The Hartford 2012 Annual Report Download - page 132

Download and view the complete annual report

Please find page 132 of the 2012 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

|

|

Table of Contents

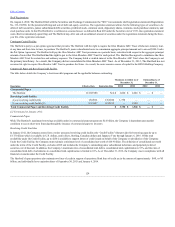

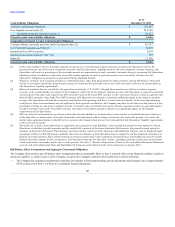

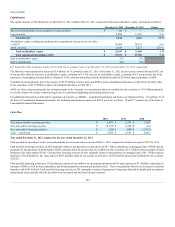

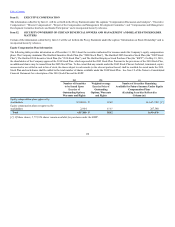

Statutory Surplus

The table below sets forth statutory surplus for the Company’s insurance companies as of December 31, 2012 and 2011:

U.S. life insurance subsidiaries, includes domestic captive insurance subsidiaries $ 6,410 $ 7,388

Property and casualty insurance subsidiaries 7,645 7,412

Statutory capital and surplus for the U.S. life insurance subsidiaries, including domestic captive insurance subsidiaries, decreased by $978, primarily due

to variable annuity surplus impacts of approximately $425, a $200 increase in reserves on a change in valuation basis, $200 transfer of the Mutual Funds

business from the U.S. life insurance companies to the life holding company, and an increase in the asset valuation reserve of $115. As a result of the

January 2013 statutory gain from the sale of the Retirement Plans and Individual Life businesses, the Company's pro forma January 2, 2013 U.S. life

statutory surplus was estimated to be $8.1 billion, before approximately $1.5 billion in extraordinary dividends and return of capital to HFSG Holding

Company.

Statutory capital and surplus for the property and casualty insurance subsidiaries increased by $233, primarily due to statutory net income, after tax, of

$727, unrealized gains of $249, and an increase in statutory admitted deferred tax assets of $77, capital contributions of $14, and an increase of statutory

admitted assets of $7, partially offset by dividends to the HFSG Holding Company of $841. Both net income and dividends are net of interest payments and

dividends, respectively, on an intercompany note between Hartford Holdings, Inc. and Hartford Fire Insurance Company.

The Company also holds regulatory capital and surplus for its operations in Japan. Under the accounting practices and procedures governed by Japanese

regulatory authorities, the Company’s statutory capital and surplus was $1.1 billion and $1.3 billion as of December 31, 2012 and 2011, respectively.

The Company’s stockholders’ equity, as prepared using U.S. generally accepted accounting principles (“U.S. GAAP”) was $22.4 billion as of December 31,

2012. The Company’s estimated aggregate statutory capital and surplus, as prepared in accordance with the National Association of Insurance

Commissioners’ Accounting Practices and Procedures Manual (“U.S. STAT”) was $14.1 billion as of December 31, 2012. Significant differences between

U.S. GAAP stockholders’ equity and aggregate statutory capital and surplus prepared in accordance with U.S. STAT include the following:

•U.S. STAT excludes equity of non-insurance and foreign insurance subsidiaries not held by U.S. insurance subsidiaries.

•Costs incurred by the Company to acquire insurance policies are deferred under U.S. GAAP while those costs are expensed immediately under U.S.

STAT.

•Temporary differences between the book and tax basis of an asset or liability which are recorded as deferred tax assets are evaluated for recoverability

under U.S. GAAP while those amounts deferred are subject to limitations under U.S. STAT.

•The assumptions used in the determination of Life benefit reserves is prescribed under U.S. STAT, while the assumptions used under U.S. GAAP are

generally the Company’s best estimates. The methodologies for determining life insurance reserve amounts may also be different. For example, reserving

for living benefit reserves under U.S. STAT is generally addressed by the Commissioners’ Annuity Reserving Valuation Methodology and the related

Actuarial Guidelines, while under U.S. GAAP, those same living benefits may be considered embedded derivatives and recorded at fair value or they

may be considered SOP 03-1 reserves. The sensitivity of these life insurance reserves to changes in equity markets, as applicable, will be different

between U.S. GAAP and U.S. STAT.

•The difference between the amortized cost and fair value of fixed maturity and other investments, net of tax, is recorded as an increase or decrease to the

carrying value of the related asset and to equity under U.S. GAAP, while U.S. STAT only records certain securities at fair value, such as equity

securities and certain lower rated bonds required by the NAIC to be recorded at the lower of amortized cost or fair value.

•U.S. STAT for life insurance companies establishes a formula reserve for realized and unrealized losses due to default and equity risks associated with

certain invested assets (the Asset Valuation Reserve), while U.S. GAAP does not. Also, for those realized gains and losses caused by changes in interest

rates, U.S. STAT for life insurance companies defers and amortizes the gains and losses, caused by changes in interest rates, into income over the

original life to maturity of the asset sold (the Interest Maintenance Reserve) while U.S. GAAP does not.

•Goodwill arising from the acquisition of a business is tested for recoverability on an annual basis (or more frequently, as necessary) for U.S. GAAP,

while under U.S. STAT goodwill is amortized over a period not to exceed 10 years and the amount of goodwill is limited.

131