The Hartford 2013 Annual Report Download - page 150

Download and view the complete annual report

Please find page 150 of the 2013 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

|

|

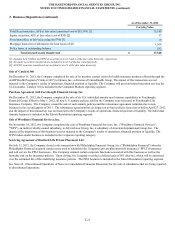

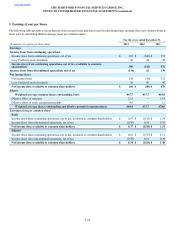

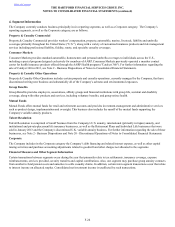

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (continued)

1. Basis of Presentation and Significant Accounting Policies (continued)

F-14

Cash Flow Hedges

Changes in the fair value of a derivative that is designated and qualifies as a cash flow hedge, including foreign-currency cash flow

hedges, are recorded in AOCI and are reclassified into earnings when the variability of the cash flow of the hedged item impacts

earnings. Gains and losses on derivative contracts that are reclassified from AOCI to current period earnings are included in the line item

in the consolidated statements of operations in which the cash flows of the hedged item are recorded. Any hedge ineffectiveness is

recorded immediately in current period earnings as net realized capital gains and losses. Periodic derivative net coupon settlements are

recorded in the line item of the consolidated statements of operations in which the cash flows of the hedged item are recorded.

Net Investment in a Foreign Operation Hedges

Changes in fair value of a derivative used as a hedge of a net investment in a foreign operation, to the extent effective as a hedge, are

recorded in the foreign currency translation adjustments account within AOCI. Cumulative changes in fair value recorded in AOCI are

reclassified into earnings upon the sale or complete, or substantially complete, liquidation of the foreign entity. Any hedge

ineffectiveness is recorded immediately in current period earnings as net realized capital gains and losses. Periodic derivative net coupon

settlements are recorded in the line item of the consolidated statements of operations in which the cash flows of the hedged item are

recorded.

Other Investment and/or Risk Management Activities

The Company’s other investment and/or risk management activities primarily relate to strategies used to reduce economic risk or

replicate permitted investments and do not receive hedge accounting treatment. Changes in the fair value, including periodic derivative

net coupon settlements, of derivative instruments held for other investment and/or risk management purposes are reported in current

period earnings as net realized capital gains and losses.

Hedge Documentation and Effectiveness Testing

To qualify for hedge accounting treatment, a derivative must be highly effective in mitigating the designated changes in fair value or

cash flow of the hedged item. At hedge inception, the Company formally documents all relationships between hedging instruments and

hedged items, as well as its risk-management objective and strategy for undertaking each hedge transaction. The documentation process

includes linking derivatives that are designated as fair value, cash flow, or net investment hedges to specific assets or liabilities on the

balance sheet or to specific forecasted transactions and defining the effectiveness and ineffectiveness testing methods to be used. The

Company also formally assesses both at the hedge’s inception and ongoing on a quarterly basis, whether the derivatives that are used in

hedging transactions have been and are expected to continue to be highly effective in offsetting changes in fair values or cash flows of

hedged items. Hedge effectiveness is assessed primarily using quantitative methods as well as using qualitative methods. Quantitative

methods include regression or other statistical analysis of changes in fair value or cash flows associated with the hedge relationship.

Qualitative methods may include comparison of critical terms of the derivative to the hedged item. Hedge ineffectiveness of the hedge

relationships are measured each reporting period using the “Change in Variable Cash Flows Method”, the “Change in Fair Value

Method”, the “Hypothetical Derivative Method”, or the “Dollar Offset Method”.

Discontinuance of Hedge Accounting

The Company discontinues hedge accounting prospectively when (1) it is determined that the derivative is no longer highly effective in

offsetting changes in the fair value or cash flows of a hedged item; (2) the derivative is de-designated as a hedging instrument; or (3) the

derivative expires or is sold, terminated or exercised.

When hedge accounting is discontinued because it is determined that the derivative no longer qualifies as an effective fair-value hedge,

the derivative continues to be carried at fair value on the balance sheet with changes in its fair value recognized in current period

earnings. Changes in the fair value of the hedged item attributable to the hedged risk is no longer adjusted through current period

earnings and the existing basis adjustment is amortized to earnings over the remaining life of the hedge item through the applicable

earnings component associated with the hedged item.

When hedge accounting is discontinued because the Company becomes aware that it is not probable that the forecasted transaction will

occur, the derivative continues to be carried on the balance sheet at its fair value, and gains and losses that were accumulated in AOCI

are recognized immediately in earnings.

In other situations in which hedge accounting is discontinued on a cash-flow hedge, including those where the derivative is sold,

terminated or exercised, amounts previously deferred in AOCI are reclassified into earnings when earnings are impacted by the

variability of the cash flow of the hedged item.