Kroger 2013 Annual Report Download - page 147

Download and view the complete annual report

Please find page 147 of the 2013 Kroger annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152

|

|

A-74

NO T E S T O C O N S O L I D A T E D F I N A N C I A L S T A T E M E N T S , CO N T I N U E D

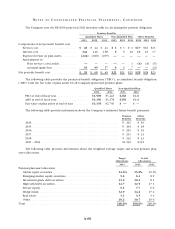

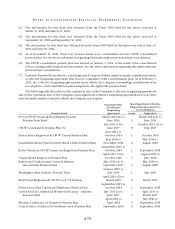

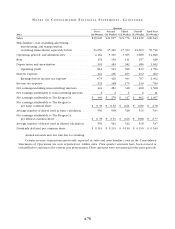

(1) This column represents the number of significant collective bargaining agreements and their expiration

date for each of the Company’s pension funds listed above. For purposes of this table, the “significant

collective bargaining agreements” are the largest based on covered employees that, when aggregated,

cover the majority of the employees for which we make multi-employer contributions for the referenced

pension fund.

(2) Certain collective bargaining agreements for each of these pension funds are operating under

an extension.

(3) As of January 1, 2012, four multi-employer pension funds were consolidated into the UFCW consolidated

pension plan. See the above information regarding this multi-employer pension fund consolidation.

Based on the most recent information available to it, the Company believes that the present value of

actuarial accrued liabilities in most of these multi-employer plans substantially exceeds the value of the assets

held in trust to pay benefits. Moreover, if the Company were to exit certain markets or otherwise cease making

contributions to these funds, the Company could trigger a substantial withdrawal liability. Any adjustment for

withdrawal liability will be recorded when it is probable that a liability exists and can be reasonably estimated.

The Company also contributes to various other multi-employer benefit plans that provide health and

welfare benefits to active and retired participants. Total contributions made by the Company to these other

multi-employer benefit plans were approximately $1,100 in 2013, $1,100 in 2012 and $1,000 in 2011.

17. R E C E N T L Y A D O P T E D A C C O U N T I N G S T A N D A R D S

In February 2013, the Financial Accounting Standards Board (“FASB”) amended its standards on

comprehensive income by requiring disclosure of information about amounts reclassified out of accumulated

other comprehensive income (“AOCI”) by component. Specifically, the amendment requires disclosure of the

effect of significant reclassifications out of AOCI on the respective line items in net income in which the item

was reclassified if the amount being reclassified is required to be reclassified to net income in its entirety

in the same reporting period. It requires cross reference to other disclosures that provide additional detail

for amounts that are not required to be reclassified in their entirety in the same reporting period. This new

disclosure became effective for the Company beginning February 3, 2013, and is being adopted prospectively

in accordance with the standard. See Note 9 to the Company’s Consolidated Financial Statements for the

Company’s new disclosures related to this amended standard.

In December 2011, the FASB amended its standards related to offsetting assets and liabilities. This

amendment requires entities to disclose both gross and net information about certain instruments and

transactions eligible for offset in the statement of financial position and certain instruments and transactions

subject to an agreement similar to a master netting agreement. This information is intended to enable users of

the financial statements to understand the effect of these arrangements on the Company’s financial position.

The new rules became effective for the Company on February 3, 2013. In January 2013, the FASB further

amended this standard to limit its scope to derivatives, repurchase and reverse repurchase agreements,

securities borrowings and lending transactions. See Note 7 to the Company’s Consolidated Financial Statements

for the Company’s new disclosures related to this amended standard.

1 8 . R E C E N T L Y I S S U E D A C C O U N T I N G S T A N D A R D S

In July 2013, the FASB amended Accounting Standards Codification (“ASC”) 740, “Income Taxes.” The

amendment provides guidance on the financial statement presentation of an unrecognized tax benefit, as

either a reduction of a deferred tax asset or as a liability, when a net operating loss carryforward, similar tax

loss, or a tax credit carryforward exists. The amendment will be effective for interim and annual periods

beginning after December 15, 2013 and may be applied on a retrospective basis. Early adoption is permitted.

The Company does not expect the adoption of this amendment to have a significant effect on the Company’s

consolidated financial position or results of operations.