MasterCard 2010 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2010 MasterCard annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

|

|

situation is reversed and interchange fees are paid by issuers to acquirers. We establish default interchange fees

that apply when there are no other established settlement terms in place between an issuer and an acquirer. We

administer the collection and remittance of interchange fees through the settlement process. Interchange fees can

be a significant component of the merchant discount, and therefore of the costs that merchants pay to accept

payment cards. These fees are currently subject to regulatory, legislative and/or legal challenges in a number of

jurisdictions. We are devoting substantial management and financial resources to the defense of interchange fees

and to the other legal and regulatory challenges we face. See “Risk Factors—Legal and Regulatory Risks” in Part

I, Item 1A.

Merchant Discount. The merchant discount is established by the acquirer to cover its costs and profit

margin of participating in the four-party system. The discount takes into consideration the amount of the

interchange fee which the acquirer generally pays to the issuer, and the balance of the discount either consists of

fees established by the acquirer and paid by the merchant for certain of the acquirer’s services to the merchant

(which are retained by the acquirer) or reflects the costs of such services.

Additional Fees and Economic Considerations. Acquirers may charge merchants processing and related

fees in addition to the merchant discount. Issuers may also charge cardholders fees for the transaction, including,

for example, fees for extending revolving credit. As described below, we charge issuers and acquirers

transaction-based and related fees for the transaction processing and related services we provide them.

In a four-party payment system, the economics of a payment transaction relative to MasterCard vary widely

depending on such factors as whether the transaction is domestic (and, if it is domestic, the country in which it

takes place) or cross-border, whether it is a point-of-sale purchase transaction or cash withdrawal, and whether

the transaction is processed over our network or a third-party network or is handled solely by a financial

institution that is both the acquirer for the merchant and the issuer to the cardholder (an “on-us” transaction).

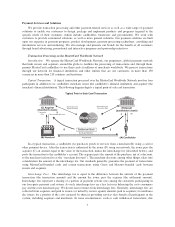

MasterCard Worldwide Network Architecture and Operations. We believe the architecture of the

MasterCard Worldwide Network is unique, featuring a globally integrated structure that provides scalability for

our customers and enables them to expand into regional and global markets. Our network also features an

intelligent architecture that enables it to adapt to the needs of each transaction by blending two distinct

processing structures—distributed (peer-to-peer) and centralized (hub-and-spoke). Transactions that require fast,

reliable processing, such as those submitted using a MasterCard PayPass®-enabled device in a tollway, use the

network’s distributed processing structure, ensuring they are processed close to where the transaction occurred.

Transactions that require value-added processing, such as real-time access to transaction data for fraud scoring or

rewards at the point-of-sale, or customization of transaction data for unique consumer-spending controls, use the

network’s centralized processing structure, ensuring advanced processing services are applied to the transaction.

The network typically operates at under 80% capacity and can handle more than 160 million transactions

per hour with an average network response time of 130 milliseconds. The network can also substantially scale

capacity to meet demand. Our transaction processing services are available 24 hours per day, every day of the

year. Our global payment network provides multiple levels of back-up protection and related continuity

procedures in the event of an outage should the issuer, acquirer or payment network experience a service

interruption. To date, we have consistently maintained availability of our global processing systems more than

99.9% of the time.

Processing Capabilities.

•Transaction Switching—Authorization, Clearing and Settlement. MasterCard provides transaction

switching (authorization, clearing and settlement) through the MasterCard Worldwide Network.

OAuthorization. Authorization refers to the process by which a transaction is approved by the issuer

or, in certain circumstances such as when the issuer’s systems are unavailable or cannot be

contacted, by MasterCard or others on behalf of the issuer in accordance with either the issuer’s

instructions or applicable rules. For offline transactions (as well as online transactions in Europe),

the Dual Message System (which sends authorization and clearing messages separately) provides for

8