The Hartford 2012 Annual Report Download - page 203

Download and view the complete annual report

Please find page 203 of the 2012 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

|

|

Table of Contents

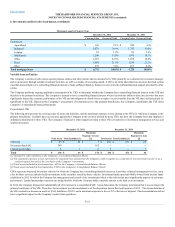

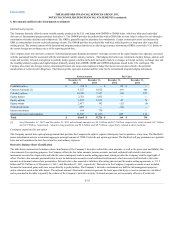

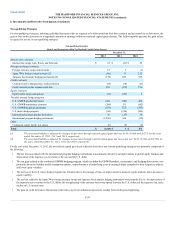

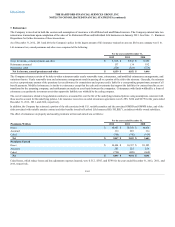

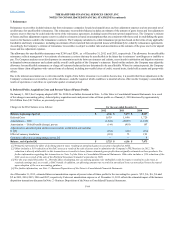

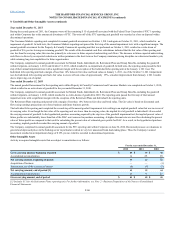

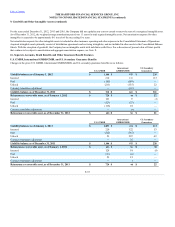

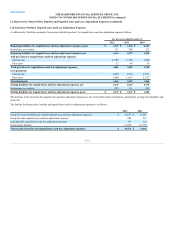

The Company enters into credit default swaps that assume credit risk of a single entity, referenced index, or asset pool in order to synthetically replicate

investment transactions. The Company will receive periodic payments based on an agreed upon rate and notional amount and will only make a payment if

there is a credit event. A credit event payment will typically be equal to the notional value of the swap contract less the value of the referenced security issuer’s

debt obligation after the occurrence of the credit event. A credit event is generally defined as a default on contractually obligated interest or principal payments

or bankruptcy of the referenced entity. The credit default swaps in which the Company assumes credit risk primarily reference investment grade single

corporate issuers and baskets, which include standard and customized diversified portfolios of corporate issuers. The diversified portfolios of corporate

issuers are established within sector concentration limits and may be divided into tranches that possess different credit ratings.

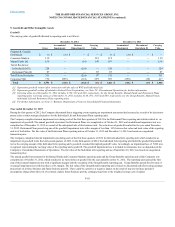

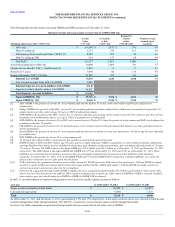

The following tables present the notional amount, fair value, weighted average years to maturity, underlying referenced credit obligation type and average credit

ratings, and offsetting notional amounts and fair value for credit derivatives in which the Company is assuming credit risk as of December 31, 2012 and

2011.

Single name credit default swaps

Investment grade risk exposure $ 2,321 $ 7 3 years Corporate Credit/

Foreign Gov.

A$1,367 $ (26)

Below investment grade risk exposure 145 (1)1 year Corporate Credit B+ 145 (3)

Basket credit default swaps [4]

Investment grade risk exposure 3,978 73 years Corporate Credit BBB+ 2,712 (13)

Investment grade risk exposure 330 (17)4 years CMBS Credit A330 17

Below investment grade risk exposure 195 (46)4 years CMBS Credit B+ 195 46

Embedded credit derivatives

Investment grade risk exposure 525 478 4 years Corporate Credit BBB- — —

F-61