LensCrafters 2012 Annual Report Download - page 206

Download and view the complete annual report

Please find page 206 of the 2012 LensCrafters annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

|

|

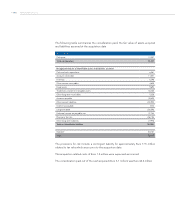

ANNUAL REPORT 2012> 120 |

beginning on or after January 1, 2013. The Group believes that the amendment will not

have a material impact on its consolidated financial statements.

On May 17, 2012 the IASB issued the Improvements to IFRS, which are summarized below.

The Group believes that these amendments will not have a significant impact on its

consolidated financial statements The amendments are applicable to reporting periods

beginning on or after January 1, 2013. Early adoption is permitted, however, the Group has

not elected to early adopt any of the following:

• Amendment to IFRS 1 - “First time adoption of IFRS”. The amendment clarifies that

an entity may apply IFRS 1 more than once under certain circumstances. An entity that

previously applied IFRS but then stopped is permitted but not required to apply IFRS

1 when it recommences applying IFRS;

• Amendment to IFRS 1 - “First time adoption of IFRS”. The amendment clarifies that an

entity can choose to adopt IAS 23, “Borrowing costs”, either from its date of transition

or from an earlier date;

• Amendment to IAS 1 - “Presentation of Financial Statements”. The amendment clarifies

the disclosure requirements for comparative information when an entity provides

a third balance sheet either as required by IAS 8, “Accounting policies, changes in

accounting estimates and errors” or voluntarily;

• Amendment to IFRS 1 as a result of the above amendment to IAS 1. The consequential

amendment clarifies that a first-time adopter should provide the supporting notes for

all statements presented;

• Amendment to IAS 16 - “Property, Plant and Equipment”. The amendment clarifies that

spare parts and servicing equipment are classified as property, plant and equipment

rather than inventory when they are used for longer than one period;

• Amendment to IAS 32 - “Financial Instruments Presentation”. The amendment clarifies

the treatment of income taxes relating to distributions and transaction costs. Income

taxes related to distributions are to be recognized in the income statement, and

income taxes related to the costs of equity transactions are to be recognized in equity;

• Amendment to IAS 34 - “Interim Financial Reporting”. The amendment clarifies that a

measure of total assets and liabilities is required for an operating segment in interim

financial statements if such information is regularly provided to the “Chief Operating

Decision Maker” and there has been a material change in those measures since the

most recent annual financial statements.

The assets of the Group are exposed to different types of financial risk: market risk (which

includes exchange rate risks, interest rate risk relative to fair value variability and cash flow

uncertainty), credit risk and liquidity risk. The risk management strategy of the Group aims

to stabilize the results of the Group by minimizing the potential effects due to volatility in

financial markets. The Group uses derivative financial instruments, principally interest rate

and currency swap agreements, as part of its risk management strategy.

Financial risk management is centralized within the Treasury department which identifies,

evaluates and implements financial risk hedging activities, in compliance with the Financial

Risk Management Policy guidelines approved by the Board of Directors, and in accordance

with the Group operational units. The Policy defines the guidelines for any kind of risk, such

3. FINANCIAL RISKS