The Hartford 2013 Annual Report Download - page 124

Download and view the complete annual report

Please find page 124 of the 2013 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

|

|

124

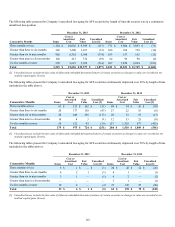

HLIKK has four revolving credit facilities in support of operations. Two of the credit facilities have no amounts drawn as of

December 31, 2013 with borrowing limits of approximately ¥5 billion, or $48 each, and individually have expiration dates of January 5,

2015 and September 30, 2014. In December 2013, HLIKK entered into two new revolving credit facility agreements with two Japanese

banks in order to finance certain withholding taxes on mutual fund gains, that are subsequently credited when HLIKK files its’ income

tax returns. At December 31, 2013, HLIKK had drawn the total borrowing limits of ¥5 billion, or $48, and ¥20 billion, or $190 on these

credit facilities. The ¥5 billion credit facility accrues interest at a variable rate based on the one month Tokyo Interbank Offering Rate

(TIBOR) plus 3 bps, which as of December 31, 2013 the interest rate was 15 bps, and the ¥20 billion credit facility accrues interest at a

variable rate based on TIBOR plus 3 bps, or the actual cost of funding, which as of December 31, 2013 the interest rate was 20 bps.

Both of the credit facilities expire on September 30, 2014.

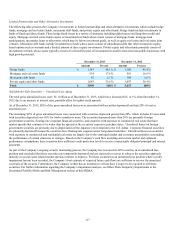

Derivative Commitments

Certain of the Company’s derivative agreements contain provisions that are tied to the financial strength ratings of the individual legal

entity that entered into the derivative agreement as set by nationally recognized statistical rating agencies. If the legal entity’s financial

strength were to fall below certain ratings, the counterparties to the derivative agreements could demand immediate and ongoing full

collateralization and in certain instances demand immediate settlement of all outstanding derivative positions traded under each

impacted bilateral agreement. The settlement amount is determined by netting the derivative positions transacted under each agreement.

If the termination rights were to be exercised by the counterparties, it could impact the legal entity’s ability to conduct hedging activities

by increasing the associated costs and decreasing the willingness of counterparties to transact with the legal entity. The aggregate fair

value of all derivative instruments with credit-risk-related contingent features that are in a net liability position as of December 31, 2013

was $1.2 billion. Of this $1.2 billion the legal entities have posted collateral of $1.4 billion in the normal course of business. In addition,

the Company has posted collateral of $44 associated with a customized GMWB derivative. Based on derivative market values as of

December 31, 2013, a downgrade of one level below the current financial strength ratings by either Moody’s or S&P could require

approximately an additional $12 to be posted as collateral. Based on derivative market values as of December 31, 2013, a downgrade by

either Moody’s or S&P of two levels below the legal entities’ current financial strength ratings could require approximately an additional

$33 of assets to be posted as collateral. These collateral amounts could change as derivative market values change, as a result of changes

in our hedging activities or to the extent changes in contractual terms are negotiated. The nature of the collateral that we would post, if

required, would be primarily in the form of U.S. Treasury bills, U.S. Treasury notes and government agency securities.

As of December 31, 2013, the aggregate notional amount and fair value of derivative relationships that could be subject to immediate

termination in the event of rating agency downgrades to either BBB+ or Baa1 was $536 and $(17), respectively.

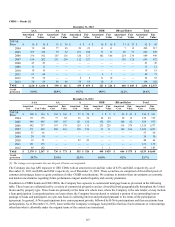

Insurance Operations

Current and expected patterns of claim frequency and severity or surrenders may change from period to period but continue to be within

historical norms and, therefore, the Company’s insurance operations’ current liquidity position is considered to be sufficient to meet

anticipated demands over the next twelve months, including any obligations related to the Company’s restructuring activities. For a

discussion and tabular presentation of the Company’s current contractual obligations by period, refer to Off-Balance Sheet Arrangements

and Aggregate Contractual Obligations within the Capital Resources and Liquidity section of the MD&A.

The principal sources of operating funds are premiums, fees earned from assets under management and investment income, while

investing cash flows originate from maturities and sales of invested assets. The primary uses of funds are to pay claims, claim

adjustment expenses, commissions and other underwriting expenses, to purchase new investments and to make dividend payments to the

HFSG Holding Company.

The Company’s insurance operations consist of property and casualty insurance products (collectively referred to as “Property &

Casualty Operations”) and life insurance and legacy annuity products (collectively referred to as “Life Operations”).

Property & Casualty Operations

Property & Casualty Operations holds fixed maturity securities including a significant short-term investment position (securities with

maturities of one year or less at the time of purchase) to meet liquidity needs.

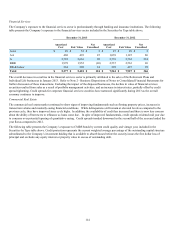

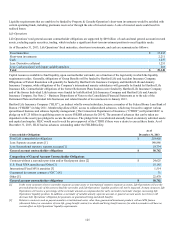

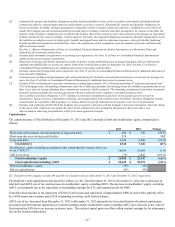

As of December 31, 2013, Property & Casualty Operations’ fixed maturities, short-term investments, and cash are summarized as

follows:

Fixed maturities $ 24,704

Short-term investments 984

Cash 189

Less: Derivative collateral 241

Total $ 25,636