The Hartford 2012 Annual Report Download - page 217

Download and view the complete annual report

Please find page 217 of the 2012 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

|

|

Table of Contents

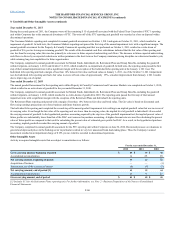

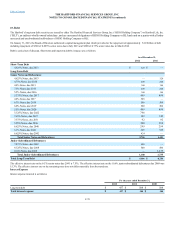

Certain of the Company’s derivative agreements contain provisions that are tied to the financial strength ratings of the individual legal entity that entered into

the derivative agreement as set by nationally recognized statistical rating agencies. If the legal entity’s financial strength were to fall below certain ratings, the

counterparties to the derivative agreements could demand immediate and ongoing full collateralization and in certain instances demand immediate settlement of

all outstanding derivative positions traded under each impacted bilateral agreement. The settlement amount is determined by netting the derivative positions

transacted under each agreement. If the termination rights were to be exercised by the counterparties; it could impact the legal entity’s ability to conduct hedging

activities by increasing the associated costs and decreasing the willingness of counterparties to transact with the legal entity. The aggregate fair value of all

derivative instruments with credit-risk-related contingent features that are in a net liability position as of December 31, 2012, is $643. Of this $643 the legal

entities have posted collateral of $589 in the normal course of business. Based on derivative market values as of December 31, 2012, a downgrade of one level

below the current financial strength ratings by either Moody’s or S&P could require approximately an additional $37 to be posted as collateral. Based on

derivative market values as of December 31, 2012, a downgrade by either Moody’s or S&P of two levels below the legal entities’ current financial strength

ratings could require approximately an additional $57 of assets to be posted as collateral. These collateral amounts could change as derivative market values

change, as a result of changes in our hedging activities or to the extent changes in contractual terms are negotiated. The nature of the collateral that we would

post, if required, would be primarily in the form of U.S. Treasury bills and U.S. Treasury notes.

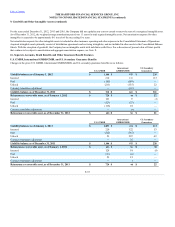

On February 5, 2013 Moody's lowered its counterparty credit and insurer financial strength ratings on Hartford Life and Annuity Insurance Company to

Baa2. Given this downgrade action, termination rating triggers in seven derivative counterparty relationships were impacted. The Company is in the process of

re-negotiating the rating triggers which it expects to successfully complete. Accordingly, the Company does not expect the current hedging programs to be

adversely impacted by the announcement of the downgrade of Hartford Life and Annuity Insurance Company. As of December 31, 2012, the notional amount

and fair value related to these counterparties is $18.8 billion and $331, respectively. These counterparties have the right to terminate these relationships and

would have to settle the outstanding derivatives prior to exercising their termination right. Accordingly, as of December 31, 2012 five of these counterparties

combined would owe the Company the derivatives fair value of $ 375 and the Company would owe two counterparties combined $ 44. Of this $44, the legal

entities have posted collateral of $33 in the normal course of business. The counterparties have not exercised this termination right. The notional and fair value

amounts include a customized GMWB derivative with a notional amount of $ 3.9 billion and a fair value of $133, for which the Company has a contractual

right to make a collateral payment in the amount of approximately $ 45 to prevent its termination.

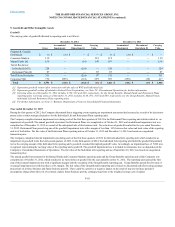

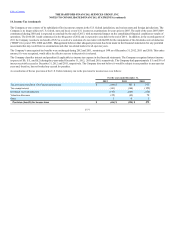

Income (loss) from continuing operations before income taxes included income (loss) from domestic operations of $(1,305), $481 and $1,998 for 2012, 2011

and 2010, and income (loss) from foreign operations of $778, $(180) and $274 for 2012, 2011 and 2010. Substantially all of the income (loss) from foreign

operations is earned by a Japanese subsidiary.

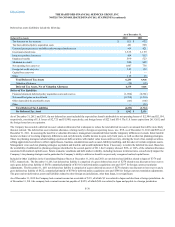

The provision (benefit) for income taxes consists of the following:

Current - U.S. Federal $20 $ (495) $ 106

- International 6 22 69

Deferred - U.S. Federal Excluding NOL Carryforward (377)921 93

- Net Operating Loss Carryforward (301)(652) 1

- International 158 (121)303

F-75