HTC 2012 Annual Report Download - page 125

Download and view the complete annual report

Please find page 125 of the 2012 HTC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130

|

|

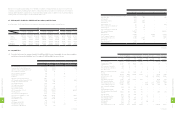

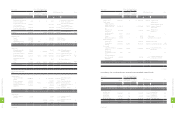

ROC GAAP Effect of the Transition from

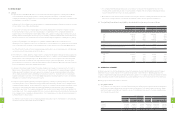

ROC GAAP to IFRSs

IFRSs Amount Item Note

Item Amount

Measurement

or Recognition

Inconsistency

Presentation

Difference

NT$ NT$ NT$ NT$ US$ (Note 3)

Non-operating income and

gains

Non-operating income

and gains

Interest income $617,635 $- $- $617,635 $21,204 Interest income

Investment gain 387,478 - - 387,478 13,302 Gain on sale of

investments

Exchange gain 666,883 - - 666,883 22,894 Exchange gain

Valuation gain on financial

assets 17,417 - - 17,417 597 Valuation gain on financial

assets

Other 550,897 - - 550,897 18,913 Other

Total non-operating

income and gains 2,240,310 - - 2,240,310 76,910 Total non-operating

income and gains

Non-operating expenses and

losses

Non-operating expenses

and losses

Interest expense 1,715 - - 1,715 59 Interest expense

Loss on disposal of

Investments 165,184 - - 165,184 5,671 Loss on disposal of

Investments

Loss on disposal of

properties 6,395 - - 6,395 220 Loss on disposal of

properties

Impairment loss 1,313,353 - - 1,313,353 45,087 Impairment loss

Other 122,912 - - 122,912 4,219 Other

Total non-operating

expenses and losses 1,609,559 - - 1,609,559 55,256 Total non-operating

expenses and losses

Income before income tax 19,450,458 7,607 - 19,458,065 667,997 Income before income tax

Income tax (1,861,272) 25,000 - (1,836,272) (63,039) Income tax c)

Net income $17,589,186 $32,607 $- 17,621,793 604,958 Net income

(1,089,693) (37,409)

Exchange differences

on translating foreign

operations

6,777 232

Unrealized valuation

gain on available-for-sale

financial assets

194,052 6,662

Unrealized valuation loss

on financial instruments

for cash flow hedging

(5,383) (185) Actuarial loss on defined

benefit pension plan d)

915 31 Income tax relating to

components of OCI d)

(893,332) (30,669) OCI for the year (net of

tax)

$16,728,461 $574,289 Total comprehensive

income

Note::

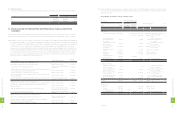

a) Under ROC GAAP, the term "cash" used in the financial statements includes cash on hand, demand deposits, check

deposits, time deposits that are cancellable but without any loss of principal and negotiable certificates of deposit

that are readily salable without any loss of principal. However, under IFRSs, cash equivalents are short-term, highly

liquid investments that are both readily convertible to known amounts of cash and so near their maturity that they

present insignificant risk of changes in value. An investment normally qualifies as a cash equivalent only when it

has a short maturity of three months or less from the date of acquisition. Some certificates of deposit the Company

held had maturity of more than 3 months from the date of investment. Thus, as of January 1, 2012 and December

31, 2012, the reclassification adjustment resulted in decreases of NT$25,474,750 thousand (US$874,549 thousand)

and NT$2,911,924 thousand (US$99,967 thousand), respectively, in "cash and cash equivalents" and increases by the

same amounts in "other current financial assets - current."

b) Under ROC GAAP, a deferred income tax asset or liability should be classified as current or noncurrent in

accordance with the classification of the related asset or liability for financial reporting. However, a deferred income

tax asset or liability that is not related to an asset or liability for financial reporting should be classified as current or

noncurrent on the basis of the expected length of time before it is realized or settled. By contrast, under IFRSs, a

deferred income tax asset or liability is always classified as noncurrent. Thus, as of January 1, 2012 and December

31, 2012, the reclassification adjustment resulted in decreases of NT$2,246,196 thousand (US$77,112 thousand) and

NT$3,530,215 thousand (US$121,193 thousand), respectively, in "deferred income tax asset - current" and increases

by the same amounts in "deferred income tax assets - non-current."

