Oracle 2015 Annual Report Download - page 110

Download and view the complete annual report

Please find page 110 of the 2015 Oracle annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

Table of Contents

ORACLE CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

May 31, 2016

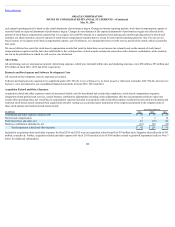

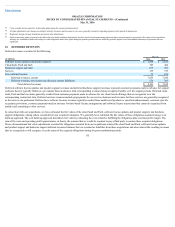

4. FAIR VALUE MEASUREMENTS

We perform fair value measurements in accordance with ASC 820. ASC 820 defines fair value as the price that would be received from selling an asset or paid to

transfer a liability in an orderly transaction between market participants at the measurement date. When determining the fair value measurements for assets and

liabilities required to be recorded at their fair values, we consider the principal or most advantageous market in which we would transact and consider assumptions

that market participants would use when pricing the assets or liabilities, such as inherent risk, transfer restrictions and risk of nonperformance.

ASC 820 establishes a fair value hierarchy that requires an entity to maximize the use of observable inputs and minimize the use of unobservable inputs when

measuring fair value. An asset’s or a liability’s categorization within the fair value hierarchy is based upon the lowest level of input that is significant to the fair

value measurement. ASC 820 establishes three levels of inputs that may be used to measure fair value:

• Level 1: quoted prices in active markets for identical assets or liabilities;

• Level 2: inputs other than Level 1 that are observable, either directly or indirectly, such as quoted prices in active markets for similar assets or liabilities,

quoted prices for identical or similar assets or liabilities in markets that are not active, or other inputs that are observable or can be corroborated by

observable market data for substantially the full term of the assets or liabilities; or

• Level 3: unobservable inputs that are supported by little or no market activity and that are significant to the fair values of the assets or liabilities.

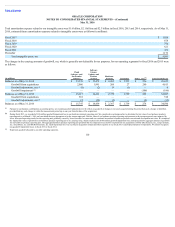

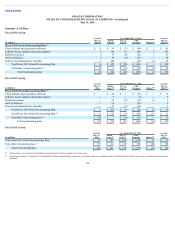

Assets and Liabilities Measured at Fair Value on a Recurring Basis

Our assets and liabilities measured at fair value on a recurring basis, excluding accrued interest components, consisted of the following (Level 1 and Level 2 inputs

are defined above):

May 31, 2016 May 31, 2015

Fair Value Measurements

Using Input Types

Fair Value Measurements

Using Input Types

(in millions) Level 1 Level 2 Total Level 1 Level 2 Total

Assets:

Money market funds $ 3,750 $ — $ 3,750 $ — $ — $ —

U.S. Treasury securities 214 — 214 668 — 668

Commercial paper debt securities — 2,155 2,155 — 9,203 9,203

Corporate debt securities and other 179 35,095 35,274 190 28,654 28,844

Derivative financial instruments — 122 122 — 74 74

Total assets $ 4,143 $ 37,372 $ 41,515 $ 858 $ 37,931 $ 38,789

Liabilities:

Derivative financial instruments $ — $ 218 $ 218 $ — $ 244 $ 244

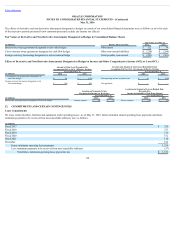

Our valuation techniques used to measure the fair values of our marketable securities that were classified as Level 1 in the table above were derived from quoted

market prices and active markets for these instruments exist. Our valuation techniques used to measure the fair values of Level 2 instruments listed in the table

above, the counterparties to which have high credit ratings, were derived from the following: non-binding market consensus prices that were corroborated by

observable market data, quoted market prices for similar instruments, or pricing models, such as discounted cash flow techniques, with all significant inputs derived

from or corroborated by observable market data including LIBOR-based yield curves, among others.

Based on the trading prices of our $40.1 billion and $42.0 billion of borrowings, which consisted of senior notes and the related fair value hedges that were

outstanding as of May 31, 2016 and 2015, respectively, the estimated

108