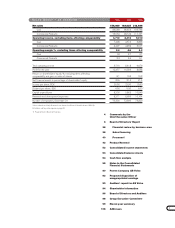

Volvo 1998 Annual Report Download - page 7

Download and view the complete annual report

Please find page 7 of the 1998 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

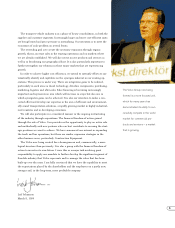

The transport vehicle industry is in a phase of heavy consolidation, in both the

supplier and customer segments. Increasingly larger and more cost-efficient units

are being formed and price pressure is intensifying. Our intention is to meet the

economies of scale problem on several fronts.

The overriding goal is to create the necessary expansion through organic

growth, that is, increase sales in the existing operations and on markets where

we are already established. We will also invest in new products and services as

well as in broadening our geographical base. It is also particularly important to

further strengthen our relations in those major markets that are experiencing

growth.

In order to achieve higher cost efficiency, we intend to intensify efforts to sys-

tematically identify and capitalize on the synergies inherent in our existing op-

erations. This process is under way. There are integration gains to be realized,

particularly in such areas as diesel technology, driveline components, purchasing,

marketing, logistics and after-sales. Sales financing is becoming increasingly

important and represents an area which will increase in scope but also one in

which synergistics gains can be acheived. It is also our intention to make a con-

certed effort and develop our expertise in the area of efficient and environment-

ally sound transportation solutions, a rapidly growing market in highly industrial-

ized countries and in developing economies.

We will also participate in a considered manner in the ongoing restructuring

of the industry through acquisitions. The financial freedom of action gained

through the sale of Volvo Cars provides us the opportunity to play an active role

and methodically seek new partners who can best contribute to securing the strat-

egic positions we want to achieve. We have announced our interest in expanding

the truck and bus operations, but there are similar expansion strategies in the

other business areas, particularly Construction Equipment.

The Volvo now being created has a homogeneous and, commercially, a more

logical structure than previously. It is also a group with the financial freedom of

action to invest in its own future. I view this as a major task involving great

responsibility to apply our mandate to further develop the significant segment of

Swedish industry that Volvo represents and to manage the value that has been

built-up over the years. I am fully convinced that we have the capability to meet

the expectations placed by the shareholders and the employees on a partly new,

stronger and, in the long-term, more profitable company.

Leif Johansson

March 8, 1999

5

The Volvo Group now being

formed is a more focused unit,

which for many years has

demonstrated its ability to suc-

cessfully compete in the world

market for commercial pro-

ducts and services – a market

that is growing.