MasterCard 2010 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2010 MasterCard annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

|

|

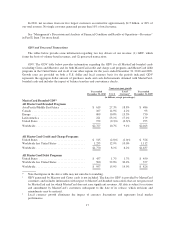

MasterCard members or its payment obligations to MasterCard merchants, we may require the member to post

collateral, typically in the form of standby letters of credit, bank guarantees or secured cash accounts. As of

December 31, 2010, we had members who had posted approximately $3.0 billion in collateral held for settlement

exposure for MasterCard-branded transactions. If a member becomes unable or unwilling to meet its obligations

to us or other members, we are able to draw upon such member’s collateral, if provided, in order to minimize any

potential loss to our members or ourselves. In addition to obtaining collateral from members, in situations where

a member is potentially unable to meet its obligations to us or other members, we can block authorization and

settlement of transactions and ultimately terminate membership. Additionally, and to further preserve payment

system integrity, MasterCard reserves the right to terminate a member’s right to participate in MasterCard’s

payment card network if, for example, the member fails or refuses to make payments in the ordinary course of

business, or if a liquidating agent, conservator or receiver is appointed for the member. In addition to these

measures, we have also established a $2.75 billion committed credit facility to provide liquidity for general

corporate purposes, including to provide liquidity in the event of member settlement failure. See “Risk Factors—

Business Risks—As a guarantor of certain obligations of principal members and affiliate debit licensees, we are

exposed to risk of loss or illiquidity if any of our customers default on their MasterCard, Cirrus or Maestro

settlement obligations” in Part I, Item 1A. See also “Risk Factors—Business Risks—Unprecedented global

economic events in financial markets around the world have directly and adversely affected, and may continue to

affect, many of our customers, merchants that accept our brands and cardholders who use our brands, which

could result in a material and adverse impact on our prospects, growth, profitability, revenue and overall

business” in Part I, Item 1A.

Payment System Integrity

The integrity of our payment system can be affected by fraudulent activity and illegal uses of cards and our

system. Fraud is most often committed in connection with lost, stolen or counterfeit cards or stolen account

information, often resulting from security breaches of third party systems that inappropriately store cardholder

account data. See “Risk Factors—Business Risks—Account data breaches involving card data stored by us or

third parties could adversely affect our reputation and revenue” in Part I, Item 1A. Fraud is also more likely to

occur in transactions where the card is not present, such as e-Commerce, mail order and telephone order

transactions. Security and cardholder authentication for these remote channels are particularly critical issues

facing our customers and merchants who engage in these forms of commerce, where a signed cardholder sales

receipt or the presence of the card or merchant agent is unavailable.

We monitor areas of risk exposure and enforce our standards to combat fraudulent activity. We also operate

several compliance programs to help ensure that the integrity of our payment system is maintained by our

customers and their agents. Key compliance programs include merchant audits (for high fraud, excessive

chargebacks and processing of illegal transactions) and security compliance (including our MasterCard Site Data

Protection Service®, which assists customers and merchants in protecting commercial sites from hacker

intrusions and subsequent account data compromises) by requiring proper adherence to the Payment Card

Industry Data Security Standards (PCI DDS). Our customers are also required to report instances of fraud to us in

a timely manner so we can monitor trends and initiate action where appropriate.

Our customers generally are responsible for fraud losses associated with the cards they issue and the

merchants from which they acquire transactions. However, we have implemented a series of programs and

systems to aid them in detecting and preventing the fraudulent use of MasterCard cards. We provide education

programs and various risk management tools to help prevent fraud, including MasterCard SecureCode®, a global

Internet authentication solution that permits cardholders to authenticate themselves to their issuer using a unique,

personal code, and our Site Data Protection program. We also provide fraud detection and prevention solutions,

including EMS and DataCash fraud prevention tools.

19