HTC 2012 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2012 HTC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

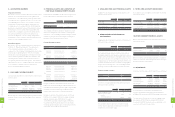

Long-term equity investments

As of January 1, 2011, the capital surplus from long-term equity-method investments was NT$18,411 thousand. When

the Company did not subscribe for the new shares issued by an equity-method investee, Huada Digital Corporation,

in September 2011, the Company's total investment carrying value and capital surplus decreased by NT$374 thousand

each in 2011. As a result, the capital surplus from long-term equity-method investments as of December 31, 2012 was

NT$18,037 thousand (US$619 thousand). 。

Merger

The additional paid-in capital from a merger with IA Style (Note 14) was NT$24,710 thousand as of January 1, 2011. In

December 2011, the retirement of treasury stock caused a decrease of NT$287 thousand in additional paid-in capital from

the foregoing merger. As a result, the additional paid-in capital from a merger as of December 31, 2012 was NT$24,423

thousand (US$838 thousand).。

4. Appropriation of Retained Earnings and Dividend Policy

Under the Company's Articles of Incorporation, if the Company has earnings after the annual final accounting, it shall be

allocated in the following order:

a. To pay taxes

b. To cover accumulated losses, if any

c. To appropriate 10% legal reserve unless the total legal reserve accumulated has already reached the amount of the

Company's authorized capital

d. To pay remuneration to directors and supervisors at 0.3% maximum of the balance after deducting the amounts under

the above items (a) to (c)

e. To pay bonus to employees at 5% minimum of the balance after deducting the amounts under the above items (a) to (c),

or such balance plus the unappropriated retained earnings of previous years. However, the bonus may not exceed the

limits on employee bonus distributions as set out in the Regulations Governing the Offering and Issuance of Securities

by Issuers. Where bonus to employees is allocated by means of new share issuance, the employees to receive bonus

may include the affiliates' employees who meet specific requirements prescribed by the board of directors.

f. For any remainder, the board of directors should propose allocation ratios based on the dividend policy set forth in the

Company's Articles and propose them at the stockholders' meeting.

Legal reserve should be appropriated until it has reached a company's paid-in capital. This reserve may be used to offset

a deficit. Under the revised Company Law issued on January 4, 2012, when the legal reserve has exceeded 25% of a

company’s paid-in capital, the excess may be transferred to capital or distributed in cash.

As part of a high-technology industry and as a growing enterprise, the Company considers its operating environment,

industry developments, and long-term interests of stockholders as well as its programs to maintain operating efficiency

and meet its capital expenditure budget and financial goals in determining the stock or cash dividends to be paid. The

Company’s dividend policy stipulates that at least 50% of total dividends may be distributed as cash dividends.

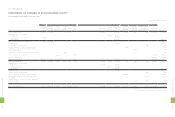

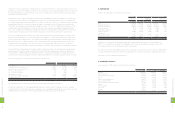

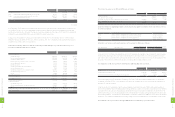

The appropriations of earnings for 2010 and 2011 were approved in the stockholders' meetings on June 15, 2011 and June

12, 2012, respectively. The appropriations and dividends per share were as follows:

For Year 2010 For Year 2011

Appropriation of

Earnings

Dividends

Per Share

Appropriation of

Earnings Dividends Per Share

NT$ NT$ NT$ NT$ NT$ US$ (Note 3)

Legal reserve $- $- $6,197,580 $212,763 $- $-

Special reserve 580,856 - (580,856) (19,941) - -

Cash dividends 29,891,089 37.00 33,249,085 1,141,443 40.00 1.37

Stock dividends 403,934 0.50 - - - -

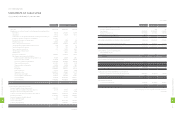

20. STOCKHOLDERS' EQUITY

1. Capital Stock

The Company's outstanding common stock as of January 1, 2011 amounted to NT$8,176,532 thousand, divided into

817,653 thousand common shares at NT$10 par value. In June 2011, the stockholders approved the transfer of retained

earnings of NT$403,934 thousand and employee bonuses of NT$40,055 thousand to capital stock. Also, in December

2011, the Company retired 10,000 thousand treasury shares amounting to NT$100,000 thousand. As a result, the

amount of the Company's outstanding common stock as of December 31, 2012 increased to NT$8,520,521 thousand

(US$292,510 thousand), divided into 852,052 thousand common shares at NT$10 (US$0.34) par value.

