Time Magazine 2010 Annual Report Download - page 95

Download and view the complete annual report

Please find page 95 of the 2010 Time Magazine annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

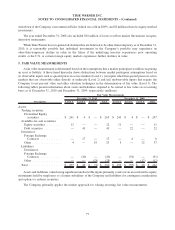

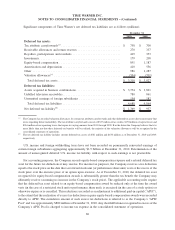

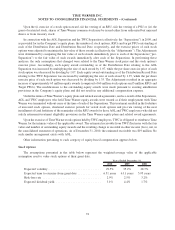

Maturities of Public Debt

The Company’s public debt matures as follows (millions):

2011 2012 2013 2014 2015 Thereafter

Debt................................. $ — 638 732 — 1,000 14,031

Covenants and Rating Triggers

Each of the Company’s New Credit Agreement and public debt indentures contain customary covenants. A

breach of such covenants in the New Credit Agreement that continues beyond any grace period constitutes a default,

which can limit the Company’s ability to borrow and can give rise to a right of the lenders to terminate the facilities

and/or require immediate payment of any outstanding debt. A breach of such covenants in the public debt indentures

beyond any grace period constitutes a default which can require immediate payment of the outstanding debt. There

are no rating-based defaults or covenants in the New Credit Agreement or public debt indentures.

The interest rate on borrowings under the Revolving Credit Facilities and the facility fee are based in part on the

Company’s credit ratings. Therefore, in the event that the Company’s credit ratings decrease, the cost of maintaining

the Revolving Credit Facilities and the cost of borrowing increase and, conversely, if the ratings improve, such costs

decrease. As of December 31, 2010, the Company’s investment grade debt ratings were as follows: Fitch BBB,

Moody’s Baa2, and S&P BBB.

As of December 31, 2010, the Company was in compliance with all covenants in the Prior Credit Agreement

and its public debt indentures. The Company does not anticipate that it will have any difficulty in the foreseeable

future complying with the covenants in its New Credit Agreement or public debt indentures.

Other Obligations

Other long-term debt obligations consist of non-recourse debt, capital lease and other obligations, including

committed financings by subsidiaries under local bank credit agreements. At December 31, 2010 and 2009, the

weighted average interest rate for other long-term debt obligations was 4.57% and 2.41%, respectively.

During the first quarter of 2010, the Company used a portion of the net proceeds from the 2010 Debt Offerings

to repay the $805 million outstanding under the Company’s two accounts receivable securitization facilities. The

Company terminated the two accounts receivable securitization facilities on March 19, 2010 and March 24, 2010,

respectively.

Capital Leases

The Company has entered into various leases primarily related to network equipment that qualify as capital

lease obligations. As a result, the present value of the remaining future minimum lease payments is recorded as a

capitalized lease asset and related capital lease obligation in the consolidated balance sheet. Assets recorded under

capital lease obligations totaled $149 million and $165 million as of December 31, 2010 and 2009, respectively.

Related accumulated amortization totaled $81 million and $70 million as of December 31, 2010 and 2009,

respectively.

83

TIME WARNER INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS – (Continued)