Pep Boys 2005 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2005 Pep Boys annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

|

|

34

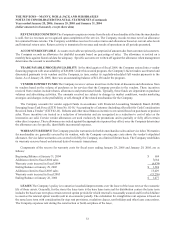

THE PEP BOYS—MANNY, MOE & JACK AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Years ended January 28, 2006, January 29, 2005 and January 31, 2004

(dollar amounts in thousands, except share data)

SERVICE REVENUE Service revenue consists of the labor charge for installing merchandise or maintaining or

repairing vehicles, excluding the sale of any installed parts or materials.

COSTS OF REVENUES Costs of merchandise sales include the cost of products sold, buying, warehousing and store

occupancy costs. Costs of service revenue include service center payroll and related employee benefits and service center

occupancy costs. Occupancy costs include utilities, rents, real estate and property taxes, repairs and maintenance and

depreciation and amortization expenses.

PENSION EXPENSE The Company reports all information on its pension and savings plan benefits in accordance with

FASB Statement of Financial Accounting Standards (SFAS) No. 132, “Employers’ Disclosure about Pensions and Other

Postretirement Benefits (revised 2003)” (SFAS 132R).

INCOME TAXES The Company uses the liability method of accounting for income taxes in accordance with SFAS No.

109, “Accounting for Income Taxes.” Under the liability method, deferred income taxes are determined based upon enacted

tax laws and rates applied to the differences between the financial statement and tax bases of assets and liabilities.

ADVERTISING The Company expenses the production costs of advertising the first time the advertising takes place.

Gross advertising expense for 2005, 2004, and 2003 was $85,809, $73,996 and $61,714, respectively. No advertising costs

were recorded as assets as of January 28, 2006 or January 29, 2005.

The Company receives funds from vendors in the normal course of business for a variety of reasons, including cooperative

advertising. Contracts for cooperative advertising typically have durations of one year. There were 168 and 244 vendors

participating in such contracts at January 28, 2006 and January 29, 2005, respectively. The Company’s level of advertising

expense would not be impacted in the absence of these contracts.

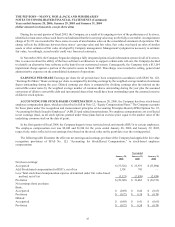

Certain cooperative advertising reimbursements are netted against specific, incremental, identifiable costs incurred in

connection with the selling of the vendor’s product. Cooperative advertising reimbursements of $35,702, and $36,579 and

$42,000 for fiscal years 2005, 2004 and 2003, respectively, were recorded as a reduction of advertising expense with the net

amount included in selling, general and administrative expenses in the consolidated statement of operations. Any excess

reimbursements over these costs are characterized as a reduction of inventory and are recognized as a reduction of cost of

sales as the inventories are sold, in accordance with EITF 02-16. The amount of excess reimbursements recognized as a

reduction of costs of sales were $53,753 and $48,950 and $18,634 for fiscal years 2005, 2004 and 2003, respectively. The

balance of excess reimbursements remaining in inventory was immaterial at January 28, 2006 and January 29, 2005.

The Company restructured substantially all of its vendor agreements in the fourth quarter of 2005. The new vendor

agreements provide flexibility in how the Company can use vendor support funds, and eliminate the administrative burden

associated with tracking the application of such funds. Therefore, going forward all vendor support funds will be treated as

a reduction of inventories and be recognized as a reduction to cost of sales as inventories are subsequently sold.

STORE OPENING COSTS The costs of opening new stores are expensed as incurred.

IMPAIRMENT OF LONG-LIVED ASSETS The Company accounts for impaired long-lived assets in accordance

with SFAS No. 144, “Accounting for the Impairment or Disposal of Long-Lived Assets.” This standard prescribes the method

for asset impairment evaluation for long-lived assets and certain identifiable intangibles that are both held and used or to be

disposed of. The Company evaluates the ability to recover long-lived assets whenever events or circumstances indicate that

the carrying value of the asset may not be recoverable. In the event assets are impaired, losses are recognized to the extent the

carrying value exceeds the fair value. In addition, the Company reports assets to be disposed of at the lower of the carrying

amount or the fair market value less selling costs.

In the fourth quarter of fiscal 2005, the Company recorded in selling, general and administrative expenses an impairment

charge of $4,200 reflecting the remaining value of a commercial sales software asset.