. We sped their departure somewhat last year, thereby realizing 24% of the capital gains

we show in the table that follows.

Though far from foolproof, these transactions involve no credit risk and are conducted in

exceptionally liquid securities. We therefore finance the positions almost entirely with

borrowed money. As the assets are reduced, so also are the borrowings. The smaller

portfolio we now have means that in the near future our earnings in this category will decline

significantly. It was fun while it lasted, and at some point we’ ll get another turn at bat.

• A far less pleasant unwinding operation is taking place at Gen Re Securities, the trading and

derivatives operation we inherited when we purchased General Reinsurance.

When we began to liquidate Gen Re Securities in early 2002, it had 23,218 outstanding tickets

with 884 counterparties (some having names I couldn’ t pronounce, much less

creditworthiness I could evaluate). Since then, the unit’ s managers have been skillful and

diligent in unwinding positions. Yet, at yearend – nearly two years later – we still had 7,580

tickets outstanding with 453 counterparties. (As the country song laments, “How can I miss

you if you won’ t go away?”)

The shrinking of this business has been costly. We’ ve had pre-tax losses of $173 million in

2002 and $99 million in 2003. These losses, it should be noted, came from a portfolio of

contracts that – in full compliance with GAAP – had been regularly marked-to-market with

standard allowances for future credit-loss and administrative costs. Moreover, our liquidation

has taken place both in a benign market – we’ ve had no credit losses of significance – and in

an orderly manner. This is just the opposite of what might be expected if a financial crisis

forced a number of derivatives dealers to cease operations simultaneously.

If our derivatives experience – and the Freddie Mac shenanigans of mind-blowing size and

audacity that were revealed last year – makes you suspicious of accounting in this arena,

consider yourself wised up. No matter how financially sophisticated you are, you can’ t

possibly learn from reading the disclosure documents of a derivatives-intensive company

what risks lurk in its positions. Indeed, the more you know about derivatives, the less you

will feel you can learn from the disclosures normally proffered you. In Darwin’ s words,

“Ignorance more frequently begets confidence than does knowledge.”

* * * * * * * * * * * *

And now it’ s confession time: I’ m sure I could have saved you $100 million or so, pre-tax, if I

had acted more promptly to shut down Gen Re Securities. Both Charlie and I knew at the

time of the General Reinsurance merger that its derivatives business was unattractive.

Reported profits struck us as illusory, and we felt that the business carried sizable risks that

could not effectively be measured or limited. Moreover, we knew that any major problems

the operation might experience would likely correlate with troubles in the financial or

insurance world that would affect Berkshire elsewhere. In other words, if the derivatives

business were ever to need shoring up, it would commandeer the capital and credit of

Berkshire at just the time we could otherwise deploy those resources to huge advantage. (A

historical note: We had just such an experience in 1974 when we were the victim of a major

insurance fraud. We could not determine for some time how much the fraud would ultimately

cost us and therefore kept more funds in cash-equivalents than we normally would have.