Kraft 2007 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2007 Kraft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

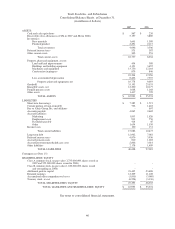

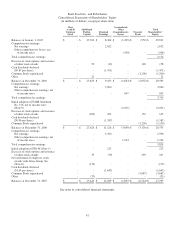

|

|

Inventories:

Inventories are stated at the lower of cost or market. The last-in, first-out (“LIFO”) method is used to cost a majority of

domestic inventories. The cost of other inventories is principally determined by the average cost method. We used the LIFO

method to determine the cost of 37% of inventories at December 31, 2007 and 41% of inventories at December 31, 2006. The

stated LIFO amounts of inventories were $142 million lower at December 31, 2007 and $70 million higher at December 31,

2006 than the current cost of inventories. We also record inventory allowances for overstocked and obsolete inventories due to

ingredient and packaging changes.

We prospectively adopted the provisions of Statement of Financial Accounting Standards (“SFAS”) No. 151, Inventory Costs,

on January 1, 2006. SFAS No. 151 requires us to: (i) recognize abnormal idle facility expense, spoilage, freight and handling

costs as current-period charges; and (ii) allocate fixed production overhead costs to inventories based on the normal capacity of

the production facility. The effect of adoption did not have a material impact on our financial statements.

Long-lived assets:

Property, plant and equipment are stated at historical cost and depreciated by the straight-line method over the estimated useful

lives of the assets. Machinery and equipment are depreciated over periods ranging from 3 to 20 years, and buildings and

building improvements over periods up to 40 years.

We review long-lived assets, including amortizable intangible assets, for impairment when conditions exist that indicate the

carrying amount of the assets may not be fully recoverable. We perform undiscounted operating cash flow analyses to determine

if an impairment exists. When testing assets held for use for impairment, we group assets and liabilities at the lowest level for

which cash flows are separately identifiable. If an impairment is determined to exist, the loss is calculated based on fair value.

Impairment losses on assets to be disposed of, if any, are based on the estimated proceeds to be received, less costs of disposal.

During 2006, we recorded non-cash asset impairment charges of $245 million related to our Tassimo hot beverage system long-

lived assets. The charges are included in asset impairment and exit costs in the consolidated statement of earnings.

Software costs:

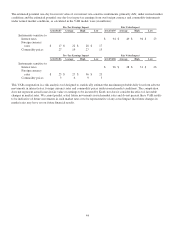

We capitalize certain computer software and software development costs incurred in connection with developing or obtaining

computer software for internal use. Capitalized software costs are included in property, plant and equipment on the consolidated

balance sheets and amortized on a straight-line basis over the estimated useful lives of the software, which do not exceed five

years.

Goodwill and Intangible assets:

SFAS No. 142, Goodwill and Other Intangible Assets, (“SFAS No. 142”) requires us to test goodwill and non-amortizable

intangible assets at least annually for impairment. To test goodwill, we compare the fair value of each reporting unit with the

carrying value of the reporting unit. If the carrying value exceeds the fair value, goodwill is considered impaired. The

impairment loss is measured as the difference between the carrying value and implied fair value of goodwill, which is

determined using discounted cash flows. To test non-amortizable intangible assets for impairment, we compare the fair value of

the intangible asset with its carrying value. If the carrying value exceeds fair value, the intangible asset is considered impaired

and is reduced to fair value. Definite lived intangible assets are amortized over their estimated useful lives.

Since our adoption of SFAS No. 142, we have completed our annual impairment review of goodwill and non-amortizable

intangible assets as of January 1. During the first quarter of 2007, we completed our annual review of goodwill and

non-amortizable intangible assets and found no impairments. Effective October 1, 2007, we adopted a new accounting policy to

perform our annual impairment review of goodwill and non-amortizable intangible assets as of October 1 instead of January 1

of each year. The change in our testing date was made to align it with the revised timing of our annual strategic planning process

implemented in 2007. As a result, we performed our annual impairment tests again as of October 1, 2007 and found no

impairments. During the first quarter of 2006, we completed our annual review of goodwill and intangible assets and recorded a

$24 million non-cash charge for impairment of biscuits assets in Egypt and hot cereal assets in the U.S. The charge is included

in asset impairment and exit costs in the consolidated statement of earnings. During the first quarter of 2005, we completed our

annual review of goodwill and intangible assets. No impairments resulted from this review.

Insurance & Self-Insurance:

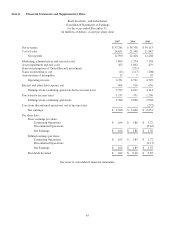

We use a combination of insurance and self-insurance for a number of risks, including workers’ compensation, general liability,

automobile liability, product liability and our obligation for employee healthcare benefits. Liabilities associated with the risks

are estimated by considering historical claims experience and other actuarial assumptions.

50