2. Global Depositary Receipts

In November 2003, the Company issued 14,400 thousand common shares corresponding to 3,600 thousand units of Global

Depositary Receipts ("GDRs"). For this GDR issuance, the Company's stockholders, including Via Technologies, Inc., also issued

12,878.4 thousand common shares, corresponding to 3,219.6 thousand GDR units. Thus, the entire offering consisted of 6,819.6

thousand GDR units. Taking into account the effect of stock dividends, the GDRs increased to 9,015.1 thousand units (36,060.5

thousand shares). The holders of these GDRs requested the Company to redeem the GDRs to get the Company's common

shares. As of December 31, 2012, there were 7,820 thousand units of GDRs redeemed, representing 31,280.2 thousand common

shares, and the outstanding GDRs represented 4,780.3 thousand common shares or 0.58% of the Company's common shares.

3. Capital Surplus

Under the Company Law, capital surplus may be used to offset a deficit. The capital surplus from share issued in

excess of par (additional paid-in capital from issuance of common shares, merger and treasury stock transactions) and

donations may be capitalized once a year within a certain percentage of a company's paid-in capital. However, the

capital surplus from long-term investments may not be used for any purpose.

Additional paid-in capital - issuance of shares in excess of par

The additional paid-in capital was NT$10,777,623 thousand as of January 1, 2011. In June 2011, the bonus to employees of

NT$8,491,704 thousand for 2010 was approved in the stockholders' meeting. Of the approved bonus, NT$4,245,851 thousand

was in the form of common stock, consisting of 4,006 thousand common shares at their fair value, which were distributed in

2011. The difference between par value and fair value of NT$4,205,796 thousand was accounted for as additional paid-in capital

in 2011. In December 2011, the retirement of treasury stock caused a decrease of NT$173,811 thousand in additional paid-in

capital. As a result, the additional paid-in capital as of December 31, 2012 was NT$14,809,608 thousand (US$508,415 thousand).

Treasury stock transactions and expired stock options

In June 2011, the Company resolved to transfer treasury shares to employees. In 2011, the number of shares for transfer

to employees was 6,000 thousand, with 5,875 thousand shares exercised. Based on the fair value at the grant date,

NT$1,750,767 thousand was accounted for as capital surplus - treasury stock transactions, and NT$37,503 thousand for the

unexercised 125 thousand shares was accounted for as capital surplus - expired stock options. Also, in December 2011, the

retirement of treasury stock caused decreases of NT$20,309 thousand in treasury stock transactions and NT$435 thousand

in expired stock options. As a result, as of December 31, 2012, capital surpluses were NT$1,730,458 thousand (US$59,407

thousand) from treasury stock transactions and NT$37,068 thousand (US$1,273 thousand) from expired stock options.

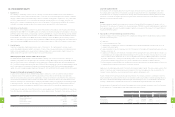

The fair values at the grant date for the fifth and sixth stock option buyback were NT$394.105 and NT$210.121, respectively.

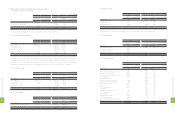

These fair values were estimated using the Black-Scholes option valuation model. The inputs to the model were as follows:

5th Buyback 6th Buyback

Assumption Exercise price (NT$) $598.83 $797.30

Expected dividend yield 3.71% 3.71%

Expected life 1.67 months 1.67 months

Expected price volatility 56.99% 56.99%

Risk-free interest rate 0.7157% 0.7157%

Fair value $394.105 $210.121

1

7

4

8

FINANCIAL INFORMATION

1

7

5

8

FINANCIAL INFORMATION