The Hartford 2012 Annual Report Download - page 226

Download and view the complete annual report

Please find page 226 of the 2012 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

|

|

Table of Contents

The domestic insurance subsidiaries of The Hartford prepare their statutory financial statements in conformity with statutory accounting practices prescribed

or permitted by the applicable state insurance department which vary materially from U.S. GAAP. Prescribed statutory accounting practices include

publications of the National Association of Insurance Commissioners (“NAIC”), as well as state laws, regulations and general administrative rules. The

differences between statutory financial statements and financial statements prepared in accordance with U.S. GAAP vary between domestic and foreign

jurisdictions. The principal differences are that statutory financial statements do not reflect deferred policy acquisition costs and limit deferred income taxes,

life benefit reserves predominately use interest rate and mortality assumptions prescribed by the NAIC, bonds are generally carried at amortized cost and

reinsurance assets and liabilities are presented net of reinsurance.

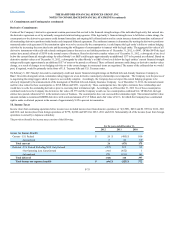

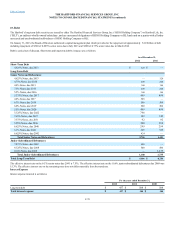

The statutory net income (loss) and surplus was as follows:

U.S. life insurance subsidiaries, includes domestic captive insurance subsidiaries $592 $ (1,272) $ (140)

Property and casualty insurance subsidiaries 883 514 1,477

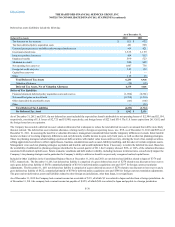

U.S. life insurance subsidiaries, includes domestic captive insurance subsidiaries $ 6,410 $ 7,388

Property and casualty insurance subsidiaries 7,645 7,412

The Company also holds regulatory capital and surplus for its operations in Japan. Under the accounting practices and procedures governed by Japanese

regulatory authorities, the Company’s statutory capital and surplus was $1.1 billion and $1.3 billion, as of December 31, 2012 and 2011, respectively.

Regulatory Capital Requirements

The Hartford's U.S. insurance companies' states of domicile impose risk-based capital (“RBC”) requirements. The requirements provide a means of

measuring the minimum amount of statutory surplus appropriate for an insurance company to support its overall business operations based on its size and

risk profile. Regulatory compliance is determined by a ratio of a company's total adjusted capital (“TAC”) to its authorized control level RBC (“ACL RBC”).

Companies below specific trigger points or ratios are classified within certain levels, each of which requires specified corrective action. The minimum level of

TAC before corrective action commences is two times the ACL RBC (“Company Action Level”). The adequacy of a company's capital is determined by the

ratio of a company's TAC to its Company Action Level (known as the RBC ratio). All of The Hartford's operating insurance subsidiaries had RBC ratios in

excess of the minimum levels required by the applicable insurance regulations.

Similar to the RBC ratios that are employed by U.S. insurance regulators, regulatory authorities in the international jurisdictions in which The Hartford

operates generally establish minimum solvency requirements for insurance companies. All of The Hartford's international insurance subsidiaries have

solvency margins in excess of the minimum levels required by the applicable regulatory authorities.

F-84