Oracle 2015 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2015 Oracle annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

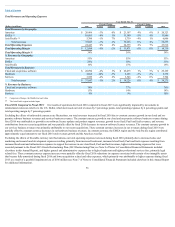

Table of Contents

Our advanced customer support services are offered as standalone arrangements or as a part of arrangements to customers buying other software and non-software

products and services. We offer these advanced support services, both on-premise and remote, to Oracle customers to enable increased performance and higher

availability of their products and services. Depending upon the nature of the arrangement, revenues from these services are recognized as the services are

performed or ratably over the term of the service period, which is generally one year or less.

Education revenues are also a part of our services business and include instructor-led, media-based and internet-based training in the use of our software and

hardware products. Education revenues are recognized as the classes or other education offerings are delivered.

If an arrangement contains multiple elements and does not qualify for separate accounting for the product and service transactions, then new software licenses

revenues and/or hardware products revenues, including the costs of hardware products, are generally recognized together with the services based on contract

accounting using either the percentage-of-completion or completed-contract method. For the purposes of revenue classification of the elements that are accounted

for as a single unit of accounting, we allocate revenues to software and non-software elements based on a rational and consistent methodology utilizing our best

estimate of the relative selling price of such elements.

We also evaluate arrangements with governmental entities containing “fiscal funding” or “termination for convenience” provisions, when such provisions are

required by law, to determine the probability of possible cancellation. We consider multiple factors, including the history with the customer in similar transactions,

the “essential use” of the software or hardware products and the planning, budgeting and approval processes undertaken by the governmental entity. If we

determine upon execution of these arrangements that the likelihood of cancellation is remote, we then recognize revenues once all of the criteria described above

have been met. If such a determination cannot be made, revenues are recognized upon the earlier of cash receipt or approval of the applicable funding provision by

the governmental entity.

We assess whether fees are fixed or determinable at the time of sale and recognize revenues if all other revenue recognition requirements are met. Our standard

payment terms are net 30 days. However, payment terms may vary based on the country in which the agreement is executed. We evaluate non-standard payment

terms based on whether we have successful collection history on comparable arrangements (based upon similarity of customers, products, and license economics)

and, if so, generally conclude such payment terms are fixed and determinable and thereby satisfy the required criteria for revenue recognition.

While most of our arrangements for sales within our businesses include short-term payment terms, we have a standard practice of providing long-term financing to

creditworthy customers primarily through our financing division. Since fiscal 1989, when our financing division was formed, we have established a history of

collection, without concessions, on these receivables with payment terms that generally extend up to five years from the contract date. Provided all other revenue

recognition criteria have been met, we recognize new software licenses revenues and hardware products revenues for these arrangements upon delivery, net of any

payment discounts from financing transactions. We have generally sold receivables financed through our financing division on a non-recourse basis to third-party

financing institutions within 90 days of the contracts’ dates of execution and we classify the proceeds from these sales as cash flows from operating activities in our

consolidated statements of cash flows. We account for the sales of these receivables as “true sales” as defined in ASC 860, TransfersandServicing, as we are

considered to have surrendered control of these financing receivables.

Our customers include several of our suppliers and, occasionally, we have purchased goods or services for our operations from these vendors at or about the same

time that we have sold our products to these same companies (Concurrent Transactions). Software license agreements, sales of hardware or sales of services that

occur within a three-month time period from the date we have purchased goods or services from that same customer are reviewed for appropriate accounting

treatment and disclosure. When we acquire goods or services from a customer, we negotiate the purchase separately from any sales transaction, at terms we

consider to be at arm’s length and settle the purchase in cash. We recognize revenues from Concurrent Transactions if all of our revenue recognition criteria are met

and the goods and services acquired are necessary for our current operations.

50