Honda 2007 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2007 Honda annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

63

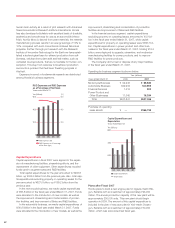

The estimated amount of capital expenditures in fiscal 2008 is

shown below.

Yen (millions)

Year ending March 31 2008

Motorcycle Business ¥092,800

Automobile Business 588,000

Financial Services 1,300

Power Product and Other Businesses 27,900

Total ¥710,000

The estimated amount of capital expenditures in fiscal 2008 for

financial services does not include property on operating leases.

Liquidity and Capital Resources

Overview of Capital Requirements, Sources and Uses

The policy of Honda is to support its business activities by

maintaining sufficient capital resources, a sufficient level of

liquidity and a sound balance sheet.

Honda’s main business is the manufacturing and sale of

motorcycles, automobiles and power products. To support this

business, it also provides retail financing and automobile leas-

ing services for customers, as well as wholesale financing

services for dealers.

In its manufacturing and sales business, Honda requires

operating capital mainly to purchase parts and materials

required for production, as well as to control inventory of fin-

ished products and cover receivables from dealers. Honda also

requires funds for capital expenditures, mainly to introduce new

models, upgrade, rationalize and renew production facilities, as

well as to expand and reinforce Sales and R&D facilities.

Honda meets its operating capital requirements mainly

through cash generated by operations. Honda funds its finan-

cial programs for customers and dealers primarily from corpo-

rate bonds, medium-term notes, commercial paper, and

securitization of finance receivables. The year-end balance of

liabilities associated with fund-raising by finance subsidiaries

was ¥4,470.4 billion as of March 31, 2007.

Cash Flows

Consolidated cash and cash equivalents amounted to ¥945.5

billion as of March 31, 2007, up ¥228.7 billion, or 31.9%, from a

year earlier, mainly owing to the increases in net cash provided by

operating and financing activities, offset in part by the increase in

net cash used in investing activities as described below.

Net cash provided by operating activities amounted to

¥904.5 billion. Factors increasing operating cash flows

included continued significant growth in sales and stable oper-

ating margins (excluding the effect of the non-cash gain on

return in the prior year), accompanied by lower increases in net

operating assets and liabilities in the current year.

Net cash used in investing activities totaled ¥1,130.7 billion.

Factors increasing net cash used in investing cash flows were

mainly due to ¥597.9 billion in capital expenditures associated

with introducing new models, upgrading, streamlining and

renewing production facilities, and the improvement of Sales

and R&D facilities. Other factors were ¥240.2 billion increase in

acquisition of finance subsidiaries-receivables and ¥365.5 bil-

lion increase of property on operating leases associated with

higher sales of automobiles in North America and elsewhere.

Net cash provided by financing activities was ¥423.4 billion.

During the year, Honda raised ¥306.0 billion in short-term debt

through the issue of commercial paper, and also raised ¥969.4

billion in long-term debt through the issue of bonds and

medium-term notes to meet capital requirements associated

mainly with an increase in liabilities of finance subsidiaries, as

well as to repay ¥677.5 billion in long-term debt. By contrast,

Honda also made ¥26.6 billion in payments for purchase of

treasury stock and ¥140.4 billion in cash dividends paid.

Liquidity

The ¥945.5 billion in cash and cash equivalents at end of year

corresponds to approximately 1.0 month of net sales, and

Honda believes it has sufficient liquidity for its business opera-

tions. At the same time, Honda is aware of the possibility that

various factors, such as recession-induced market contraction

and financial and foreign exchange market volatility, may

adversely affect liquidity.

For this reason, finance subsidiaries carry total short-term

borrowings of ¥1,842.1 billion in the form of commercial paper

issued regularly to replace debt. This serves as alternative

liquidity for a back-up credit line equivalent to ¥826.1 billion.

Honda believes it currently has sufficient credit limits, extended

by prominent international banks.

Honda believes it has adequate liquidity to meet its cash

obligations for the near future at least for the year ending

March 31, 2008.

Honda’s short- and long-term debt securities are rated by

credit rating agencies, such as Moody’s Investor Service, Inc.,

and Standard & Poor’s Rating Services. Based on major cur-

rent ratings, which are shown below, Honda will be able to

raise funds even if it requires more capital than its present level

of liquidity would allow.

The following table shows the ratings of Honda’s unsecured

debt securities by Moody’s and Standard & Poor’s as of the

date of the filing of this Form 20-F.

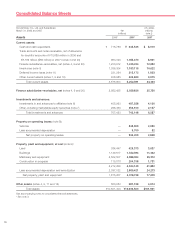

Credit Ratings for

Short-term Long-term

unsecured unsecured

debt securities debt securities

Moody’s Investors Service P-1 Aa3

Standard & Poor’s Rating Services A-1 A+

The above ratings are based on information provided by

Honda and other information deemed credible by the rating

agencies. They are also based on the agencies’ assessment of

credit risk associated with designated securities issued by

Honda. Each rating agency uses different standards for calcu-

lating Honda’s credit rating, and also makes its own assess-

ments. Ratings can be revised or nullified by agencies at any

time. These ratings are not meant to serve as a recommenda-

tion for trading in or holding debt.

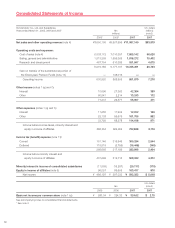

Off-Balance Sheet Arrangements

Special Purpose Entity

For the purpose of accelerating the receipt of cash related to our

finance receivables, we periodically securitize and sell pools of

these receivables. In these securitizations, we sell a portfolio of