Starwood 2008 Annual Report Download - page 103

Download and view the complete annual report

Please find page 103 of the 2008 Starwood annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

|

|

Amortization expense was $26 million in the year ended December 31, 2007, consistent with the corre-

sponding period of 2006.

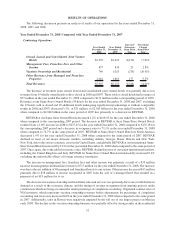

Operating Income. Operating income increased 2.3% or $19 million to $858 million for the year ended

December 31, 2007 when compared to $839 million in the same period in 2006, primarily due to the increase in

management fees, franchise fees and other income, partially offset by the restructuring and other special charges

and the decline in revenues from owned, leased and consolidated joint venture hotels discussed above.

Equity Earnings and Gains and Losses from Unconsolidated Ventures, Net. Equity earnings and gains and

losses from unconsolidated joint ventures increased to $66 million for the year ended December 31, 2007 from

$61 million in the same period of 2006 partially due to our share of gains on the sale of several hotels in an

unconsolidated joint venture during 2007.

Net Interest Expense. Net interest expense decreased to $147 million for the year ended December 31, 2007

as compared to $215 million in the same period of 2006, primarily due to $37 million of expenses recorded in the

first quarter of 2006 related to the early extinguishment of debt in connection with two transactions whereby we

defeased and were released from certain debt obligations that allowed us to sell certain hotels that previously served

as collateral for such debt. The decrease was also due to an increase in capitalized interest related to vacation

ownership projects under construction and a decrease in our overall interest rate. Our weighted average interest rate

was 6.52% at December 31, 2007 versus 6.97% at December 31, 2006.

Loss on Asset Dispositions and Impairments, Net. During 2007, we recorded a net loss of $44 million,

primarily related to a net loss of $58 million on the sale of eight wholly owned hotels and a loss of approximately

$7 million primarily related to charges at three other properties. These losses were offset in part by $20 million of

net gains primarily on the sale of assets in which we held a minority interest and a gain of $6 million as a result of

insurance proceeds received for property damage caused by storms at two owned hotels in prior years.

During 2006, we recorded a net loss of $3 million primarily related to several offsetting gains and losses,

including the sale of ten wholly-owned hotels, which were sold unencumbered by management agreements,

impairment charges related to various properties, including the Sheraton Cancun which was damaged by Hurricane

Wilma in 2005, and an adjustment to reduce the previously recorded gain on the sale of a hotel consummated in

2004 as certain contingencies associated with the sale became probable in 2006. These losses were primarily offset

by a gain of $29 million on the sale of our interests in two joint ventures and a $13 million gain as a result of

insurance proceeds received as reimbursement for property damage caused by Hurricane Wilma.

Income Tax Expense. We recorded income tax expense from continuing operations of $189 million for the

year ended December 31, 2007 compared to a benefit of $434 million in the corresponding period of 2006. The 2007

expense was favorably impacted by a $114 million benefit related to the reversal of capital loss valuation allowance,

a $28 million benefit associated with our election to claim foreign tax credits generated in 1999 and 2000 and a

$35 million benefit associated with the utilization of capital losses. Offsetting these benefits were a $97 million

charge associated with the Host Transaction and a $13 million charge associated with interest accrued for uncertain

tax positions. The 2006 tax benefit includes a one-time benefit of approximately $524 million realized in

connection with the Host Transaction, a $59 million benefit due primarily to the completion of various state

and federal income tax audits of prior years, a $34 million benefit associated with our election to claim foreign tax

credits in 2006 and 2005 and a $32 million benefit associated with the Trust prior to its acquisition by Host.

Discontinued Operations

For the year ended December 31, 2007, the loss on disposition represented a $1 million tax assessment

associated with the disposition of our gaming business in 1999. For the year ended December 31, 2006, the loss on

disposition represented a $2 million tax assessment associated with the disposition of our gaming business in 1999.

Cumulative Effect of Accounting Change, Net of Tax

On January 1, 2007, we adopted FIN 48 and recorded a benefit of $35 million to the beginning balance of

retained earnings.

37