MetLife 2000 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2000 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

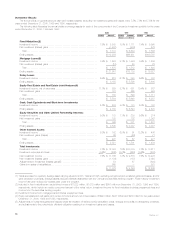

Commercial mortgage loans. The Company diversifies its commercial mortgage loans by both geographic region and property type, and

manages these investments through a network of regional offices overseen by its investment department. The following table presents the distribution

across geographic regions and property types for commercial mortgage loans at December 31, 2000 and 1999:

At December 31,

2000 1999

Carrying % of Carrying % of

Value Total Value Total

(Dollars in millions)

Region

South Atlantic ******************************************************************* $ 4,542 26.9% $ 4,098 27.6%

Pacific************************************************************************** 3,111 18.4 2,596 17.5

Middle Atlantic ******************************************************************* 2,968 17.6 2,703 18.2

East North Central**************************************************************** 1,822 10.8 1,865 12.5

West South Central*************************************************************** 1,169 6.9 1,012 6.8

New England ******************************************************************** 1,157 6.9 1,095 7.4

Mountain *********************************************************************** 753 4.5 490 3.3

West North Central *************************************************************** 740 4.4 652 4.4

International ********************************************************************* 433 2.6 202 1.3

East South Central *************************************************************** 174 1.0 149 1.0

Total ******************************************************************* $16,869 100.0% $14,862 100.0%

Property Type

Office ************************************************************************** $ 7,577 44.9% $ 6,789 45.7%

Retail*************************************************************************** 4,148 24.6 3,620 24.4

Apartments********************************************************************** 2,585 15.3 2,382 16.0

Industrial ************************************************************************ 1,414 8.4 1,136 7.6

Hotel*************************************************************************** 865 5.1 843 5.7

Other ************************************************************************** 280 1.7 92 0.6

Total ******************************************************************* $16,869 100.0% $14,862 100.0%

The following table presents the scheduled maturities for the Company’s commercial mortgage loans at December 31, 2000 and 1999:

At December 31,

2000 1999

Carrying % of Carrying % of

Value Total Value Total

(Dollars in millions)

Due in one year or less *********************************************************** $ 644 3.8% $ 806 5.4%

Due after one year through two years *********************************************** 934 5.5 482 3.2

Due after two years through three years ********************************************* 830 4.9 708 4.8

Due after three years through four years ********************************************* 1,551 9.2 787 5.3

Due after four years through five years *********************************************** 1,654 9.8 1,608 10.8

Due after five years *************************************************************** 11,256 66.8 10,471 70.5

Total ******************************************************************* $16,869 100.0% $14,862 100.0%

Problem, potential problem and restructured mortgage loans. The Company monitors its mortgage loan investments on a continual

basis. Through this monitoring process, the Company reviews loans that are restructured, delinquent or under foreclosure and identifies those that

management considers to be potentially delinquent. These loan classifications are generally consistent with those used in industry practice.

The Company defines restructured mortgage loans, consistent with industry practice, as loans in which the Company, for economic or legal reasons

related to the debtor’s financial difficulties, grants a concession to the debtor that it would not otherwise consider. This definition provides for loans to exit

the restructured category under certain conditions. The Company defines delinquent mortgage loans, consistent with industry practice, as loans in which

two or more interest or principal payments are past due. The Company defines mortgage loans under foreclosure, consistent with industry practice, as

loans in which foreclosure proceedings have formally commenced. The Company defines potentially delinquent loans as loans that, in management’s

opinion, have a high probability of becoming delinquent.

The Company reviews all mortgage loans on an annual basis. These reviews may include an analysis of the property financial statements and rent

roll, lease rollover analysis, property inspections, market analysis and tenant creditworthiness. The Company also reviews loan-to-value ratios and debt

coverage ratios for restructured loans, delinquent loans, loans under foreclosure, potentially delinquent loans, loans with an existing valuation allowance,

loans maturing within two years and loans with a loan-to-value ratio greater than 90% as determined in the prior year.

The Company establishes valuation allowances for loans that it deems impaired, as determined through its annual review process. The Company

defines impaired loans consistent with Statement of Financial Accounting Standards No. 114, Accounting by Creditors for Impairment of a Loan, as loans

which it probably will not collect all amounts due according to applicable contractual terms of the agreement. The Company bases valuation allowances

upon the present value of expected future cash flows discounted at the loan’s original effective interest rate or the value of the loan’s collateral. The

Company records valuation allowances as investment losses and includes them in earnings. The Company records subsequent adjustments to

allowances as investment gains or losses and includes them in earnings.

MetLife, Inc.

22