Shaw 2009 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2009 Shaw annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

|

|

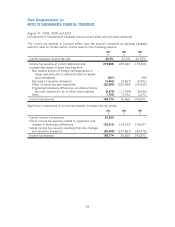

Fair value estimates are made at a specific point in time, based on relevant market information and

information about the financial instrument. These estimates are subjective in nature and involve

uncertainties and matters of significant judgement and, therefore, cannot be determined with

precision. Changes in assumptions could significantly affect the estimates.

Risk management

The Company is exposed to various market risks including currency risk and interest rate risk, as

well as credit risk and liquidity risk associated with financial assets and liabilities. The Company

has designed and implemented various risk management strategies, discussed further below, to

ensure the exposure to these risks is consistent with its risk tolerance and business objectives.

Currency risk

As the Company has grown it has accessed US capital markets for a portion of its borrowings. Since

the Company’s revenues and assets are primarily denominated in Canadian dollars, it faces

significant potential foreign exchange risks in respect of the servicing of the interest and principal

components of its US dollar denominated debt. The Company utilizes cross-currency swaps, where

appropriate, to hedge its exposures on US dollar denominated debenture indebtedness. As at

August 31, 2009, 100% of the Company’s US dollar denominated debt maturities were hedged.

In addition, some of the Company’s capital expenditures are incurred in US dollars, while its

revenue is primarily denominated in Canadian dollars. Decreases in the value of the Canadian dollar

relative to the US dollar could have an adverse effect on the Company’s cash flows. To mitigate some

of the uncertainty in respect to capital expenditures, the Company regularly enters into forward

contracts in respect of US dollar commitments. With respect to 2009, the Company entered into

forward contracts to purchase US $46,000 over a period of 12 months commencing in September

2008 at an average exchange rate of 1.1507 Cdn. In addition, the Company had in place long term

forward contracts to purchase US $12,296 during 2009 at an average rate 1.4078. At August 31,

2009, the Company has forward contracts to purchase US $84,000 over a period of 12 months

commencing in September 2009 at an average exchange rate of 1.1089 Cdn. In addition, the

Company has in place long term forward contracts to purchase US $6,972 during 2010 at an

average rate 1.4078.

Interest rate risk

Due to the capital-intensive nature of its operations, the Company utilizes long-term financing

extensively in its capital structure. The primary components of this structure are banking facilities

and various Canadian and US denominated senior notes and debentures with varying maturities

issued in the public markets as more fully described in note 9.

Interest on the Company’s banking facilities is based on floating rates, while the senior notes and

debentures are fixed-rate obligations. The Company utilizes its credit facility to finance day-to-day

operations and, depending on market conditions, periodically converts the bank loans to fixed-rate

instruments through public market debt issues. As at August 31, 2009, 100% of the Company’s

consolidated long-term debt was fixed with respect to interest rates.

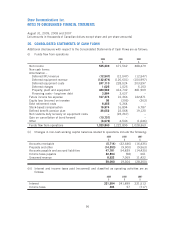

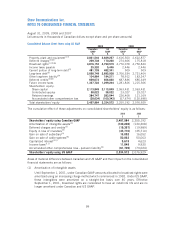

93

Shaw Communications Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

August 31, 2009, 2008 and 2007

[all amounts in thousands of Canadian dollars except share and per share amounts]