Oracle 2015 Annual Report Download - page 106

Download and view the complete annual report

Please find page 106 of the 2015 Oracle annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

Table of Contents

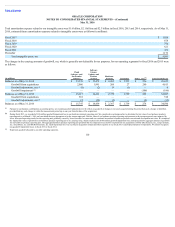

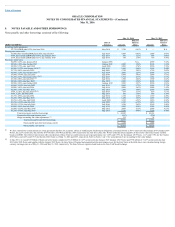

ORACLE CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

May 31, 2016

In January 2016, the FASB issued ASU 2016-01, FinancialInstruments—Overall(Subtopic825-10):RecognitionandMeasurementofFinancialAssetsand

FinancialLiabilities(ASU 2016-01), which addresses certain aspects of recognition, measurement, presentation, and disclosure of financial instruments. ASU

2016-01 is effective for us in our first quarter of fiscal 2019, and earlier adoption is not permitted except for certain provisions. We currently do not expect that our

pending adoption of ASU 2016-01 will have a material effect on our consolidated financial statements.

Stock-based Compensation: In March 2016, the FASB issued ASU 2016-09, Compensation—StockCompensation(Topic718):ImprovementstoEmployee

Share-BasedPaymentAccounting(ASU 2016-09). ASU 2016-09 changes how companies account for certain aspects of stock-based awards to employees,

including the accounting for income taxes, forfeitures, and statutory tax withholding requirements, as well as classification in the statement of cash flows. ASU

2016-09 is effective for us in our first quarter of fiscal 2018, and earlier adoption is permitted. We believe we will early adopt ASU 2016-09 in the first quarter of

fiscal 2017 and are currently evaluating the impact of our pending adoption on our consolidated financial statements. We currently believe the most significant

impact of our adoption of ASU 2016-09 to our consolidated financial statements will be to recognize certain tax benefits or tax shortfalls upon a restricted-stock

award vesting or stock option exercise event relative to the deferred tax asset position established in our provision for income taxes line of our consolidated

statement of operations instead of to consolidated equity. During fiscal 2016, 2015 and 2014, we recorded $141 million, $267 million and $254 million to

consolidated equity as tax benefits from our stock plans.

Leases: In February 2016, the FASB issued ASU 2016-02, Leases(Topic842)(ASU 2016-02). ASU 2016-02 requires companies to generally recognize on the

balance sheet operating and financing lease liabilities and corresponding right-of-use assets. ASU 2016-02 is effective for us in our first quarter of fiscal 2020 on a

modified retrospective basis, and earlier adoption is permitted. We are currently evaluating the impact of our pending adoption of ASU 2016-02 on our

consolidated financial statements, and we currently expect that most of our operating lease commitments will be subject to the new standard and recognized as

operating lease liabilities and right-of-use assets upon our adoption of ASU 2016-02, which will increase our total assets and total liabilities that we report relative

to such amounts prior to adoption.

Revenue Recognition: In May 2014, the FASB issued ASU 2014-09, RevenuefromContractswithCustomers:Topic606and issued subsequent amendments to

the initial guidance in August 2015, March 2016, April 2016 and May 2016 within ASU 2015-04, ASU 2016-08, ASU 2016-10 and ASU 2016-12, respectively

(ASU 2014-09, ASU 2015-04, ASU 2016-08, ASU 2016-10 and ASU 2016-12 collectively, Topic 606). Topic 606 supersedes nearly all existing revenue

recognition guidance under GAAP. The core principle of Topic 606 is to recognize revenues when promised goods or services are transferred to customers in an

amount that reflects the consideration that is expected to be received for those goods or services. Topic 606 defines a five-step process to achieve this core principle

and, in doing so, it is possible more judgment and estimates may be required within the revenue recognition process than are required under existing GAAP,

including identifying performance obligations in the contract, estimating the amount of variable consideration to include in the transaction price and allocating the

transaction price to each separate performance obligation, among others. Topic 606 is effective for us as of either our first quarter of fiscal 2018 or our first quarter

of fiscal 2019 using either of two methods: (1) retrospective application of Topic 606 to each prior reporting period presented with the option to elect certain

practical expedients as defined within Topic 606 or (2) retrospective application of Topic 606 with the cumulative effect of initially applying Topic 606 recognized

at the date of initial application and providing certain additional disclosures as defined per Topic 606. Preliminarily, we plan to adopt Topic 606 in the first quarter

of fiscal 2019 pursuant to the aforementioned adoption method (1) and we do not believe there will be a material impact to our revenues upon adoption. We are

continuing to evaluate the impacts of our pending adoption of Topic 606 and our preliminary assessments are subject to change.

104