Volvo 1998 Annual Report Download - page 8

Download and view the complete annual report

Please find page 8 of the 1998 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

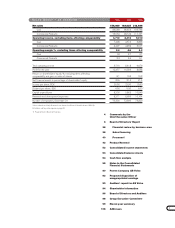

|

|

6

AB Volvo sells Volvo Cars to

Ford and concentrates its business

to commercial products

In January 1999 AB Volvo signed Heads of Agreement with Ford Motor

Company to sell Volvo Cars to Ford. The sale, which is conditional

upon the approval of Volvo’s shareholders and pertinent authorities,

will strengthen Volvo Cars’ future prospects and allow Volvo to make

major investments in trucks, buses, construction equipment, marine

and industrial engines as well as aerospace components.

Against the background of the consolidation under way in the transport vehicle

industry, Volvo conducted a strategic review of the company’s operations. As a

result of this review, Volvo decided to sell Volvo Cars to Ford as the best alterna-

tive for Volvo Cars as well as the Volvo shareholders.

The proposed sale of Volvo Cars is being carried out at a fair price and gives

Volvo a very strong financial position. Through acquisitions and investments,

Volvo will be able to establish positions of world leadership in the field of

commercial products.

Background and reasons for the sale

As in other industries with similar pressure, the automotive companies have

responded to the pressures by seeking to reach greater economies of scale within

development, manufacturing, marketing and distribution. One way to achieve

greater scale is through mergers and acquisitions, leading to a smaller number of

independent companies, each of which manages a number of different brands

within the same group. Going forward, many observers expect that the smaller

manufacturers will not remain independent, and that six to eight global, very

large-scale automotive manufacturers will constitute the industry.

With an annual production of just less than 400,000 cars, Volvo remains

a relatively small niche player. Volvo Cars’ volume growth is decisive for its

future earnings performance.

To successfully develop and market new car generations requires a very signifi-

cant level of investment in platforms, engines, distribution and in environmentally

friendly solutions for the future, such as alternative drivelines, fuel cells and

hybrids. Volvo Cars has made significant investments in the current generation

of models, which support the company’s near-term financial outlook.

Longer term, however, due to its relatively small volumes, Volvo Cars is faced

with a material risk of not being able to develop and supply a full range of

competitive products and at the same time generate satisfactory profitability.

The necessary investments and R&D expenditures within a 10-year period will

amount to significantly higher levels than today. Volvo Cars already spends less

on R&D in absolute terms than its competitors, but more as a percentage of

BOAR D OF DIRECTORS’ REPORT