The Hartford 2012 Annual Report Download - page 178

Download and view the complete annual report

Please find page 178 of the 2012 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

|

|

Table of Contents

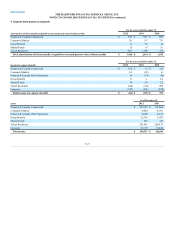

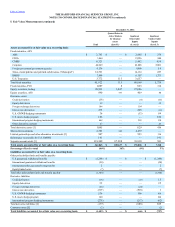

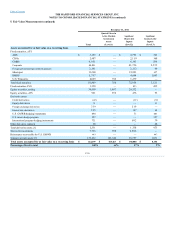

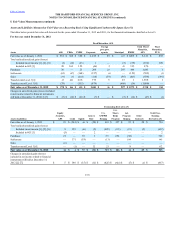

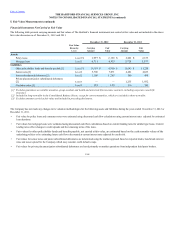

Securities and derivatives for which the Company bases fair value on broker quotations predominately include ABS, CDOs, corporate, fixed maturities, FVO

and certain credit derivatives. Due to the lack of transparency in the process brokers use to develop prices for these investments, the Company does not have

access to the significant unobservable inputs brokers use to price these securities and derivatives. The Company believes however, the types of inputs brokers

may use would likely be similar to those used to price securities and derivatives for which inputs are available to the Company, and therefore may include,

but not be limited to, loss severity rates, constant prepayment rates, constant default rates and credit spreads. Therefore, similar to non broker priced

securities and derivatives, generally, increases in these inputs would cause fair values to decrease. For the year ended December 31, 2012, no significant

adjustments were made by the Company to broker prices received.

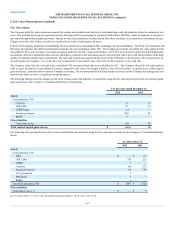

Excluded from the tables above are limited partnerships and other alternative investments which total $314 of level 3 assets measured at fair value. The

predominant valuation method uses a NAV calculated on a monthly basis and represents funds where the Company does not have the ability to redeem the

investment in the near-term at that NAV, including an assessment of the investee's liquidity.

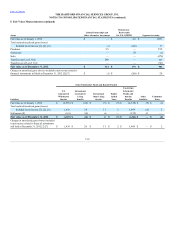

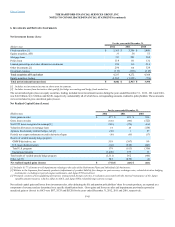

Product Derivatives

The Company formerly offered certain variable annuity products with GMWB riders in the U.S., U.K. and Japan. The GMWB provides the policyholder

with a guaranteed remaining balance ("GRB") if the account value is reduced to zero through a combination of market declines and withdrawals. The GRB is

generally equal to premiums less withdrawals. Certain contract provisions can increase the GRB at contractholder election or after the passage of time. The

GMWB represents an embedded derivative in the variable annuity contract. When it is determined that (1) the embedded derivative possesses economic

characteristics that are not clearly and closely related to the economic characteristics of the host contract, and (2) a separate instrument with the same terms

would qualify as a derivative instrument, the embedded derivative is bifurcated from the host for measurement purposes. The embedded derivative is carried

at fair value, with changes in fair value reported in net realized capital gains and losses. The Company’s GMWB liability is reported in other policyholder

funds and benefits payable in the Consolidated Balance Sheets. The notional value of the embedded derivative is the GRB.

In valuing the embedded derivative, the Company attributes to the derivative a portion of the expected fees to be collected over the expected life of the contract

from the contract holder equal to the present value of future GMWB claims (the “Attributed Fees”). The excess of fees collected from the contract holder in the

current period over the current period’s Attributed Fees are associated with the host variable annuity contract and reported in fee income.

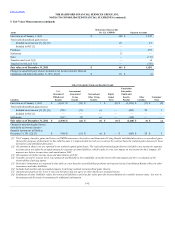

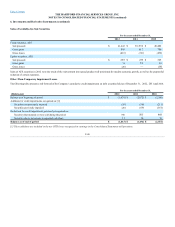

U.S. GMWB Reinsurance Derivative

The Company has reinsurance arrangements in place to transfer a portion of its risk of loss due to GMWB. These arrangements are recognized as derivatives

and carried at fair value in reinsurance recoverables. Changes in the fair value of the reinsurance agreements are reported in net realized capital gains and

losses.

The fair value of the U.S. GMWB reinsurance derivative is calculated as an aggregation of the components described in the Living Benefits Required to be

Fair Valued discussion below and is modeled using significant unobservable policyholder behavior inputs, identical to those used in calculating the underlying

liability, such as lapses, fund selection, resets and withdrawal utilization and risk margins.

F-36