Pep Boys 2005 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2005 Pep Boys annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

|

|

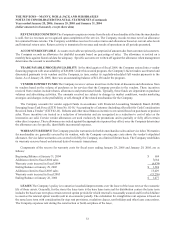

39

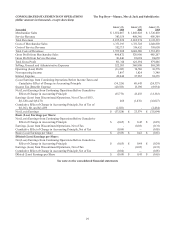

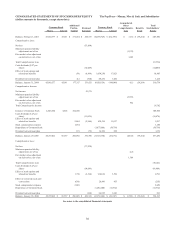

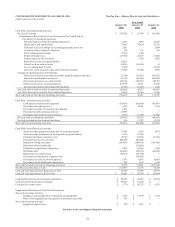

THE PEP BOYS—MANNY, MOE & JACK AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Years ended January 28, 2006, January 29, 2005 and January 31, 2004

(dollar amounts in thousands, except share data)

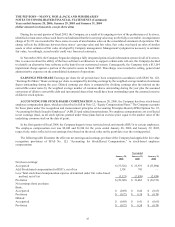

facility is secured by the real property and improvements associated with 154 of the Company’s stores. Interest at the rate of

LIBOR plus 3.0% on this facility is payable by the Company starting in February 2006. Proceeds from this facility were used

to satisfy and discharge the Company’s outstanding $43,000 6.88% Medium Term Notes due March 6, 2006 and $100,000

6.92% Term Enhanced Remarketable Securities (TERMS) due July 7, 2016 and to reduce borrowings under the Company’s

line of credit by approximately $39,000.

In the second quarter of fiscal 2005, the Company reclassified $100,000 aggregate principal amount of the TERMS to

current liabilities on the consolidated balance sheet. The TERMS were retired on January 27, 2006 with cash from the

Company’s $200,000 Senior Secured Term Loan facility. In retiring the TERMS, the Company was obligated to purchase a

call option, which, if exercised, would have allowed the securities to be remarketed through a maturity date of July 7, 2016.

The $8,100 redemption price of the call option was based upon the then present value of the remaining payments on the

TERMS through July 17, 2016, at 5.45%, discounted at the 10 year Treasury rate. Additionally, the Company prepaid $1,296

in interest through the original maturity date of July 17, 2006.

Upon maturity on June 1, 2005, the Company retired the remaining $40,444 aggregate principal amount of its 7.0%

Senior Notes with cash from operations and its existing line of credit. In December 2004, the Company repurchased, through

a tender offer, $59,556 of these notes. In the second quarter of fiscal 2004, the Company reclassified the $100,000 aggregate

principal amount of these notes then outstanding to current liabilities on the balance sheet.

In the first quarter of fiscal 2005 the Company reclassified, to current liabilities on its consolidated balance sheet,

$43,000 aggregate principal amount of 6.88% Medium-Term Notes with a stated maturity date of March 6, 2006. These notes

were retired in January 2006 with cash from the Company’s $200,000 Senior Secured Term Loan facility. Additionally, the

Company prepaid $342 in interest through the original maturity date.

On December 14, 2004, the Company issued $200,000 aggregate principal amount of 7.5% Senior Subordinated Notes

due December 15, 2014.

On December 2, 2004, the Company further amended its amended and restated line of credit agreement. The amendment

increased the amount available for borrowings to $357,500, with an ability, upon satisfaction of certain conditions, to increase

such amount to $400,000. The amendment also reduced the interest rate under the agreement to the London Interbank Offered

Rate (LIBOR) plus 1.75% (after June 1, 2005, the rate decreased to LIBOR plus 1.50%, subject to 0.25% incremental increases

as excess availability falls below $50,000). The amendment also provided the flexibility, upon satisfaction of certain conditions,

to release up to $99,000 of reserves currently required as of December 2, 2004 under the line of credit agreement to support

certain operating leases. This reserve was reduced to $76,401 on December 2, 2004. Finally, the amendment extended the

term of the agreement through December 2009. The weighted average interest rate on borrowings under the line of credit

agreement was 6.2% and 4.1% at January 28, 2006 and January 29, 2005, respectively.

In the third quarter of fiscal 2004, the Company entered into a vendor financing program with an availability of $20,000.

Under this program, the Company’s factor makes accelerated and discounted payments to its vendors and the Company, in

turn, makes its regularly scheduled full vendor payments to the factor. As of January 28, 2006 the Company had an outstanding

balance of $11,156 under these arrangements, classified as trade payable program liability in the consolidated balance sheet.

In the first quarter of fiscal 2004, the Company entered into arrangements with certain of its vendors and banks to extend

payment terms on certain merchandise purchases. Under this program, the bank makes payments to the vendor based upon

a negotiated discount rate between the parties and the Company makes its payment of the full payable to the bank at the

extended payment term. As of July 31, 2004, all obligations under these arrangements were fully satisfied and the agreement

was terminated.

The other notes payable have a principal balance of $1,315 and $1,331 and a weighted average interest rate of 5.1% and

4.8% at January 28, 2006 and January 29, 2005, respectively, and mature at various times through August 2016. Certain of

these notes are collateralized by land and buildings with an aggregate carrying value of approximately $6,744 and $6,766 at

January 28, 2006 and January 29, 2005, respectively.