Starwood 2008 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2008 Starwood annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

|

|

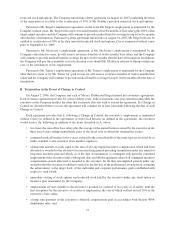

• immediate vesting of all unvested 401(k) contributions in the executive’s 401(k) account or payment by the

Company of an amount equal to any such unvested amounts that are forfeited by reason of the executive’s

termination of employment.

In addition, to the extent that any executive becomes subject to the “golden parachute” excise tax imposed

under Section 4999 of the Code, the executive would receive a gross-up payment in an amount sufficient to offset

the effects of such excise tax.

Under the severance agreements, a “Change in Control” is deemed to occur upon any of the following events:

• any person becomes the beneficial owner of securities of the Company (not including in the securities

beneficially owned by such person any securities acquired directly from the Company or its affiliates)

representing 25% or more of the combined voting power of the Company;

• a majority of the Directors cease to serve on the Company’s Board in connection with a successful hostile

proxy contest;

• a merger or consolidation of the Company or any direct or indirect subsidiary of the Company with any

other corporation, other than:

Oa merger or consolidation in which securities of the Company would represent at least 70% of the voting

power of the surviving entity; or

Oa merger or consolidation effected to implement a recapitalization of the Company in which no person

becomes the beneficial owner of 25% or more of the voting power of the Company; or

• approval of a plan of liquidation or dissolution by the stockholders or the consummation of a sale of all or

substantially all of the Company’s assets, other than a sale to an entity in which the Company’s stockholders

would hold at least 70% of the voting power in substantially the same proportions as their ownership of the

Company immediately prior to such sale. However, a “Change in Control” does not include a transaction in

which Company stockholders continue to hold substantially the same proportionate ownership in the entity

which would own all or substantially all of the Company’s assets following such transaction.

Each of Messrs. Avril, McAveety and Turner entered into similar change in control agreements in connection

with their employment with the Company, provided that no tax gross-up is provided if such payments become

subject to the excise tax. If such payments are subject to the excise tax, the benefits under the agreement will be

reduced until the point where the executive is better off paying the excise tax rather than reducing the benefits.

Mr. van Paasschen’s employment agreement provides that he would be entitled to the following benefits if his

employment were terminated without cause or he resigned with good reason following a Change in Control:

• two times the sum of his base salary plus the average of the annual bonuses earned in the three fiscal years

ending immediately prior to the fiscal year in which the termination occurs;

• a lump sum amount, in cash, equal to the sum of (A) any unpaid incentive compensation which had been

allocated or awarded for any measuring period preceding termination under any annual or long-term

incentive plan and which, as of the date of termination, is contingent only upon his continued employment

until a subsequent date, and (B) the aggregate value of all contingent incentive compensation awards

allocated or awarded to him for all then uncompleted periods under any such plan that he would have

earned on the last day of the performance award period, assuming the achievement, at the target level, of the

individual and corporate performance goals established with respect to such award;

• immediate vesting of stock options and restricted stock held under any stock option or incentive plan

maintained by the Company;

• a lump sum payment of his deferred compensation paid in accordance with Section 409A distribution

rules; and

38