Pottery Barn 2010 Annual Report Download - page 126

Download and view the complete annual report

Please find page 126 of the 2010 Pottery Barn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

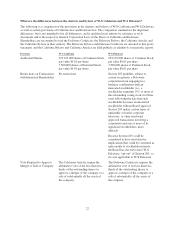

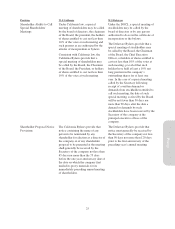

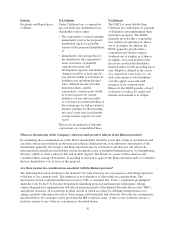

Provision W-S California W-S Delaware

Dividends and Repurchases

of Shares

Under California law, a corporation

may not make any distribution to its

shareholders unless either:

• The corporation’s retained earnings

immediately prior to the proposed

distribution equal or exceed the

amount of the proposed distribution;

or

• Immediately after giving effect to

the distribution, the corporation’s

assets (exclusive of goodwill,

capitalized research and

development expenses and deferred

charges) would be at least equal to

one and one fourth (1-1/4) times its

liabilities (not including deferred

taxes, deferred income and other

deferred credits), and the

corporation’s current assets would

be at least equal to its current

liabilities (or one and one fourth

(1-1/4) times its current liabilities if

the average pre-tax and pre-interest

expense earnings for the preceding

two fiscal years were less than the

average interest expense for such

years).

These tests are applied to California

corporations on a consolidated basis.

The DGCL is more flexible than

California law with respect to payment

of dividends and implementing share

repurchase programs. The DGCL

generally provides that a corporation

may redeem or repurchase its shares

out of its surplus. In addition, the

DGCL generally provides that a

corporation may declare and pay

dividends out of surplus, or if there is

no surplus, out of net profits for the

fiscal year in which the dividend is

declared and/or for the preceding fiscal

year. Surplus is defined as the excess

of a corporation’s net assets (i.e., its

total assets minus its total liabilities)

over the capital associated with

issuances of its common stock.

Moreover, the DGCL permits a board

of directors to reduce its capital and

transfer such amount to its surplus.

What are the interests of the Company’s directors and executive officers in the Reincorporation?

In considering the recommendations of the Board, shareholders should be aware that certain of our directors and

executive officers have interests in the transaction that are different from, or in addition to, the interests of the

shareholders generally. For instance, the Reincorporation may be of benefit to our directors and officers by

reducing their potential personal liability and increasing the scope of permitted indemnification, by strengthening

directors’ ability to resist a takeover bid, and in other respects. The Board was aware of these interests and

considered them, among other matters, in reaching its decision to approve the Reincorporation and to recommend

that our shareholders vote in favor of this proposal.

Are there income tax considerations associated with the Reincorporation?

The following discussion summarizes the material U.S. federal income tax consequences of the Reincorporation

to holders of our common stock. This summary is not exhaustive of all possible tax considerations. The

discussion is based on the Internal Revenue Code of 1986, as amended (the “Code”), regulations promulgated

under the Code by the U.S. Treasury Department (including proposed and temporary regulations), rulings,

current administrative interpretations and official pronouncements of the Internal Revenue Service (the “IRS”),

and judicial decisions, all as currently in effect and all of which are subject to differing interpretations or to

change, possibly with retroactive effect. Such change could materially and adversely affect the tax consequences

described below. No assurance can be given that the IRS would not assert, or that a court would not sustain, a

position contrary to any of the tax consequences described herein.

30