MetLife 2000 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2000 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

|

|

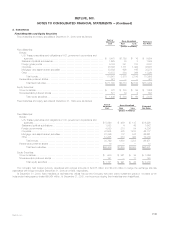

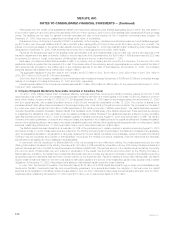

METLIFE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

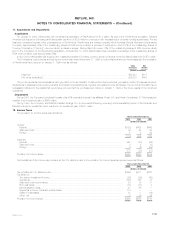

The assumptions used in determining the aggregate projected benefit obligation and aggregate contract value for the pension and other benefits

were as follows:

Pension Benefits Other Benefits

2000 1999 2000 1999

(Dollars in millions)

Weighted average assumptions at December 31:

Discount rate ************************************************************* 6.9% – 7.75% 6.25% – 7.75% 6% – 7.5% 6% – 7.75%

Expected rate of return on plan assets**************************************** 8% – 9% 8% – 10.5% 6% – 9% 6% – 9%

Rate of compensation increase ********************************************** 4% – 6% 4.5% – 8.5% N/A N/A

The assumed health care cost trend rates used in measuring the accumulated nonpension postretirement benefit obligation were 6.5% per year for

pre-Medicare eligible claims and 6% for Medicare eligible claims in 2000 and 1999.

Assumed health care cost trend rates may have a significant effect on the amounts reported for health care plans. A one-percentage point change in

assumed health care cost trend rates would have the following effects:

One Percent One Percent

Increase Decrease

(Dollars in millions)

Effect on total of service and interest cost components *********************************************** $16 $13

Effect of accumulated postretirement benefit obligation************************************************ $143 $118

The components of periodic benefit costs were as follows:

Pension Benefits Other Benefits

2000 1999 1998 2000 1999 1998

(Dollars in millions)

Service cost ******************************************************************* $ 98 $ 100 $ 90 $ 29 $ 28 $ 31

Interest cost ******************************************************************* 291 271 257 113 107 114

Expected return on plan assets *************************************************** (420) (363) (337) (97) (89) (79)

Amortization of prior actuarial gains ************************************************ (19) (6) (11) (22) (11) (13)

Curtailment (credit) cost ********************************************************* (3) (17) (10) 2 10 4

Net periodic benefit (credit) cost ************************************************** $ (53) $ (15) $ (11) $ 25 $ 45 $ 57

Savings and Investment Plans

The Company sponsors savings and investment plans for substantially all employees under which the Company matches a portion of employee

contributions. The Company contributed $65 million, $45 million and $43 million for the years ended December 31, 2000, 1999 and 1998, respectively.

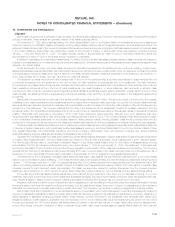

6. Closed Block

On the date of demutualization, Metropolitan Life established a closed block for the benefit of holders of certain individual life insurance policies of

Metropolitan Life. Assets have been allocated to the closed block in an amount that has been determined to produce cash flows which, together with

anticipated revenues from the policies included in the closed block, are reasonably expected to be sufficient to support obligations and liabilities relating

to these policies, including, but not limited to, provisions for the payment of claims and certain expenses and taxes, and to provide for the continuation of

policyholder dividend scales in effect for 1999, if the experience underlying such dividend scales continues, and for appropriate adjustments in such

scales if the experience changes. The closed block assets, the cash flows generated by the closed block assets and the anticipated revenues from the

policies in the closed block will benefit only the holders of the policies in the closed block. To the extent that, over time, cash flows from the assets

allocated to the closed block and claims and other experience related to the closed block are, in the aggregate, more or less favorable than what was

assumed when the closed block was established, total dividends paid to closed block policyholders in the future may be greater than or less than the

total dividends that would have been paid to these policyholders if the policyholder dividend scales in effect for 1999 had been continued. Any cash flows

in excess of amounts assumed will be available for distribution over time to closed block policyholders and will not be available to stockholders. If the

closed block has insufficient funds to make guaranteed policy benefit payments, such payments will be made from assets outside of the closed block.

The closed block will continue in effect as long as any policy in the closed block remains in-force. The expected life of the closed block is over 100 years.

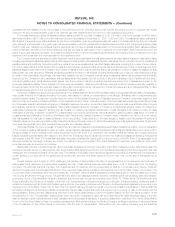

The Company uses the same accounting principles to account for the participating policies included in the closed block as it used prior to the date

of demutualization. However, the Company establishes a policyholder dividend obligation for earnings that will be paid to policyholders as additional

dividends as described below. The excess of closed block liabilities over closed block assets at the effective date of the demutualization (adjusted to

eliminate the impact of related amounts in accumulated other comprehensive income) represents the estimated maximum future earnings from the

closed block expected to result from operations attributed to the closed block after income taxes. Earnings of the closed block are recognized in income

over the period the policies and contracts in the closed block remain in-force. Management believes that over time the actual cumulative earnings of the

closed block will approximately equal the expected cumulative earnings due to the effect of dividend changes. If, over the period the closed block

remains in existence, the actual cumulative earnings of the closed block is greater than the expected cumulative earnings of the closed block, the

Company will pay the excess of the actual cumulative earnings of the closed block over the expected cumulative earnings to closed block policyholders

as additional policyholder dividends unless offset by future unfavorable experience of the closed block and, accordingly, will recognize only the expected

cumulative earnings in income with the excess recorded as a policyholder dividend obligation. If over such period, the actual cumulative earnings of the

closed block is less than the expected cumulative earnings of the closed block, the Company will recognize only the actual earnings in income. However,

the Company may change policyholder dividend scales in the future, which would be intended to increase future actual earnings until the actual

MetLife, Inc. F-21