Under ROC GAAP, deferred tax assets are recognized in full but are reduced by a valuation allowance account if

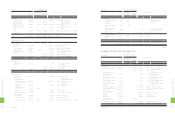

there is evidence showing that a portion of or all the deferred tax assets will not be realized. However, under IFRSs,

an entity recognizes only to the extent that it is highly probable that taxable profits will be available against which

the deferred tax assets can be used; thus, a valuation allowance account is not used. Thus, as of January 1, 2012 and

December 31, 2012, the reclassification adjustment resulted in decreases of NT$11,132,656 thousand (US$382,185

thousand) and NT$6,445,409 thousand (US$221,271 thousand), respectively, in "deferred income tax assets" and in

the valuation allowance account. Also, as of January 1, 2012 and December 31, 2012, the reclassification adjustment

resulted in increases of NT$340,261 thousand (US$11,681 thousand) and NT$647,936 thousand (US$22,244

thousand), respectively, in "deferred income tax assets" and "deferred income tax liabilities".

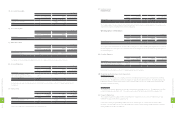

c) Under ROC GAAP, deferred income tax assets or liabilities from intergroup sales are recognized for the change

in tax basis using the tax rate of ROC. However, under IFRSs, the buyer's tax rates are used instead. Thus, the

IFRSs adjustment as of January 1, 2012 resulted in increases of NT$58,000 thousand (US$1,991 thousand) each

in "deferred income tax assets" and "accumulated earnings." In addition, the evaluation adjustment made on

December 31, 2012 resulted in increases of NT$83,000 thousand (US$2,849 thousand) in "deferred income tax

assets" and in "accumulated earnings" and a decrease in "income tax" by NT$25,000 thousand (US$858 thousand).

d) Under IFRS 1, the Company elected to recognize all cumulative actuarial gains and losses relating to employee

benefits at the date of transition to IFRSs. Thus, as of January 1, 2012, the IFRSs adjustment resulted in a decrease of

NT$83,687 thousand (US$2,873 thousand) in "accumulated earnings" due to decreases in "deferred pension cost"

by NT$342 thousand (US$12 thousand), "defined benefit assets" by NT$83,052 thousand (US$2,851 thousand) and

"net loss not recognized as pension cost" by NT$293 thousand (US$10 thousand).

As of December 31, 2012, the IFRSs adjustment resulted in a decrease in "accumulated earnings" by NT$86,417

thousand (US$2,967 thousand) due to decreases in "deferred pension cost" by NT$269 thousand (US$9 thousand),

"defined benefit assets" by NT$86,716 thousand (US$2,977 thousand), "net loss not recognized as pension cost"

by NT$347 thousand (US$12 thousand) and increase in "deferred income tax assets" by NT$915 thousand (US$31

thousand). In addition, this adjustment resulted in decreases in "cost of revenues" by NT$473 thousand (US$16

thousand), "selling and marketing expenses" by NT$526 thousand (US$18 thousand), "general and administrative

expenses" by NT$193 thousand (US$7 thousand) and "research and developing expenses" by NT$545 thousand

(US$19 thousand).

e) Under ROC GAAP, if an obligation is probable (i.e., likely to occur) and the amount could be reasonably estimated,

it is a contingent liability and should be accrued for, but under which account is not clearly defined. However, under

IFRSs, it defines "provisions" as obligations that are probable (i.e., more likely than not) and the amount could be

reasonably estimated. Thus, as of January 1, 2012 and December 31, 2012, the reclassification adjustment resulted in

decreases of NT$15,133,275 thousand (US$519,526 thousand) and NT$8,881,514 thousand (US$304,903 thousand),

respectively, in "other current liabilities" and increases by the same amounts in "provisions - current."

f) Accumulated compensated absences are not addressed in existing ROC GAAP; thus, the Company has not

recognized the expected cost of employee benefits in the form of accumulated compensated absences at the end

of reporting periods. However, under IFRSs, when the employees render services that increase their entitlement

to future compensated absences, an entity should recognize the expected cost of employee benefits at the end of

reporting periods. Thus, as of January 1, 2012, the IFRSs adjustment resulted in an increase in "accrued expenses"

2

4

6

8

FINANCIAL INFORMATION

2

4

7

8

FINANCIAL INFORMATION