The Hartford 2012 Annual Report Download - page 122

Download and view the complete annual report

Please find page 122 of the 2012 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

|

|

Table of Contents

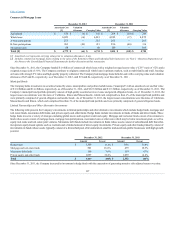

In addition to the credit impairments recognized in earnings, the Company recognized non-credit impairments in other comprehensive income of $ 40 for the

year ended December 31, 2012, predominantly concentrated in corporate financial services and RMBS. These non-credit impairments represent the difference

between fair value and the Company’s best estimate of expected future cash flows discounted at the security’s effective yield prior to impairment, rather than at

current market implied credit spreads. These non-credit impairments primarily represent increases in market liquidity premiums and credit spread widening

that occurred after the securities were purchased, as well as a discount for variable-rate coupons which are paying less than at purchase date. In general, larger

liquidity premiums and wider credit spreads are the result of deterioration of the underlying collateral performance of the securities, as well as the risk

premium required to reflect future uncertainty in the real estate market.

Future impairments may develop as the result of changes in intent to sell specific securities or if actual results underperform current modeling assumptions,

which may be the result of, but are not limited to, macroeconomic factors and security-specific performance below current expectations. Ultimate loss

formation will be a function of macroeconomic factors and idiosyncratic security-specific performance. As a result, it is difficult to predict future impairments

with accuracy.

Year ended December 31, 2011

For the year ended December 31, 2011, impairments recognized in earnings were comprised of credit impairments of $ 125, primarily concentrated on

structured securities associated with commercial real estate, as well as direct private investments. Also included were impairments on debt securities for which

the Company intended to sel1 of $32, mainly comprised of corporate bonds, certain ABS aircraft bonds and CMBS as market pricing improved, as well as

impairments on equity securities of $17 primarily related to preferred stock associated with direct private investments.

Year ended December 31, 2010

Impairments recognized in earnings were comprised of credit impairments of $372 primarily concentrated on structured securities associated with commercial

and residential real estate. Also included were impairments on debt securities for which the Company intended to sell of $54, mainly comprised of CMBS

bonds in order to take advantage of price appreciation, as well as impairments on equity securities of $8 primarily on below investment grade securities

depressed 20% for more than six months.

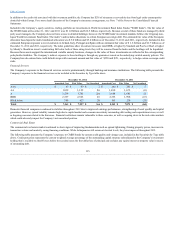

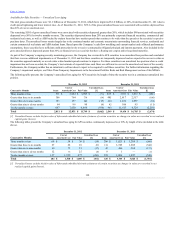

Valuation Allowances on Mortgage Loans

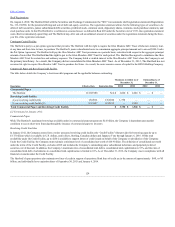

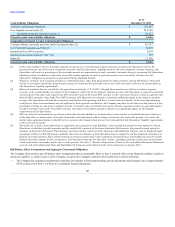

The following table presents (additions)/reversals to valuation allowances on mortgage loans.

Credit-related concerns $14 $ 27 $ (70)

Held for sale

Agricultural loans —(3)(10)

B-note participations — — (22)

Mezzanine loans — — (52)

Year ended December 31, 2012

For the year ended December 31, 2012, valuation allowances on mortgage loan reversals of $14 were largely driven by recovery of the property collateralizing a

B-Note. The valuation allowance was reversed due to an increase in the valuation of the underlying collateral as a result of improved occupancy rates and

performance of the property. Continued improvement in commercial real estate property valuations will positively impact future loss development, with future

impairments driven by idiosyncratic loan-specific performance.

Year ended December 31, 2011

For the year ended December 31, 2011, valuation allowances on mortgage loan additions of $24 were largely driven by the release of a reserve associated with

the sale of a previously reserved for mezzanine loan. Excluded from the table above are valuation allowances associated with mortgage loans related to the

divestiture of Federal Trust Corporation. For further information regarding the divestiture of Federal Trust Corporation, see Note 20 of the Notes to the

Consolidated Financial Statements.

Year ended December 31, 2010

For the years ended December 31, 2010, valuation allowances on mortgage loan additions of $(154), primarily related to B-Note participant and mezzanine

loan sales. Also included were additions for expected credit losses due to borrower financial difficulty and/or collateral deterioration.

121